Certainly one of a number of articles I picked up on over the previous few days. and determined to submit at Indignant Bear. Youthful persons are overextending themselves financially to purchase housing. Not so completely different than just a few a long time in the past. Besides they’re extra in debt.

Hitting House: Housing Affordability within the U.S. March 2024

The Problem:

Information reviews abound of housing changing into unaffordable to a widening swathe of the American inhabitants, each residence consumers and renters and throughout the nation, not simply in historically excessive worth areas like San Francisco and New York. This deteriorating affordability instantly impacts American lives, together with the place individuals select to stay and work. It has additionally been cited as a significant contributor to key social issues like rising homelessness and worsening youngster wellbeing. How does affordability differ throughout areas and revenue courses? What components are making housing unaffordable and may insurance policies counter them?

The Info:

- Housing affordability has worsened over the previous 20 years. Median home costs at the moment are 6 instances the median revenue, up from a variety of between 4 and 5 20 years in the past. In cities alongside the coasts, the numbers are larger, exceeding 10 in San Francisco as an illustration. The ratio of median rents to median revenue has additionally crept up over this era from 25 % to 30 %. Rising home costs are a selected downside for these intending to purchase their first houses, whereas present householders are cushioned considerably by their elevated fairness in the home as the value of their residence rises.

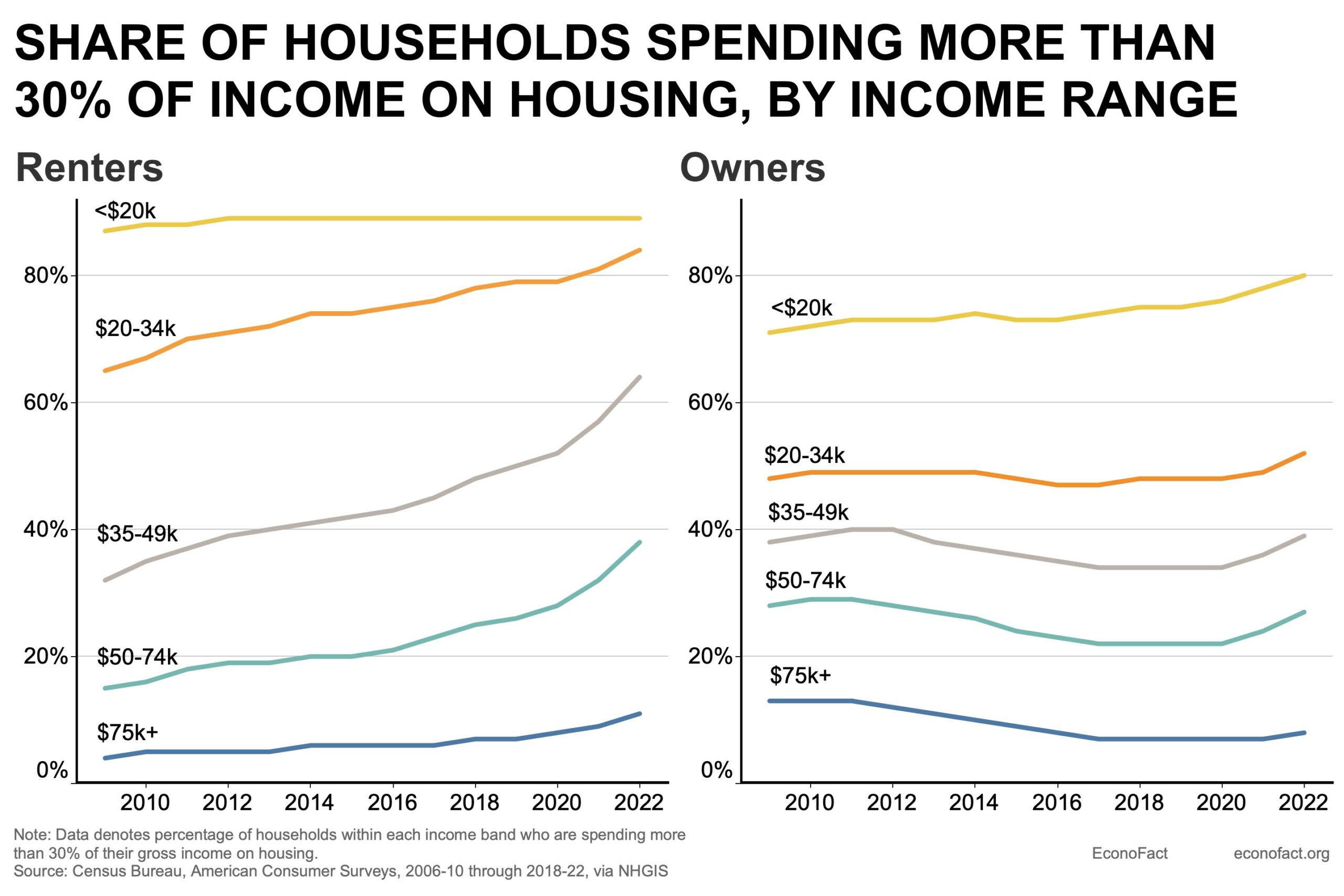

- Households — renters particularly — are more and more cost-burdened. Households are thought-about cost-burdened in the event that they spend greater than 30% of their revenue on lease, mortgage and different housing wants. Amongst householders, about 40 % of these within the $35,000-49,000 revenue vary are cost-burdened, although this share has not modified a lot over the previous decade (see chart). In distinction, the share of cost-burdened renters in that revenue vary has risen sharply from beneath 40 % of households in 2010 to over 60 % immediately. Whilst most households are spending a smaller share of their funds on different fundamentals like meals and clothes, the share of family’s budgets spent on housing has elevated. On common the price of housing has elevated by $5,000 (2021 {dollars}) per yr since 1984.

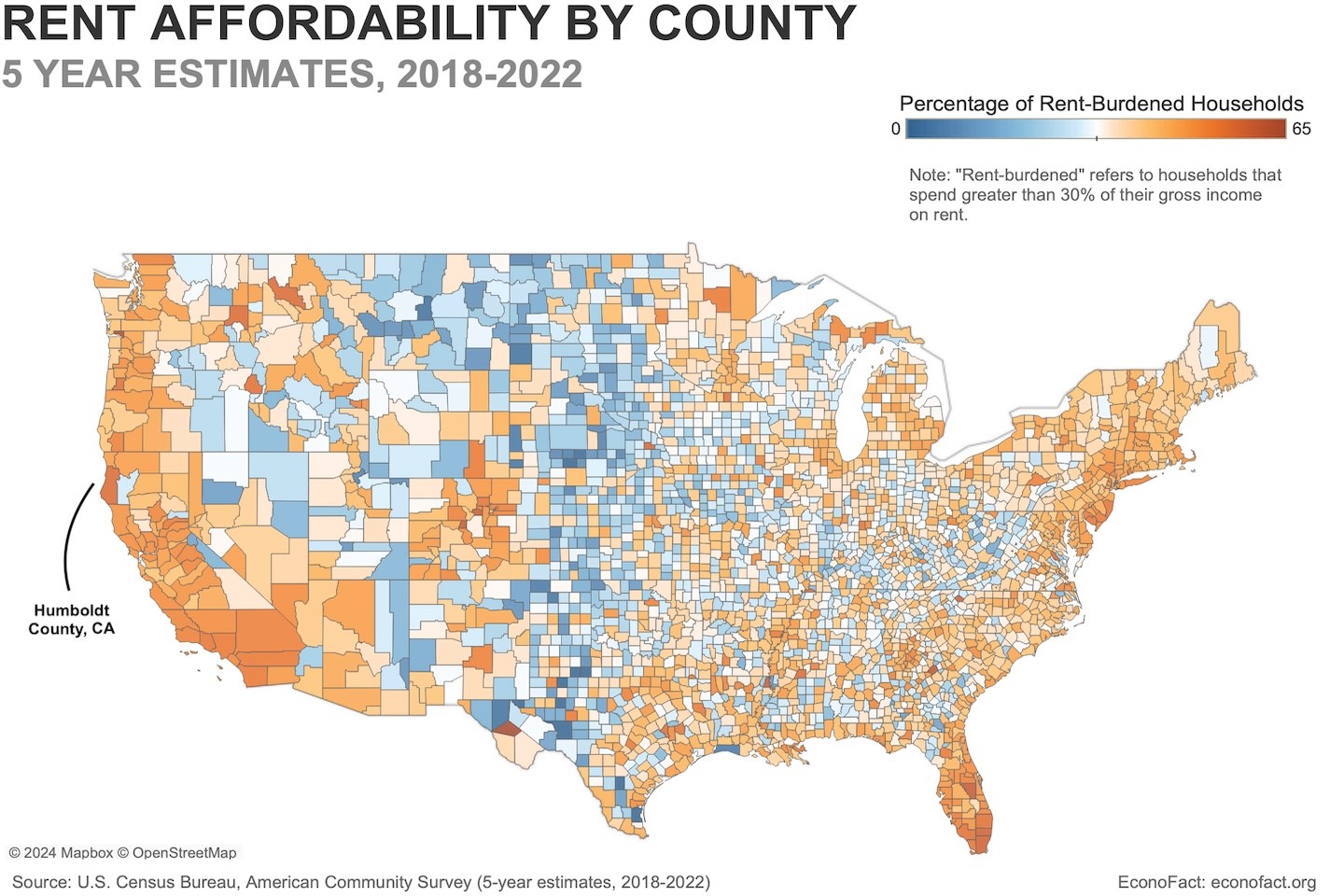

- Affordability is changing into a problem throughout the nation. Traditionally, rural and inside areas of the nation have been extra inexpensive. However, even previous to the pandemic, migration towards these areas has helped drive sooner home worth appreciation than in dearer areas. The pandemic and elevated use of distant work practices additional leveled the enjoying discipline: city flight to much less densely populated — and usually cheaper — areas has additional shrunk the affordability hole between areas. However, the coastal elements of the nation stay extra cost-burdened than the remainder of the nation, notably for renters (see map beneath). As an example, 56% of Humboldt County households in California’s redwood coast are rent-burdened.

- The dearth of inexpensive housing has contributed to rising homelessness in lots of cities. About 250,000 Individuals have been with out houses in 2023, in accordance with estimates by the Division of Housing and City Growth, with 1 / 4 of them concentrated in New York and Los Angeles. And whereas the causes of homelessness are complicated, lack of housing provide is taken into account to play a big function.

- The decline in housing affordability displays a mixture of longer-term and cyclical components. Demographic developments have contributed to the demand-supply imbalance. Provide is crimped by extra older Individuals opting to age in place — selecting to stay single-family householders somewhat than transfer in with different members of the family, right into a retirement neighborhood, or a smaller residence — than was the case a decade in the past. Whereas residence tenure has at all times been larger for older households than youthful ones, the variety of over- 65s has quadrupled from 15 million to 60 million since 1960. The growing older inhabitants is the largest driver of lengthening residence tenure. On the demand aspect, the largest driver is new family formation. Individuals fashioned about 1,000,000 new households a yr between 2015-2017, however the tempo has virtually doubled in accordance with probably the most current knowledge, largely reflecting a pickup in family formation charges amongst millennials.

- A protracted-standing lack of homebuilding has additionally contributed to rising residence costs. Whereas lack of homebuilding is a matter in lots of international locations the shortfall has been notably acute in the USA. Amongst comparable main international locations, the USA is the one one through which the housing inventory grew extra slowly than the inhabitants between 1995 and 2020. The deficit was notably pronounced following the 2008 Nice Monetary Disaster: fewer new houses have been constructed within the 10 years ending 2018 than in any decade because the Sixties.

- Lack of homebuilding displays partially tight regulatory restrictions in lots of elements of the nation. Most significantly, zoning legal guidelines, that are largely within the arms of native jurisdictions, limit housing density in numerous methods however particularly by way of limits on minimal lot sizes, and zoning for single-family housing solely. These caps have usually been carried out on the request of native residents (see right here). Typically dubbed “NIMBYs” (for “not in my backyard”), such residents are involved that better housing density and a rising presence of lower-income households of their neighborhoods will decrease their residence values by resulting in aesthetic blight, extreme demand for native facilities and infrastructure, and better crime.

- Extra just lately, larger rates of interest since 2022 have exacerbated these secular tendencies to make housing much more unaffordable. The mortgage price on a 30-year residence mortgage soared from 3 ½ % in early 2022 to just about 8% in October 2023 because the Federal Reserve raised coverage rates of interest; the mortgage price had solely eased to about 7% by March 2024 because the tightening cycle had peaked. The issue is compounded by mortgage lock-in: larger rates of interest have left many householders — lots of whom purchased houses or refinanced on the lows of 2020-21 — with cheaper-than-market mortgages, reluctant to promote their home and reset their mortgage at present, larger charges. Would-be homebuyers immediately due to this fact face each excessive costs and onerous financing prices. That is particularly an issue for first time consumers — like 70% of Millennial consumers —who haven’t any residence fairness to roll into their subsequent buy.

- The post-pandemic pattern in the direction of elevated earn a living from home additionally impacts housing affordability. Some current analysis argues that working from residence will increase housing demand — as an illustration by rising the necessity for residence places of work — and places upward strain on home costs and rents (with a commensurate decline in industrial property costs and rents). On the identical time, the elevated flexibility in working from residence makes doable the expansion of ‘zoom towns’ which might be additional away from unaffordable cities and suburbs, reinforcing the pattern in the direction of convergence of housing prices throughout the nation.

What this Means:

Lack of housing affordability is a matter in many international locations, so it isn’t a uniquely American downside. And the complexity of the components affecting housing affordability means that there isn’t a straightforward technique to treatment the issue. However, there could also be some prospect for reduction over time for Individuals. Within the close to time period, the anticipated reversal of the Fed’s tightening cycle beginning later this yr is anticipated to decrease mortgage charges serving to cost-burdened households whereas additionally boosting provide by dampening the mortgage lock-in impact. Over the medium-term, the swell of millennials and boomers driving excessive family formation is about to subside and decline. An extended-run answer to reversing the regular decline in housing affordability — or least conserving it in test — rests on elevated provide (although some analysis suggests that offer restrictions have performed a much bigger function in boosting home costs than rents). There are some encouraging indicators of willingness to alter zoning legal guidelines and permit better development of inexpensive housing in city facilities. Certainly, there has already been some improve in multifamily housing begins lately. A big pipeline of flats beneath development is about to hit the market over the approaching months; this might assist ease a few of the strain on rents. Coverage actions that mix tax incentives to encourage better provide of inexpensive housing can nudge this course of alongside. Homebuilders can also innovate in an effort to create extra inexpensive housing. Whereas these current steps are encouraging, the secular forces which have pushed down housing affordability appear unlikely to rapidly reverse, conserving the problem excessive on the coverage agenda.