With lower than three weeks till the U.S. presidential election, thousands and thousands of Individuals say the financial system is a high challenge as they determine how you can solid their vote — an comprehensible focus after the rollercoaster of the previous 4 years, which included every part from a bear market to the hottest inflation for the reason that Eighties.

However with the chaos of the pandemic behind us and inflation edging near its pre-2020 ranges, the U.S. financial system is ripe for a recent evaluation of its strengths and weaknesses, together with whether or not the Biden administration’s financial insurance policies have paid off.

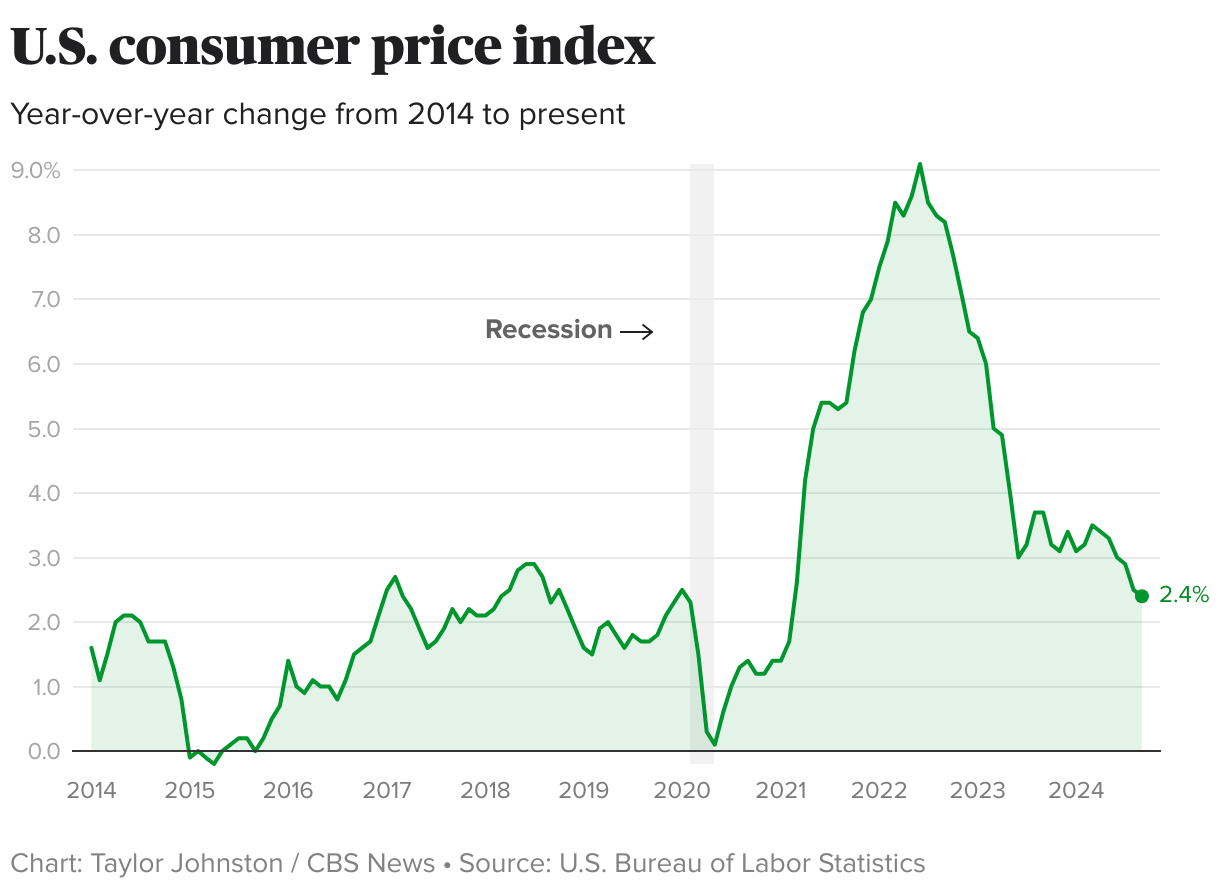

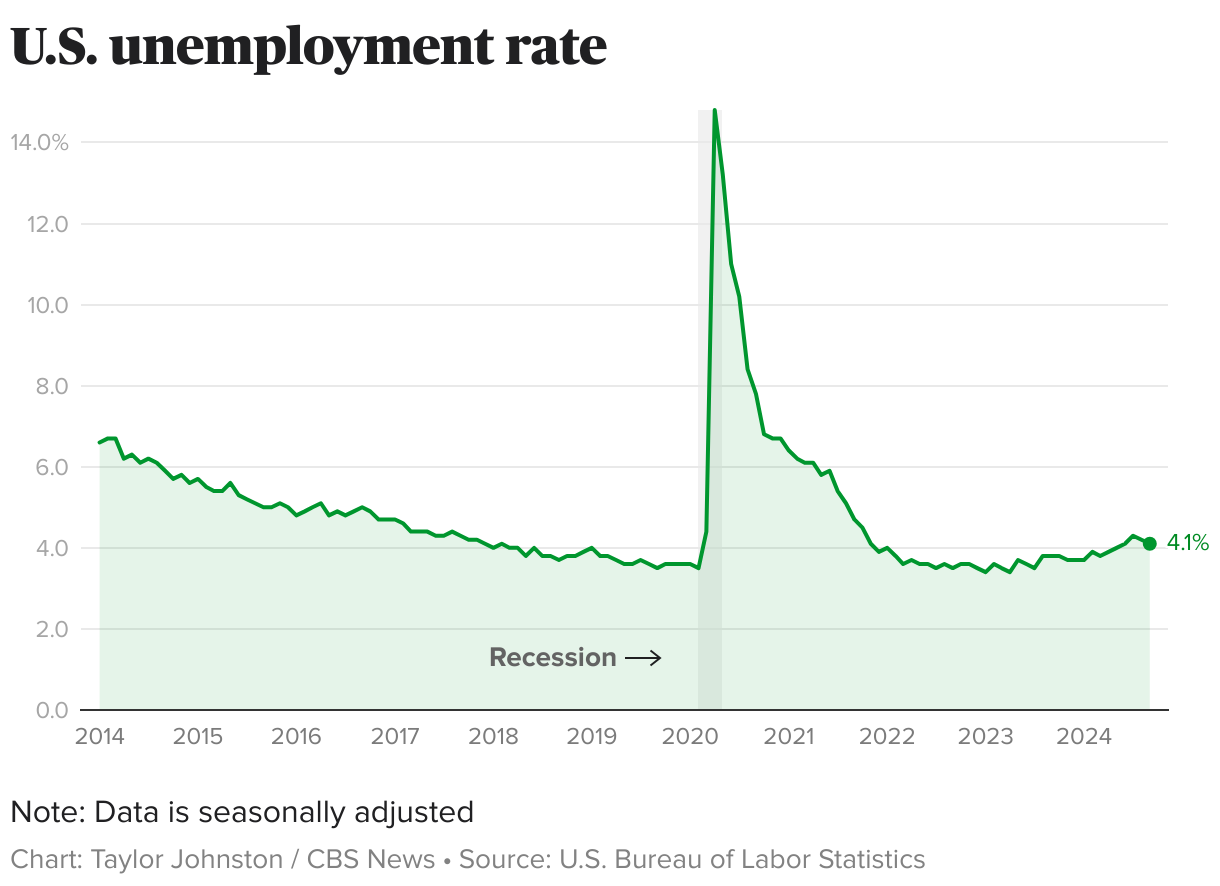

By many measures, the U.S. financial system has regained its footing, rising from the well being disaster with the kind of progress that it skilled previous to 2020. Gross home product is rising solidly, whereas unemployment and the labor market have additionally rebalanced, remaining near their pre-pandemic ranges. Critically, inflation has dropped to a three-year low and is approaching the Federal Reserve’s annual goal of two%.

To the shock of many forecasters, that rebound occurred even because the Fed boosted rates of interest to a 23-year excessive in an effort to chill inflation. Traditionally, such charge hikes have usually led to recessions. However to this point, the U.S. has averted a downturn, and as a substitute seems heading for a “soft landing,” or when the financial system continues to develop and the job market stays sturdy regardless of the headwinds of upper charges.

“In the 35 years I’ve been an economist, I’ve rarely seen an economy performing as well as it is,” Mark Zandi, chief economist of Moody’s Analytics who has beforehand suggested presidential candidates from each events, instructed CBS MoneyWatch. “I’d give it an A+.”

Like Zandi, many different consultants are giving the financial system sturdy marks. The U.S. financial system is “hot, hot, hot,” famous Yardeni Analysis in an October 17 report. The job market is “resilient” and “there is no quit in the U.S. consumer,” analysts at Oxford Economics instructed buyers this week.

But many Individuals would possibly scoff at such bullish assessments: 6 in 10 now describe the U.S. financial system as both “fairly bad” or “very bad,” based on CBS Information polling.

That’s not misplaced on Zandi and different economists. “The difference between the happy talk of economists and what people say has never been this wide,” he famous.

Why Individuals give the financial system poor marks

Just one in 10 Individuals charge the financial system as “very good,” based on CB Information ballot of registered voters taken between October 8-11. In the meantime, about 52% of Individuals say they and their household are worse off at the moment than they have been 4 years in the past, Gallup present in a new ballot.

“Despite recent economic data suggesting the labor market, consumer spending and the overall economy are proving to be very resilient and strong, consumers’ sentiment about economic conditions and future prospects remain downbeat,” Kathy Bostjancic, chief economist at Nationwide, instructed CBS MoneyWatch.

The discordant financial views amongst consultants and typical Individuals displays a number of components. First, and maybe most urgent within the short-term, costs across the U.S. stay elevated even because the searing inflation that adopted the pandemic descends to regular ranges.

Second, economists tasked with the complexity of deciphering a $29 trillion financial system naturally depend on broad metrics reminiscent of GDP, the Shopper Worth Index and the nation’s unemployment charge.

But such knowledge, even when bolstered with shopper confidence surveys and different public sentiment measures, don’t seize the much more nuanced monetary realities going through households. For a lot of Individuals, their perceptions are formed much less by fluctuations in progress charges or month-to-month job good points than by the extra palpable day by day battle to pay for meals, lease and well being care.

Third, mounting inequality in wealth and revenue has made successive generations of Individuals extra susceptible to financial crises on the identical time that conventional monetary milestones, reminiscent of proudly owning a house, turn out to be more durable to attain.

Lastly, polling means that political polarization is considerably coloring individuals’s views of the financial system. In such an atmosphere, a pointy disconnect between what the financial system seems like on paper and the way individuals expertise it isn’t solely unsurprising, however maybe inevitable.

An academic and occasion divide

Certainly, there are maor partisan and academic divides in how individuals assess the financial system, CBS Information polling reveals. For one, Republicans are more likely to provide the financial system poor marks than Democrats, a mirrored image of partisan views in regards to the path of the nation.

“If you are Republican, it doesn’t matter what you say — they don’t think the economy is good,” Zandi famous.

Virtually 9 in 10 conservatives describe the financial system as dangerous, in contrast with 3 in 10 individuals who lean liberal, CBS Information polling discovered. If former president Donald Trump wins in November, Zandi predicts that sentiment in regards to the financial system will shift, with liberal-leaning voters all of the sudden souring on the financial system and conservatives changing into extra upbeat.

However there’s one other divide that factors to the longer-term inequality points within the U.S.: a spot between individuals with and with out faculty levels. Individuals with out a bachelor’s diploma are way more detrimental in regards to the financial system than these with a school schooling — a disparity which will level to a long time of lagging wage progress for employees with solely highschool levels.

As an example, 47% of White voters with a school diploma describe the financial system pretty much as good, in contrast with 29% of these with out a diploma, an 18 percentage-point hole, CBS Information polling discovered earlier this month.

Individuals with faculty levels have seen their revenue and wealth surge in the course of the previous a number of a long time, leaving non-college educated employees behind. The disparities are significantly acute for younger males with out a bachelor’s diploma, with Pew discovering that this group earned median incomes of $45,000 in 2023 — 22% lower than the identical group in 1973.

These employees are feeling the sting of inflation essentially the most acutely, Zandi stated. “Grocery, rents, gasoline took off largely because of the pandemic and the Russian war, and those are things that you need and are a good part of the budget of lower-income households, who are lesser educated.”

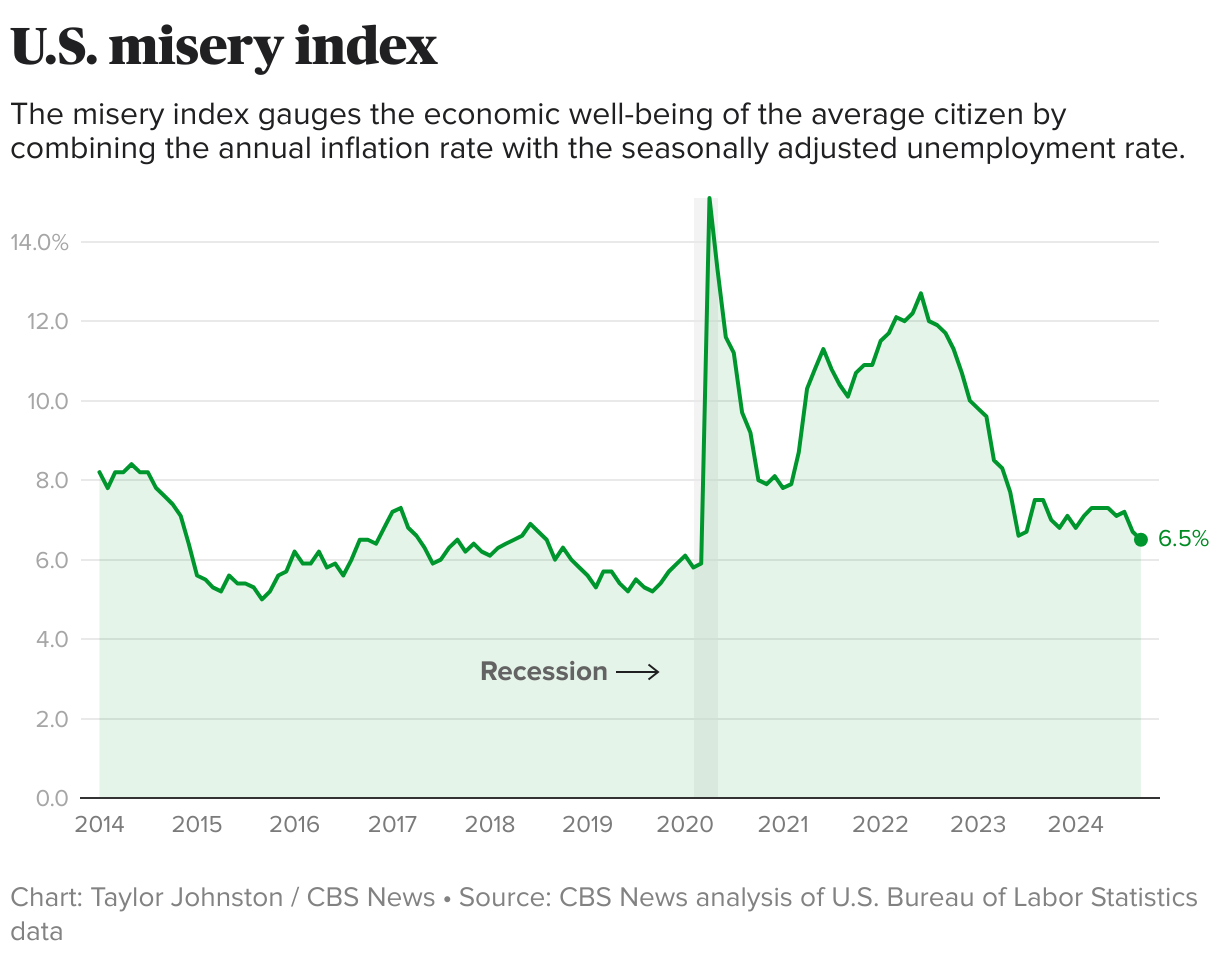

The “misery” index

One other technique to measure the financial realities of Individuals is the so-called distress index, which represents the sum of the unemployment and inflation charges. The thought is that greater unemployment and inflation will result in extra unhappiness, whereas decrease charges will scale back struggling.

The distress index, a casual measure adopted by economists, stood at 6.5% in September, beneath its common since 1947 of 9.1%, Ed Yardeni of Yardeni Analysis famous in a latest report.

“Should consumers be happier?” Yardeni requested.

Possibly, however Yardeni identified that Individuals are responding to greater than the inflation charge and the well being of the job market. Individuals additionally face many different monetary pressures, starting from excessive borrowing prices as a result of Federal Reserve’s interest-rate hikes to a sense of “precarity,” particularly amongst youthful voters who’re struggling to purchase their first house or pay faculty loans — points that aren’t tracked by the distress index.

Older Individuals, in the meantime, have drastically prospered from greater house values and a inventory market that continues to hit new highs, however half of them are additionally financially supporting their grownup kids, Yardeni famous.

“On average, parents providing financial support give $1,384 to their children monthly,” he stated. “That’s more than twice what the average working parent in the study contributed to his/her own retirement savings monthly.”

Decrease inflation, greater costs

Inflation, in the meantime, has dipped to a three-year low, hitting 2.4% in September, the latest Shopper Worth Index reveals. That’s not removed from the Fed’s aim of driving it right down to 2% on an annual foundation, opening the door to the central financial institution’s September charge lower, its first for the reason that begin of the pandemic.

However regardless of the Fed’s jumbo 0.5 share level lower final month, borrowing stays costly, together with for mortgages, which has priced many homebuyers out of the market.

“The reasons for the sour outlook are rooted in the prior surge in inflation that has greatly lifted the level of prices for goods and services, including for homes and rents, and the still-high interest rate burdens facing particularly lower- and middle-income households,” Bostjancic stated.

As an example, groceries nonetheless value 26% greater than in January 2020 simply previous to the pandemic, a painful hit to the pockets every time shoppers top off on meals.

“Almost everyone has a food item they purchase on a regular basis they use as a litmus test for everything they view about economy, and they are paying more than they did four years ago,” Zandi stated. “A pound of sugar, ramen noodles — even though the price of those things haven’t risen much over the last year, they are 20-25% higher than they were four years ago.”

Costs “aren’t going back to what they were,” he added. “That’s what people feel.”

Employment and wages

The U.S. unemployment charge stays close to a 50-year low, though it has inched up barely in latest months, which is one motive the Fed opted to chop charges final month.

Hiring is slowing however stays comparatively sturdy, with employers including 254,000 jobs in September, blowing away economists’ forecasts. The U.S. is creating about 150,000 to 175,000 new jobs per thirty days on common, Zandi stated, which he described as “extraordinary.”

“When you look at forecasts before the pandemic of job growth, it would be 75,000, not 150,000,” he famous.

In the meantime, employees’ wages have edged forward of inflation since Might 2023, giving workers some aid. But it surely won’t be sufficient to offset the ache of excessive costs.

“Even though income levels for households have also increased, many times catching up to the rise in inflation, consumers still reel at the sticker shock of higher prices,” Bostjancic stated.

Inventory market at report highs

Whereas the inventory market doesn’t replicate the financial system, rising asset costs have helped raise the monetary fortunes of thousands and thousands of Individuals. This 12 months, the S&P 500 has repeatedly hit report highs, offering good points to the 401(ok) plans and funding accounts of employees and retirees alike.

However solely 6 in 10 Individuals personal shares, in accordance to Gallup, and greater than half of employees lack entry to an employer-sponsored retirement plan.

These Individuals “aren’t benefiting from record stock prices,” Zandi stated.

Many are unaware that the inventory market has reached report heights, with solely 4 in 10 Individuals telling CBS Information that fairness costs are greater than at the beginning of the 12 months. About 3 in 10 say it’s decrease or the identical, whereas one other third say they’re uncertain.

“I have this metaphor in my mind that the economy is like an elephant, and depending on what you part you touch you can get a different sense” of what it’s, Zandi stated.