– by New Deal democrat

Whereas we’re ready for brand new financial knowledge tomorrow, let me choose up on a problem I closed with yesterday: whereas manufacturing has turned down, items manufacturing within the US economic system is being held up by building, and particularly residential building. Given the extreme hike in mortgage charges in addition to home costs, I described it as “levitation.” So in the present day let’s take a look at that levitation.

As per regular, I at all times begin out with the truth that mortgage charges lead gross sales. The under graph contains mortgage charges (blue, left scale) in contrast with housing permits (crimson, proper scale) and the much more main, however very noisy new single household house gross sales (grey, proper scale). The latter two are normed to their peak at 100:

And as mortgage charges elevated from 3% to 7%, gross sales and permits declined about 20%, +/-5%. This can be a severe decline, which has typically however not at all times meant a recession has adopted.

For completeness’ sake, right here is actual personal residential mounted spending from the GDP reviews in contrast with single household permits, which have been the least noisy main housing metric of all. Once more, each are normed to 100 as of their peaks, and permits are averaged quarterly for higher comparability:

Observe that actual housing spending within the GDP has declined about 15%.

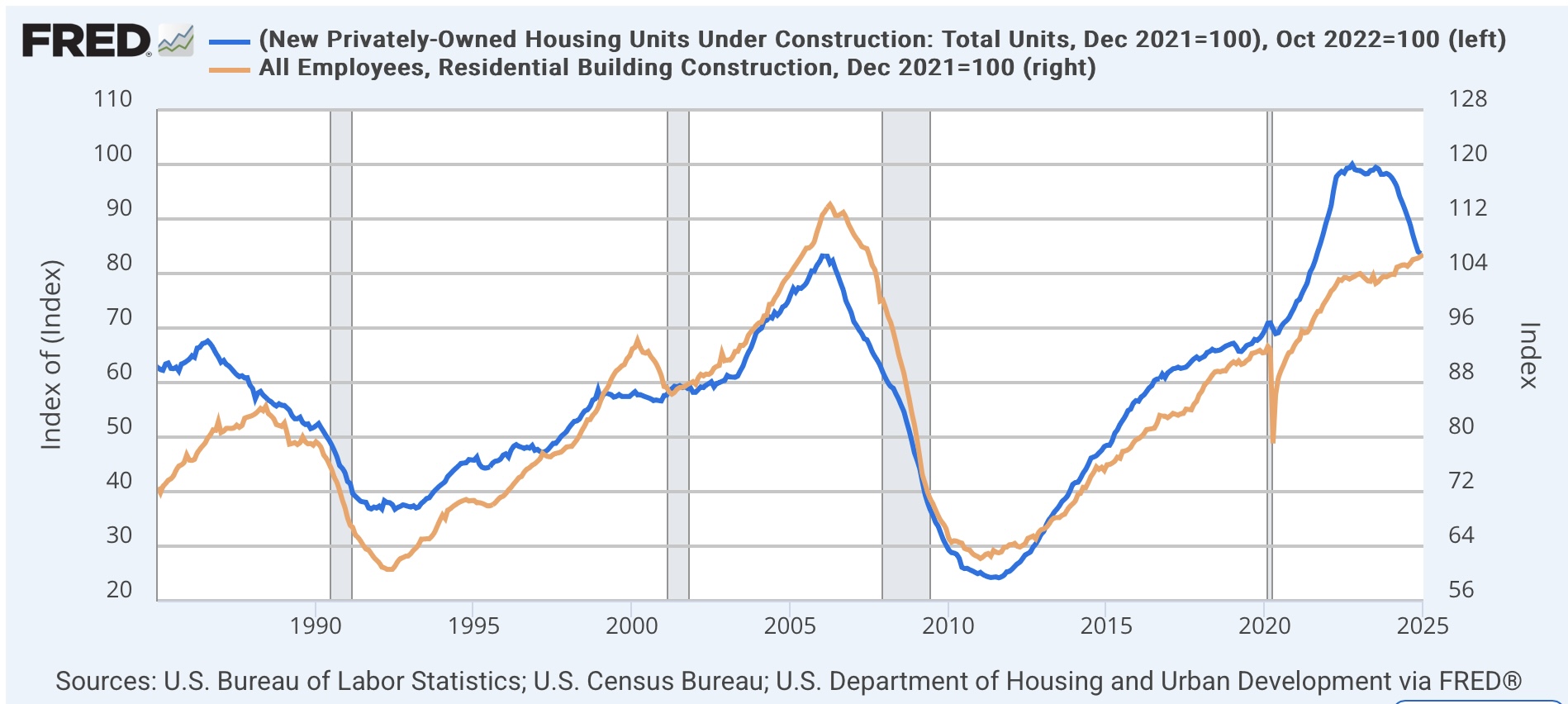

Subsequent, the noisier housing begins (gentle orange) comply with permits by a month or two. And housing models underneath building (which fluctuate by begins minus completions), a that are the “real” combination financial exercise, comply with with a big delay, on this case by virtually 1 yr. Observe once more all three are normed to 100 as of the month of their peaks:

The primary act of levitation after the pandemic was how models underneath building stayed virtually completely flat for about 18 months after they approached their peak. Traditionally this was a really lengthy delay.

However in the end housing models underneath building turned down, and did so with a vengeance, now down over 15%, which prior to now has been in line with a recession, though not at all times. Which leads us to the second act of levitation, which is the variety of workers concerned in housing building (gold, proper scale):

Employment in residential building has continued to extend, regardless of the downturn in each different housing sector metric!

When would possibly we count on this final shoe to drop? Right here’s the long term historic look:

Within the case of the 2000s housing bubble, building employment turned down with solely a really slight delay. The 2001 recession was partly a tech bubble, partly the China manufacturing employment shock, and partly the September 11 terrorist assaults, so housing building didn’t flip down meaningfully. Residential building employment peaked 15 months after housing building turned flat.

Maybe the closest analogue is the Eighties building increase. Here’s a close-up on that period:

Within the Eighties, residential building employment elevated for 22 months after precise building turned down.

The place does that depart us now? We’re at present over two years after the precise peak in building, and roughly 18 months because it turned down considerably. Because the above historic graph exhibits, the final three natural recessions (i.e., not together with the pandemic) began as soon as residential building employment was down 10% (and the traits in different sectors usually main recessions additionally had been in place).

I’ve been searching for residential building employment to show down for no less than half of yr. My greatest guess is that it’ll lastly flip down in some unspecified time in the future within the subsequent six months, if the remaining financial items (particularly mortgage charges!) stay in place. As soon as they do flip down, they could comply with a equally sharp decline as building already has, which might recommend a recession 12-18 months afterward common. Please observe this final sentence is *not* a forecast, solely a mean. There are a lot of different transferring elements to think about.