If we have been to take a look at the prices of healthcare insurance coverage for households and companies, it has not remained the identical percentage-wise for employers or workers. My preliminary sentence is a backwards approach of claiming prices are rising sooner than features in earnings for both.

Nothing has modified right here and the foes to single payer in authorities and trade maintain insisting that is the higher approach to supply healthcare. Edward Kennedy died too quickly to assist us with Single Payer.

Such a plan shouldn’t be uncovered to governmental cuts on account of politics. Certainly, it ought to be much like Social Safety. One thing politicians shouldn’t mess with except they don’t worth their standing in Washington D, C. There’s a higher strategy to say this. It eludes me proper now.

The Wall Avenue Journal (to which I subscribe) posted a short commentary “Healthcare Premiums Are Soaring Even as Inflation Eases, in Charts.” Their opening assertion?

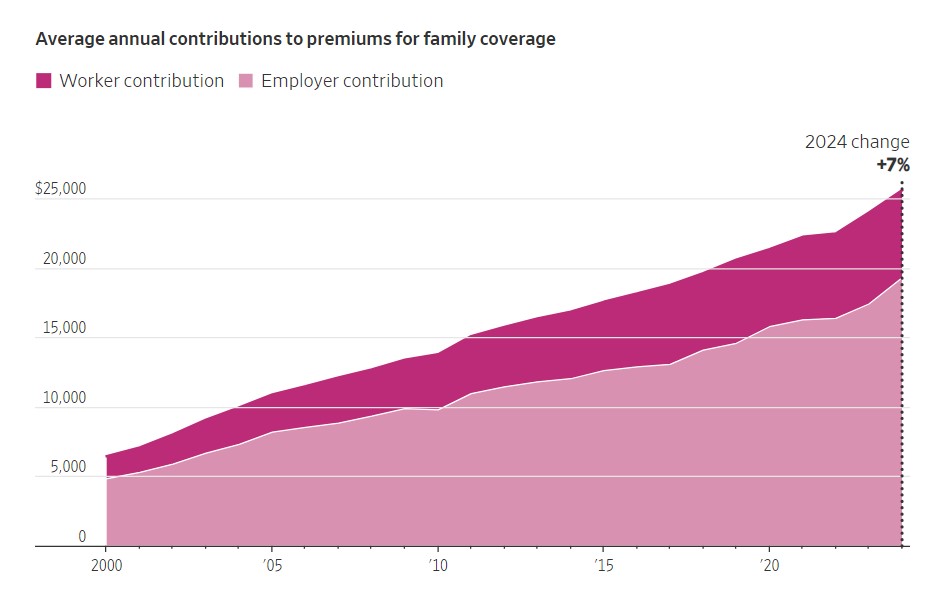

“Again-to-back years of will increase in Healthcare premiums have added to the typical price of household protection, reaching roughly $25,500 this yr for employers and staff.“

To which the assertion of rising healthcare prices is true. I believe there shall be no finish quickly to the will increase in healthcare prices to labor, companies or the income on the different finish. The next WSJ chart depicts the rising prices to Staff and Employers.

Inflation is easing throughout a lot of the financial system. For healthcare? Not but.

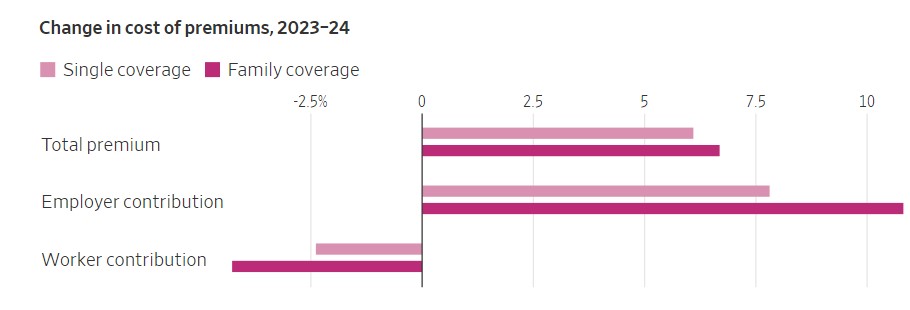

The price of employer medical health insurance rose 7% for a second straight yr, sustaining a progress fee not seen in additional than a decade, based on an annual survey by the healthcare nonprofit KFF. The back-to-back years of fast will increase have added greater than $3,000 to the typical household premium, which reached roughly $25,500 this yr.

Companies did take in this yr’s larger premium prices. Doing such alerts (lately), employers are delicate to the boundaries of what staff can afford. Matthew Rae, affiliate director of the KFF healthcare market program and an writer of the survey:

Employers spent about $1,880 extra this yr, bringing their common price for household premiums to $19,276. A staff’ share of the typical household premium dropped by roughly $280 from final yr, to $6,296.

Companies can’t maintain that up, mentioned Shawn Gremminger, chief government of the Nationwide Alliance of Healthcare Purchaser Coalitions, an employer group. And staff in the end bear these larger prices in different methods, he mentioned, together with smaller raises or job cuts. Including . . .

“That’s adding real stress to the economy.”

Outlook for 2025

Stress on the sector is predicted to proceed, at the least for an additional yr. Employers and profit consultants state health-insurance prices are projected to rise quickly once more in 2025.

Healthcare prices don’t change as swiftly as in different sectors of the financial system, the place inflation has cooled. Costs for well being companies are sometimes locked in beneath multiyear contracts.

As well as, hospitals have not too long ago gained new contracts with bigger value will increase claiming they want such to offset raises for his or her staff. There may be an argument to this logic which I can’t embody right here.

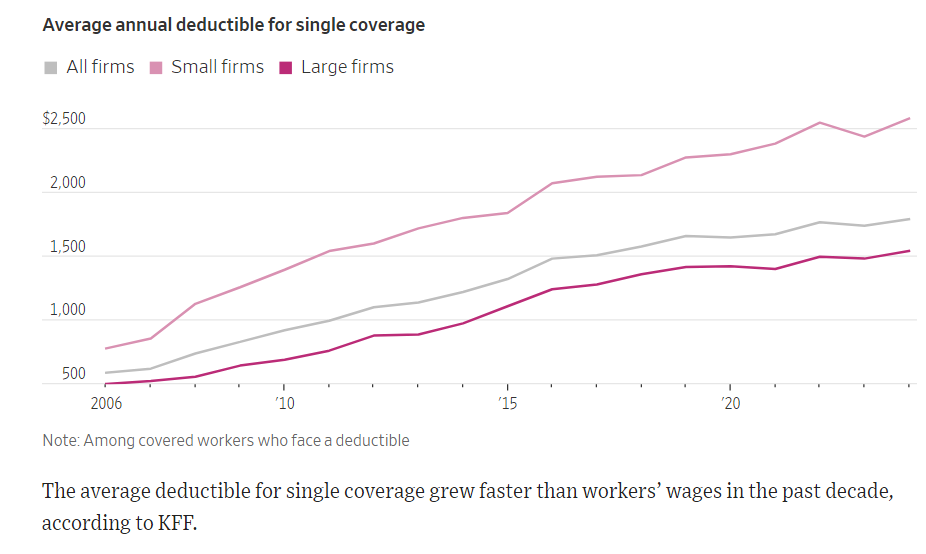

Deductibles edge upward

Will increase in deductibles? The quantities workers should pay out of pocket earlier than medical health insurance kicks in is steep and has been for years. It has eased extra not too long ago as a result of the expense may have already got been greater than staff might afford based on Matthew Rae of KFF.

Nevertheless, this yr the typical deductible for big firms inched larger by 4% for staff with single protection. Staff in smaller firms have been hit tougher with deductibles rising a median 6% for single protection deductibles yearly.

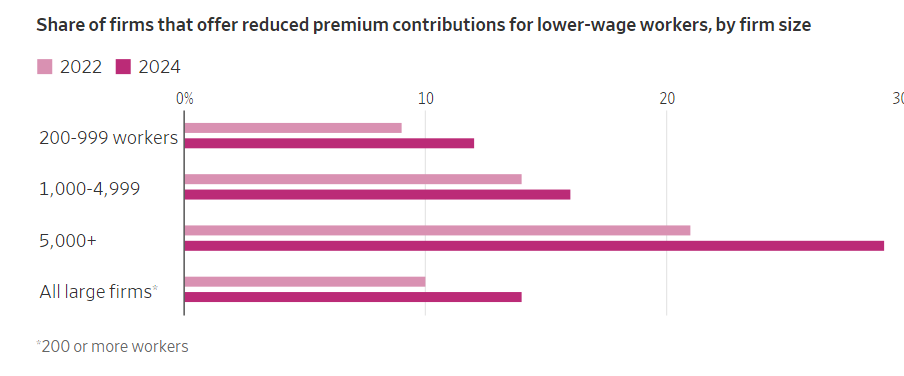

Decrease-wage staff may pay much less

To assist staff afford medical health insurance, some giant employers are decreasing the prices for staff with decrease wages.

Some giant employers are additionally providing lower-wage staff health-insurance options with skimpier advantages and low premiums. Practically one in 5 of the most important employers reported having these restricted plans.

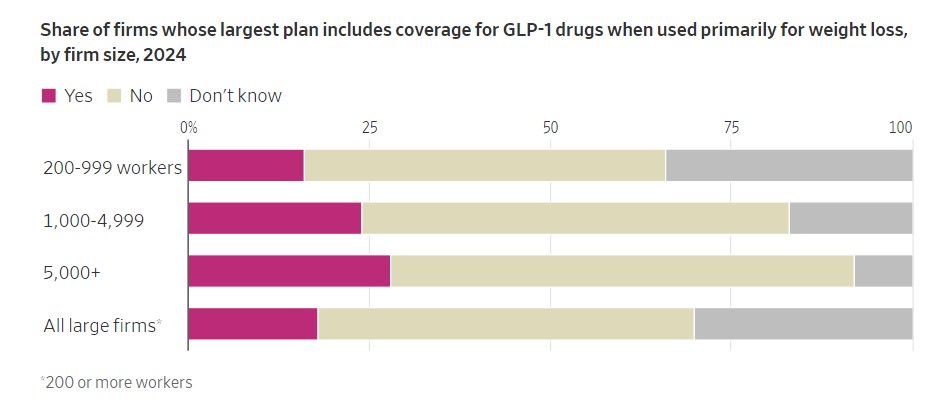

Employers maintain off on weight-loss medicine

Most employers proceed to not cowl weight-loss medicine, based on the KFF survey. Whereas staff are asking for the medicine, employers have balked due to excessive prices.

Even when companies cowl the medicine, that doesn’t assure staff unfettered entry. Roughly half of the companies require staff to clear hurdles earlier than or whereas filling prescriptions. They require workers to pursue different avenues for weight reduction.

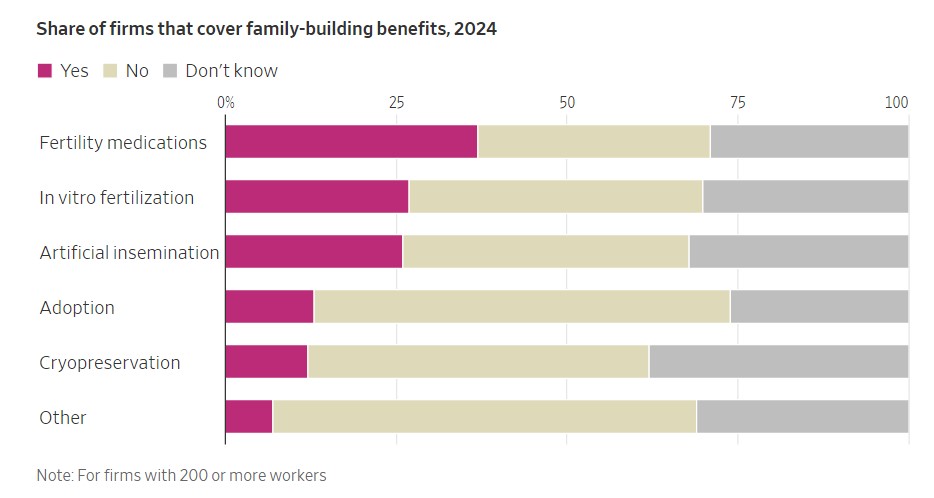

In vitro fertilization, fertility protection are restricted

Throughout all companies of at the least 200 staff, few firms report providing fertility advantages. Thes isn’t the case among the many largest employers.

Roughly half of the nation’s largest employers supply well being advantages for fertility drugs, synthetic insemination or in vitro fertilization. Firms did add the advantages to recruit staff throughout the not too long ago tight labor market.

Survey respondents in some circumstances reported “don’t know” to questions on their protection of the companies.

The KFF Employer Well being Advantages Survey was performed within the first seven months of 2024 and included 2,142 employers that responded to the total survey.

Sources for graphics: KFF (employer survey); Bureau of Labor Statistics (inflation, staff’ earnings)

Write to Melanie Evans at [email protected] and Josh Ulick at [email protected]

How Well being Insurance coverage Prices Outpace Inflation, in Charts, Wall Avenue Journal.