I feel the title makes it clear that this will likely be a rambling confused put up. I’m typing on with the thought that one thing is healthier than nothing and nobody has to learn this.

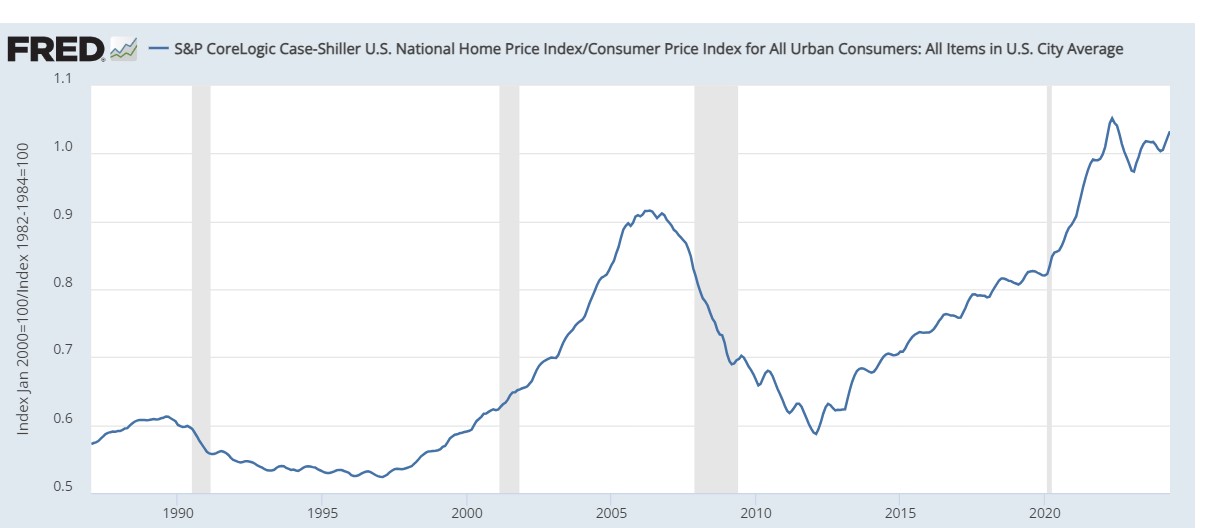

The primary subject – home costs, is in actual fact one which pursuits me so much. I’ve a regressin which suggests {that a} excessive ratio of home costs to the overall value stage is horrible information, as a result of it signifies a housing bubble which can burst and be adopted by a chronic recession.

At present the ratio of the Case-Shiller housing value index to the CPI is greater than it was in 2006.

I don’t need to jinx the financial system (my predictions are virtually all the time unsuitable) however I’m not terrified. I feel that this time it’s completely different. This time there has additionally been an enormous enhance in hire additionally relative to the quickly growing basic value stage. This implies that top housing costs are resulting from a real scarcity not hypothesis.

HIgh rents additionally imply that the worth of housing providers is excessive. Individuals paying a excessive down cost and really excessive mortgage funds because of the mixture of a excessive home value and excessive mortgage rates of interest have unatractive alternate options. In econospeak the worth of the housing providers they acquire is excessive.

I rely extra on vibes than numbers (and I admit it). There aren’t the standard signs of a bubble which embody lots of speak about capital good points, individuals explicitly shopping for planning to promote quickly for a better value (flip) individuals getting into the market who didn;t take part earlier than (the place right here the market is for second houses).

Additionally individuals complain in regards to the excessive costs. A excessive value is unhealthy for the customer and good for the vendor, and likewise unhealthy for somebody who plans to purchase sooner or later and good for somebody who can promote. I learn in regards to the complaints of determined consumers not the gloating of seellers.

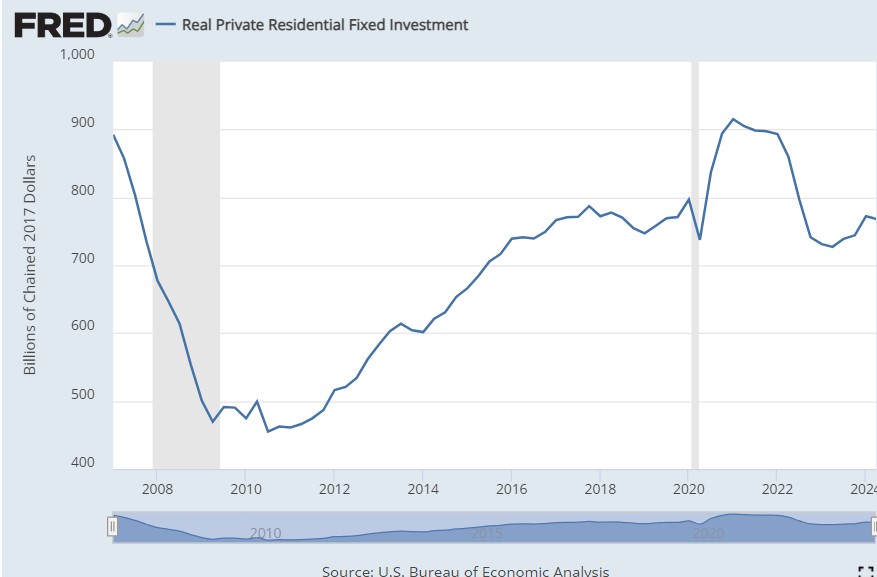

The excessive demand at excessive costs can be crucial proper now. I signifies that residential funding has remained pretty excessive regardless of excessive rates of interest (together with the mortgage rate of interest which is the one what issues for housing demand).,

This is essential. The principle methods wherein financial coverage impacts the actual financial system is thru residential funding which is low if rates of interest are excessive and thru change charges. Given the simultanious shift to tight anti-inflation coverage in wealthy international locations, the best way that the FED’s anti-inflation efforts would have an effect on actual GDP and employment is generally residential funding.

The third channel is funding in non-residentia constructions that are principally workplace constructing and buying malls (manufacturing unit buildings are giant however low-cost).

However wait, if excessive rates of interest didn’t have an effect on mixture demand, how did they trigger the dramatic decline in inflation ? I feel they didn’t. I feel that top inflation was resulting from Covid disruptions and never extraordinarily excessive mixture demand and that it declined although the housing scarcity brought about financial coverage to be ineffective.

That’s I observe Krugman (as all the time — it’s actually embarrassing) and name the excessive inflation lengthy termporary – one thing that lasted years however was destined to fade away by itself.

Which means that I ascribe the FED’s gentle touchdown triumph to pure luck.

It additionally signifies that I hope with some confidence that the touchdown will likely be gentle

(RJW confidence is a really alarming main indicator – I’m virtually all the time unsuitable).