I had introduced Half I and Half II some time again. Half III was tough to current in a piece-meal manner so for now I’ve set it apart. What’s fascinating about Half IV is I can beak it aside into segments, nonetheless keep the movement of informatio, and current it in a logical method. Bear with me. By the point we get to the tip, I consider it is possible for you to to piece this collectively too. In Half IV . . .

What Antonio is doing in Half IV is laying the muse for the query requested: Are Drug Corporations Alone Accountable for the Costs We Pay for Medicines? He intends to interrupt it down. I intend to interrupt it down additional for Offended Bear.

Cash from Sick Folks Half IV: Paying a Premium for Drug Pricing Irregularity, 46brooklyn Analysis, Antonio Ciaccia

One of many principal issues in making an attempt to grasp drug costs is the policymakers haven’t determined what they need drug pricing coverage to really accomplish (we not too long ago raised this level in our evaluation of Might 2024 drug pricing adjustments). With no guideline or philosophy to behave as a beacon for coverage finish targets, drug costs could also be skilled throughout any variety of potential paradigms and serve many potential targets – which frequently leads to many drug costs for a similar product. In different phrases, the observations of worth discrimination within the drug provide chain has grow to be a characteristic, not a flaw, throughout the U.S. healthcare system.

We all know drug costs – no less than the costs skilled by the tip payer – aren’t set in accordance with the worth a pharmacy pays to amass these medicines. Within the landmark Rutledge v PCMA choice, the U.S. Supreme Court docket put this truth on the market comparatively merely, succinctly, and in a unanimous method by stating,

“The amount a PBM ‘reimburses’ a pharmacy for a drug is not necessarily tied to how much the pharmacy paid to purchase that drug from a wholesaler.”

We battle to think about different industries the place the supplier of a product (i.e., the pharmacy) would have such little say in establishing costs in relation to the merchandise it’s providing and their corresponding underlying prices (and but that’s what we all know occurs with medication). That’s not to say it doesn’t occur, simply that our notion is that when a grocer desires / wants the next worth for milk they increase the worth for milk, when a pharmacy desires / wants the next reimbursement to cowl their prices they . . . properly, we’re unsure what they’ll do instantly to enhance their worth like grocers or others can do (which is the purpose we’re making an attempt to make). We additionally know that drug pricing is extra variable (i.e. there are various costs for a similar product) than a single producer’s worth level may probably yield.

Undoubtedly, the worth of a medicine begins with a producer, nevertheless it definitely doesn’t finish there – nor can it’s utterly understood by simply the producer worth level. If the worth paid for a drugs was solely derived by the worth set by the producer, then everybody’s pricing expertise can be constant.

However it isn’t.

That truth doesn’t cease some from claiming that drug producers, and drug producers alone, are answerable for drug pricing. Conversely, it doesn’t cease the identical teams from claiming they alone are working to decrease drug costs. Such easy views on drug pricing must be rejected, as they aren’t based within the details. And to assist clarify why, at this time we display simply how all-over-the map U.S. drug costs are by revisiting the costs of insulins within the aftermath of the massive insulin drug listing worth cuts that happened in the beginning of the 12 months.

Some Background

Insulin has been the poster baby of drug pricing dysfunction for many years. Unsurprisingly, insulin has been a frequent flyer in our Cash From Sick Folks sequence, as a number of effort has been directed at making an attempt to grasp how a life-saving remedy (folks with Kind 1 Diabetes will die with out insulin) can for some be an inexpensive remedy, whereas others submit tragic movies highlighting their incapability to get the remedy they so desperately want. Whereas there are various potential insulin merchandise, the variability in affected person expertise is itself demonstrative of how an insulin product, with a producer listing worth, and a worth paid by the shelling out pharmacy to amass it, can yield such divergent views on insulin costs.

Whether or not immediately associated to those affected person tales or not, laws was handed, signed into regulation, and enacted which capped the amount of cash Medicare beneficiaries could be required to pay to get a month’s provide of insulin. The Inflation Discount Act (Biden) capped the month-to-month worth of insulin at $35 for Medicare enrollees beginning in 2023. Which suggests whatever the historic harms with insulin we’ve confirmed with rebates (Cash from Sick Folks Half I) or a supplier’s deeply discounted acquisition price (Cash from Sick Folks Half II), Medicare enrollees can anticipate some type of worth safety from these previous behaviors. Undoubtedly a great factor.

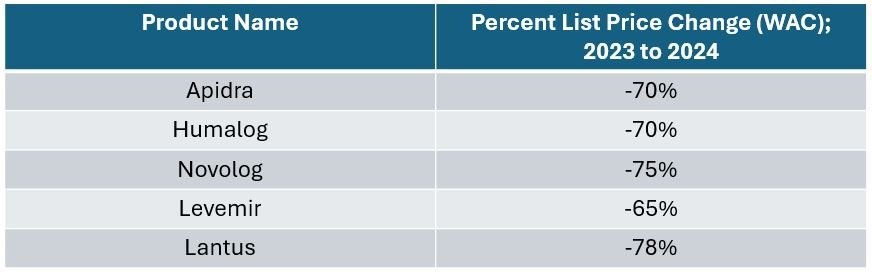

Nevertheless, the worth of these financial savings are maybe lower than when initially envisioned. Why? Effectively, insulin merchandise (not all, however the majority from a utilization standpoint) took worth decreases (like huge, 70%+ decreases) in 2024. For many who could have missed it (undoubtedly not a daily 46brooklyn reader), 5 insulin merchandise took important drug listing worth decreases in the beginning of January 2024 (technically some squeaked within the final week of 2023, however we’re calling these 2024 worth decreases). Particularly, as proven in our Model Drug Checklist Value Field Rating.

Determine 1 under outlines the product and the extent of their worth decreases:

Determine 1 Supply: Elsevier Gold Normal Drug Database, 46brooklyn Analysis

The importance of those worth drops was not misplaced on us, given the historical past of controversy surrounding the insulin market dynamics. And whereas there some good protection of those huge cuts, we perceive why extra informal observers could have missed them, for the reason that years of headlines of rising insulin costs far outmatched the protection of their cratering.

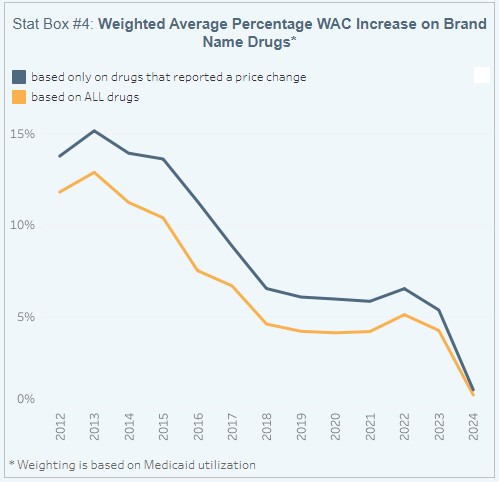

These medication, which had been priced at a number of a whole lot of {dollars} per bundle beforehand, are all now under $100 a bundle (no less than, on the idea of the producer set-list worth). The influence of those worth decreases are such that they kind of broke our notion of producer listing worth conduct adjustments broadly (no less than as measured inside our Model Field Rating in Determine 2 to the precise (Supply: Elsevier Gold Normal Drug Database, CMS State Drug Utilization Information, 46brooklyn Analysis). It’s because these merchandise signify a number of historic proportional drug spending, and so after we try and weight worth change expertise throughout model medication, we understand virtually no listing worth change conduct for 2024; a first-time commentary in additional than a decade of drug pricing context (see earlier dialogue of the phenomenon and the Model Drug Pricing Field Rating).

To display simply how essential these merchandise are to our broader prescription drug ecosystem, the 5 insulin merchandise outlined above had (Determine 1) over $11 billion in gross drug spending throughout virtually 14 million prescriptions in 2022 in Medicare (the final 12 months that has public knowledge obtainable concerning Medicare spending and utilization). These merchandise are important sufficient to signify roughly 1% of drug utilization in Medicare and 5% of gross drug spending. Stated otherwise, one in 20 {dollars} spent on the pharmacy counter in Medicare was an insulin greenback.

Unsurprisingly, the listing worth reductions acquired a number of constructive reward from a wide range of sources. And but, we nonetheless can’t fairly clarify insulin costs on the pharmacy counter in relation to the producer listing worth or the pharmacy’s price to amass.

What will we imply?

Effectively, contemplate what we would understand to be the significance of those worth decreases relative to the worth supplied from the $35 insulin copay cap. To do that, we’ll have a look at the total wholesale acquisition price (WAC) worth for probably the most generally utilized Medicare insulin – Lantus (we’re going to particularly have a look at the ten mL vial; that is one we’ve beforehand used in our Cash From Sick Folks sequence, so it helps maintain issues constant).

In 2023, earlier than Lantus’ worth lower, one vial of Lantus ran $292, which signifies that the Medicare $35 copay max would have meant a affected person was paying roughly 10% of the producer’s listing worth. In 2024, after Lantus’ worth lower, one vial of Lantus now prices $64, which means that the $35 cap means the affected person is paying round 54% of the producer’s listing worth.

What we will begin to see is that whereas it may be helpful to some for producers to decrease their worth, the tip results of listing worth decreases isn’t one that’s assured to be universally of profit. All of us (together with Medicare beneficiaries) need to pay cash (through premiums) to get entry to the good thing about price sharing for medicines on the pharmacy counter (i.e., the $35 cap vs. the total producer listing worth), and the way a lot worth our premium {dollars} safe (i.e., how a lot safety we get from gross costs on the pharmacy counter) is a perform of how a lot worth the well being plan passes on to the end-user. This was the purpose we made again with Cash from Sick Folks Half I with regard to rebates, however may have revisited in gentle of decrease priced insulins. If that sounds intriguing, then learn on to our evaluation of “Money from Sick People” Half IV, the place we try to elucidate how tousled insulin drug costs stay utilizing the biggest insurer within the nation: Medicare.

Mission achieved: Producers decrease insulin costs

Undoubtedly, there are some who’ve kind of solely advocated for the concept if drug producers would simply decrease their drug costs, we might all profit. Definitely, we will perceive how if one believes that drug producers are alone answerable for the tip drug pricing expertise, then advancing and advocating for insurance policies that may cap producer costs would appear to make sense (if we settle for the premise that worth controls would don’t have any different collateral harms). If the matter is so simple as producers setting decrease listing costs, then success can be measured comparatively merely for the insulin merchandise outlined above.

Stated otherwise, we all know the diploma to which producer listing costs for insulins modified – with worth cuts that vary from 65% to 78% – and so we might anticipate that if the diploma of these listing worth adjustments correlated with the adjustments in insulin costs skilled in Medicare, then we might undoubtedly be capable to declare drug pricing success. The arrange was such that we couldn’t resist looking.

So, quite than take heed to the phrases of advocacy teams, let’s ask the query to Medicare’s personal drug pricing knowledge:

Are drug corporations alone answerable for the costs we pay for medicines?

To start, we have to focus on our knowledge supply for this evaluation. The Facilities for Medicare & Medicaid Companies (CMS) publishes within the public area a set of information known as the “Quarterly Prescription Drug Plan Formulary, Pharmacy Network, and Pricing Information.” As described by CMS, these information present data on Half D formulary, pharmacy community, and pricing knowledge for Medicare Prescription Drug Plans and Medicare Benefit Plans. Particular to drug costs, which is what we’re fascinated about (that is 46brooklyn, duh), CMS states the pricing data offered displays “plan level average monthly costs for formulary Part D drugs.” Digging deeper (see FAQ), the pricing data is definitely damaged out in a pair methods, akin to being doubtlessly variable whether or not the day provide is 30 or 90 days for the plan, however ought to replicate, “the average cost for the day supply at in-area retail pharmacies for the Medicare plan.”

In a manner, and as a fast sidebar, these acknowledgements by CMS are welcomed by these of us at 46brooklyn, as they signify, from a sure point-of-view, that drug pricing isn’t topic to simply the producer listing worth. Why would we have to acknowledge {that a} 30-day unit worth could not equal a 90-day unit worth if producers alone had been answerable for drug costs. In case it isn’t apparent, producers don’t have any bearing on the day provide of the prescription distributed, quite that could be a perform of affected person want, prescriber choice making, pharmacist approval, and plan profit selections to permit or disallow the follow of prolonged days provides. And but, we settle for and acknowledge that costs are variable primarily based upon days provide such that we additionally acknowledge the forces past producer listing worth.

With the reassurance gathered from the background on the CMS knowledge supply, we pressed forward with gathering these information for 2023 and 2024 such that we may evaluate the Medicare insulin pricing expertise pre- and post-drug producer listing worth decreases on the Medicare plan stage. Because the information are revealed quarterly, and never all of 2024 has elapsed, we elected to seize the Q1 information for each 2023 and 2024 to have as ‘apples-to-apples’ comparability as we may arrange in the beginning. On this manner, we will immediately observe who did and who didn’t profit from drug listing worth decreases and hopefully see if listing worth adjustments resulted in a shared common expertise for all (spoiler alert: they didn’t).

As manner of fast reminder, we’ve already acknowledged that as of January 1, 2023, there was a cap for a month’s provide for every insulin product in Medicare. Particularly, no prescription drug plan in Medicare can cost greater than $35 per 30 days’s provide of every insulin product (no matter whether or not the insulin is a most well-liked or non-preferred product). We make this notice of distinction as a result of the Medicare plan price doesn’t essentially equal the Medicare enrollee’s price (no less than in a roundabout way).

As we already demonstrated, the notion of worth of the $35 affected person out-of-pocket cap modified primarily based upon these listing worth adjustments, however we’re principally gathering the pricing knowledge from Medicare to research the plan’s drug pricing view (as sufferers are already shielded from previous Cash from Sick Folks coverage). Once more, and for emphasis, CMS states the pricing data we’re relying upon displays “plan level average monthly costs for formulary Part D drugs.” Nonetheless, if producer listing worth = drug worth (and nothing else issues in that equation), then we anticipate an inventory worth lower to completely equal a plan drug worth lower.

Just a few extra housekeeping gadgets earlier than we get into the evaluation . . . We pay premiums for insurance coverage, together with in Medicare, partly to entry protection and get monetary safety towards doubtlessly expensive claims. If there are extra claims or greater price claims, the price of insurance coverage premiums will go up (no matter whether or not we’re speaking drug prices or properties or vehicles). For prescription drug insurance coverage, the costs we’re reviewing are the gross drug costs of the plan (which our evaluation will give attention to), and we must always acknowledge that no matter our findings on plan prices, sufferers needing insulin had been kind of protected on the pharmacy counter from the pricing disparities we’re going to examine (although that will or could not have benefited them ultimately). Moreover, we must also acknowledge that for 2024, adjustments within the dealing with of Medicare direct and oblique remuneration (DIR) require that pharmacy costs replicate the “lowest possible reimbursement” for a Half D drug. We interpret this to imply that whereas the 2023 costs we’ll evaluation could also be inflated by a level of unknown pharmacy DIR, no quantity of pharmacy DIR can be anticipated to fairly clarify any noticed variations within the 2024 information (given the rule). That is essential, because it represents a possible distinction in notion to deciphering the 2023 worth variability that can not be readily used to elucidate any potential 2024 worth variability.

There may be all the time extra to say, however we predict that’s enough sufficient background to start. As all the time, we encourage our readers to learn the data of the underlying knowledge supply (i.e., the Quarterly Prescription Drug Plan Formulary, Pharmacy Community, and Pricing Info) earlier than we start to supply our perspective on what these drug costs imply.

Subsequent Up an Evaluation of Pricing and its Variability for Insulin.