– by Invoice McBride

Calculated Danger

NOTE: The tables for lively listings, new listings and closed gross sales all embrace a comparability to September 2019 for every native market (some 2019 information will not be out there).

That is the second take a look at a number of early reporting native markets in September. I’m monitoring over 40 native housing markets within the US. A few of the 40 markets are states, and a few are metropolitan areas. I’ll replace these tables all through the month as further information is launched.

Closed gross sales in September had been largely for contracts signed in July and August when 30-year mortgage charges averaged 6.85% and 6.50%, respectively (Freddie Mac PMMS).

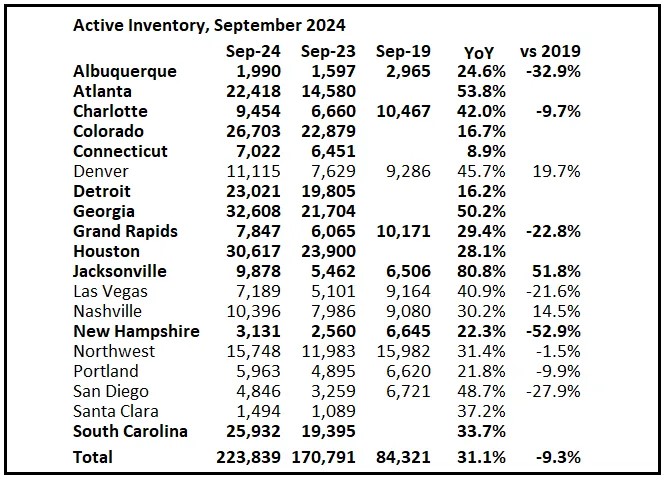

Lively Stock in September

Here’s a abstract of lively listings for these housing markets.

Stock was up 31.1% year-over-year. Final month stock in these markets was up 34.0% YoY. A key for home costs would be the degree of stock later this yr.

Stock is down in most of those areas in comparison with the identical month in 2019. Stock in Denver, Jacksonville and Nashville is up in comparison with September 2019.

There are important regional variations for stock, with sharp will increase within the South and Southeast (particularly in Florida and Texas). Most of those areas haven’t reported but for September.

Notes for all tables:

- New additions to tables in BOLD.

- Northwest (Seattle), Jacksonville Supply: Northeast Florida Affiliation of REALTORS®

- Totals don’t embrace Atlanta or Denver (included in state totals)

- Comparability to 2019 ONLY contains native markets with out there 2019 information!

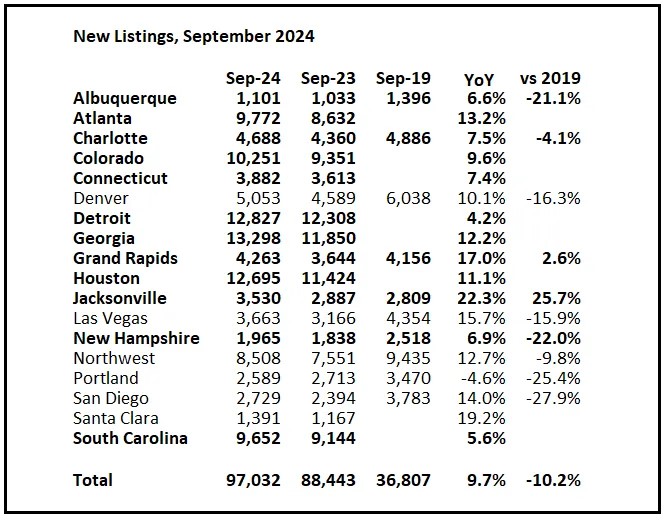

New Listings in September

And here’s a desk for brand spanking new listings in September (some areas don’t report new listings). For these areas, new listings had been up 9.7% year-over-year.

Final month, new listings in these markets had been up 9.4% year-over-year.

New listings are actually up year-over-year, however nonetheless at traditionally low ranges. New listings in most of those areas are down in comparison with September 2019 exercise (Grand Rapids and Jacksonville are up).

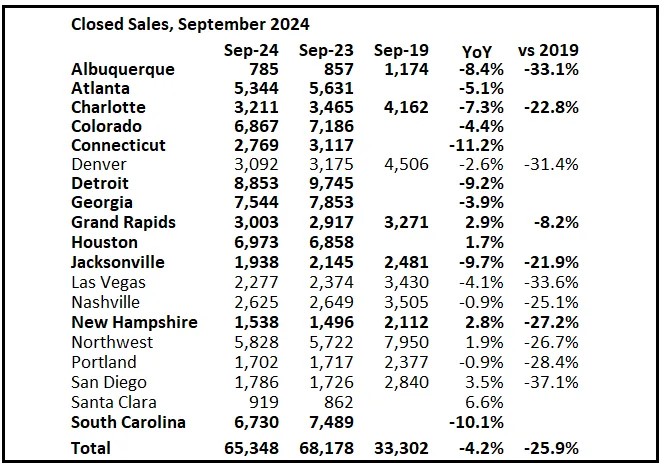

Closed Gross sales in September

And a desk of September gross sales.

In September, gross sales in these markets had been down 4.2% YoY. Final month, in August, these identical markets had been down 5.1% year-over-year Not Seasonally Adjusted (NSA).

Vital: There have been the identical variety of working days in September 2024 (20) as in September 2023 (20). So, the year-over-year change within the headline SA information can be much like the NSA information. Final month there was one fewer working day in August 2024 in comparison with August 2023 (22 vs 23), so seasonally adjusted gross sales had been down lower than NSA gross sales.

Gross sales in all of those markets are down considerably in comparison with September 2019.

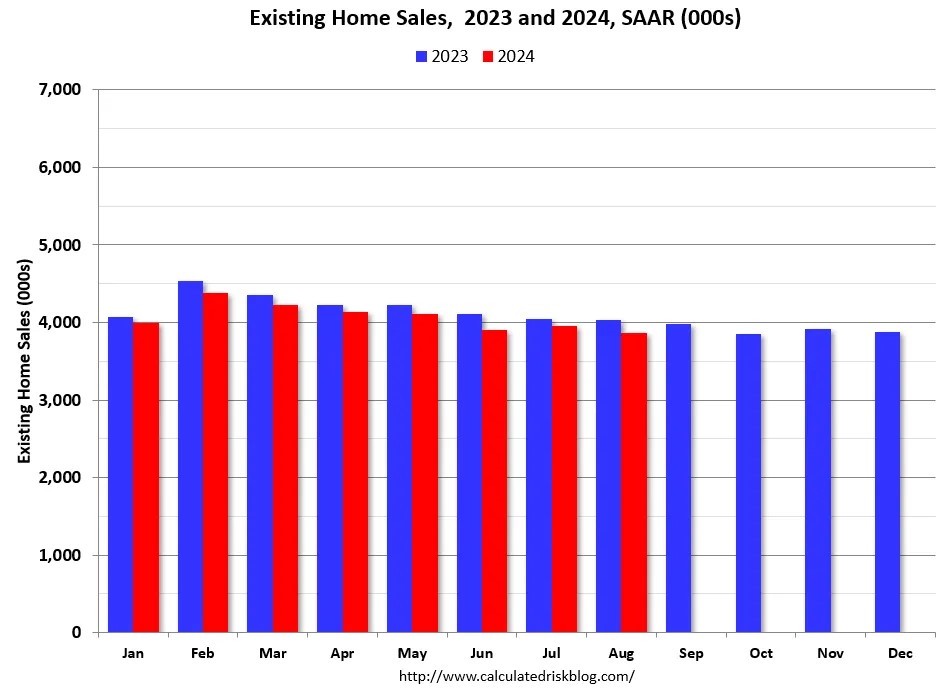

This graph exhibits current residence gross sales by month for 2023 and 2024, on a Seasonally Adjusted Annual Charge (SAAR) foundation. Final yr, the NAR reported gross sales in September 2023 at 3.98 million SAAR.

This information means that the September current residence gross sales report will present a year-over-year decline. If gross sales are up year-over-year, this would be the first year-over-year achieve since September 2021. In fact, gross sales will nonetheless be traditionally low.

Many extra native markets to come back!