Wherein I learn Paul Krugman, & as soon as once more discover myself arguing myself into believing that the Federal Reserve must have spent this spring slicing rates of interest . . .

by Brad Delong

Greedy Actuality E-newsletter

AB: I obtain a few of Brad DeLong’s commentaries in my inbox. I learn them and haven’t posted them as a result of I really feel responsible for doing so. The commentary (which incorporates Paul Krugman) if learn fastidiously agrees with what a few of us (which incorporates New Deal democrat) and also you may imagine could occur if The FED doesn’t flip lose on rates of interest. I agree with Brad. (and thanks Brad!)

~~~~~~~~

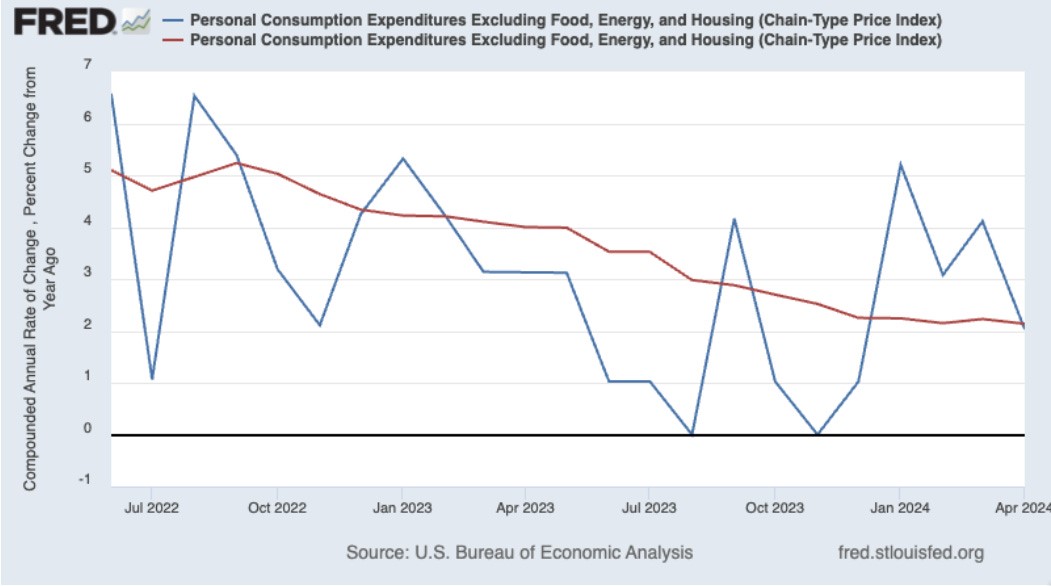

The PCE—Private Consumption Expenditures—is the Federal Reserve’s most well-liked value stage and inflation measure. The large level is that whereas the CPI—Shopper Worth Index—tracks out-of-pocket expenditures, the PCE retains observe about how shoppers shift spending when certainly one of a pair of shut substitute commodities change in value and the opposite one doesn’t. and in addition covers a broader vary of products and companies, together with, amongst different issues, medical care paid by employer-provided insurance coverage and Medicare/Medicaid. The core PCE plotted above omits meals and vitality not as a result of individuals don’t purchase them, however as a result of there’s a lengthy historic observe report that tells us that future inflation is significantly better forecast by core inflation than by the total headline index.

Paul right here removes housing from core PCE inflation as a result of “official measures of housing costs are very much a lagging indicator, reflecting a surge in rents that ended more than a year ago…. It may make sense to exclude housing costs… because a measure excluding shelter may be a [still] better predictor of future inflation…”

In each graphs, the blue line exhibits the month-to-month inflation fee, whereas the crimson line exhibits the common inflation fee over all the previous yr.

Paul’s conclusion? This:

It appears to be like as if underlying inflation might be between 2 p.c and three p.c and the recent numbers earlier this yr had been a false alarm. We could or could not have introduced inflation all the way in which again to the standard (however arbitrary) goal, however inflation actually doesn’t look as if it must be a serious preoccupation at this level . . . Inflation . . . more and more appears to be like like yesterday’s drawback, and begin worrying about the opportunity of a recession because the economic system’s energy lastly begins to erode beneath the pressure of excessive rates of interest…

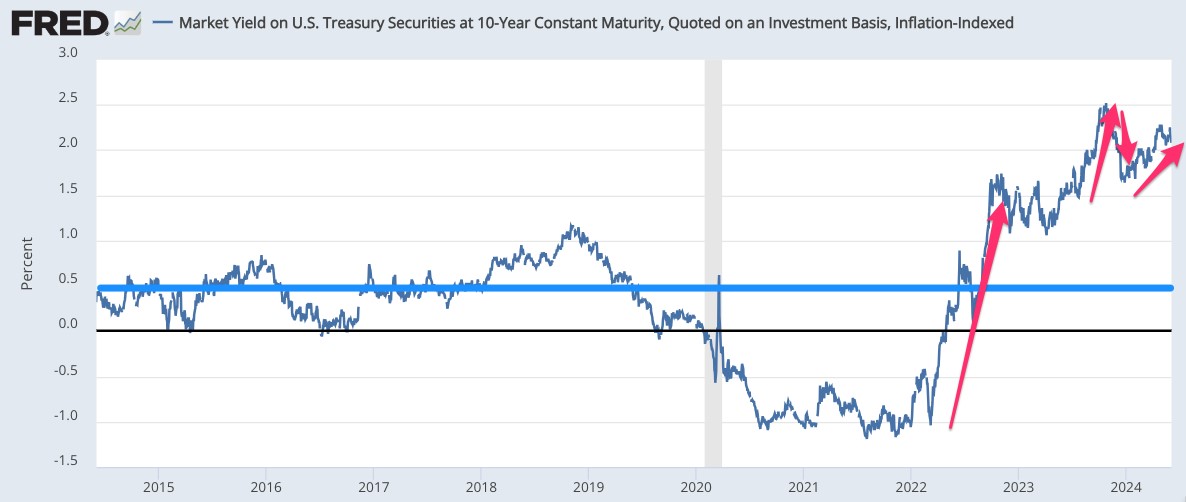

Why is Paul fearful in regards to the stage of rates of interest? One other FRED graph:

The ten-year actual rate of interest on U.S. Treasury securities is means above something you may see as its equilibrium worth in all the decade of the 2010s, and means above what it was even when it was clear in late 2021 and early 2022 that the economic system was quickly approaching full employment. Since early 2022, we have now had:

- The jump-up within the 10-Yr Treasury actual fee from -1.0% to +1.5% because the Fed moved to tighten and other people acknowledged the magnitude of that tightening.

- A late-2023 jump-up within the 10-Yr Treasury actual fee from +1.5% to +2.5% as markets determined that the Federal Reserve was certainly hell-bent at pushing inflation beneath 2%/yr even at a considerable danger of a giant recession.

- A year-cusp fall within the 10-Yr Treasury actual fee from +2.5% right down to +1.75% as markets determined that the Federal Reserve was not going to do this, however was as an alternative going to chop short-term rates of interest by as much as 1.5% in calendar yr 2024.

- The latest creep-up within the 10-Yr Treasury actual fee from +1.75% to +2.25% as markets determined that the Federal Reserve was going to maintain rates of interest increased for longer.

The argument that the equilibrium impartial actual rate of interest r* has jumped up from its +0.5% stage of the 2010s to the +1.5% it attained in late 2022 is that 4 issues have occurred:

- An amazing growth within the money owed of high-quality trusted governments has considerably eroded the protection premium.

- Massive and apparently everlasting authorities deficits are a considerable fiscal-ease issue that must be offset by financial stringency.

- The world’s financial progress configuration has shifted from investment-light to investment-heavy, with the rotation into the main sector function of decarbonization vitality and computation-heavy tech.

- Over and above (3), irrational exuberance in monetary markets has eased monetary circumstances in a means that must be offset by further financial stringency.

These could or could not have occurred.

However even when all of those have occurred, what has occurred since mid-2023 to boost r* from +1.5% to +2.25%? The one factor is that the U.S. economic system has powered forward with out financial progress weakening a lot. However my tough guideline is that financial coverage’s results on actual spending and employment work with an extended and variable lag averaging 18 months. Financial coverage turned tight in October 2022. 18 months from then is April 2024. We’re simply now beginning to get information from Might 2024.

Am I mistaken to want that the Federal Reserve had minimize short-term rates of interest this spring in an effort to maintain the Ten-Yr Treasury actual fee round +1.5%?