January CPI: a brand new paradigm, with the reappearance of some previous suspects

– by New Deal democrat

For sure, January’s improve of 0.5% in shopper costs was not welcome. And there was a altering of the guard considerably, as a number of of the previous suspects (meals and power) made new appearances.

Among the spike most likely has to do with unresolved seasonality. A variety of producers improve their costs originally of every yr, which reveals up within the graph under of CPI since mid yr 2022:

The very best bar on the graph is January 2023. January 2024 is just decrease than February of final yr. And this month’s change was the best since then. So, lots of what we have to search for are modifications within the YoY%, which is how virtually all the graphs under are offered.

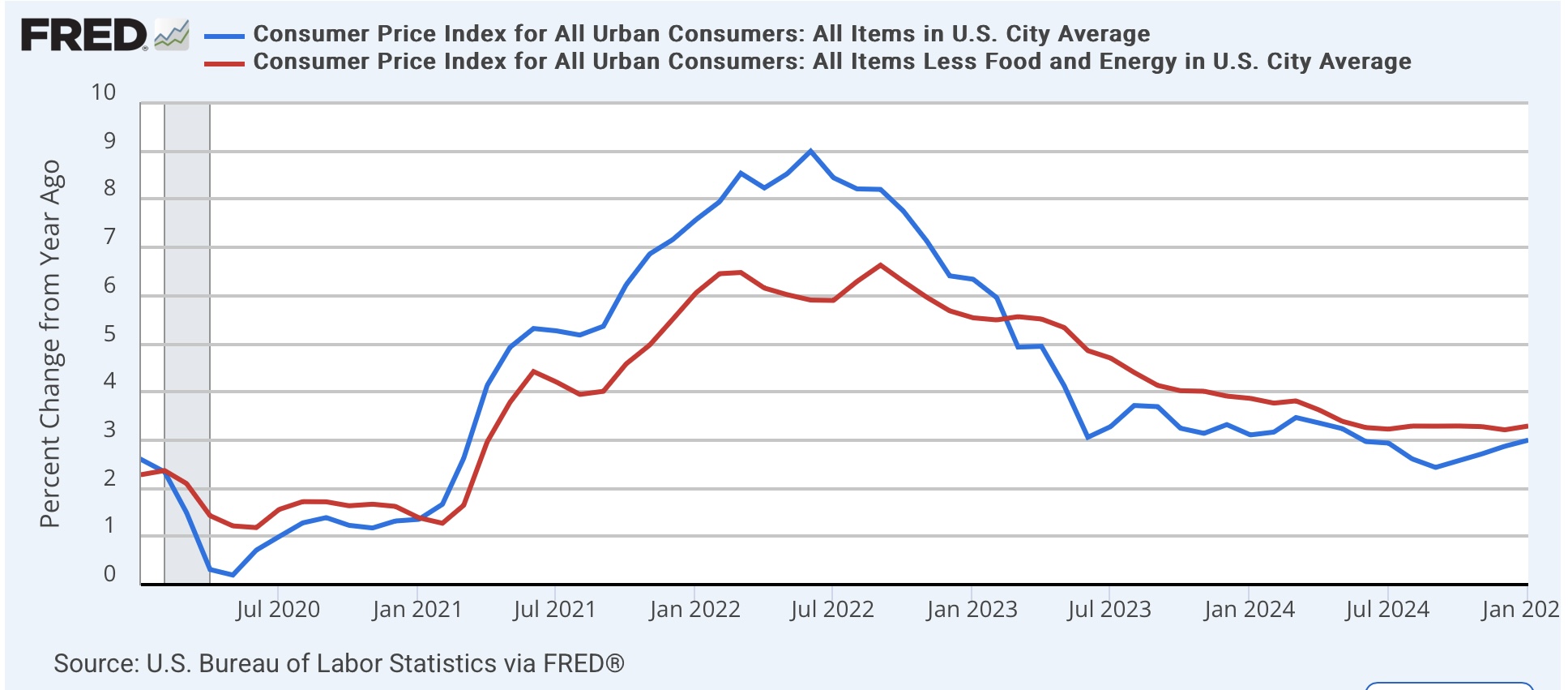

The elevated contribution of the previous suspects is clear within the graph under of core (crimson) vs. whole inflation:

Core inflation has been holding practically regular for a full yr, with modifications between 2.9% and three.2% (3.1% this month). It’s inflation in meals and power that has pushed the change in whole inflation. And though I received’t present particular graphs, meals inflation has loads to do with the worth of eggs (hen flu ensuing within the destruction of a lot of chickens) and the deflation in gasoline costs halting at roughly $3/gallon.

On the plus aspect, inflation in medical care providers was trying like a priority, however that has not less than leveled off:

And what about shelter? Properly, for the twentieth month in a row YoY inflation ex-shelter got here in at lower than 2.5%, though it did hit an eight-month excessive at 2.2%:

Each lease of main residence and homeowners’ equal lease continued their sluggish descent, hitting their lowest YoY ranges in virtually three years, at 4.2% and 4.6% respectively:

Though it didn’t decline this month, the downtrend in transportation providers inflation (motorized vehicle insurance coverage and repairs, in blue) additionally seems to be intact:

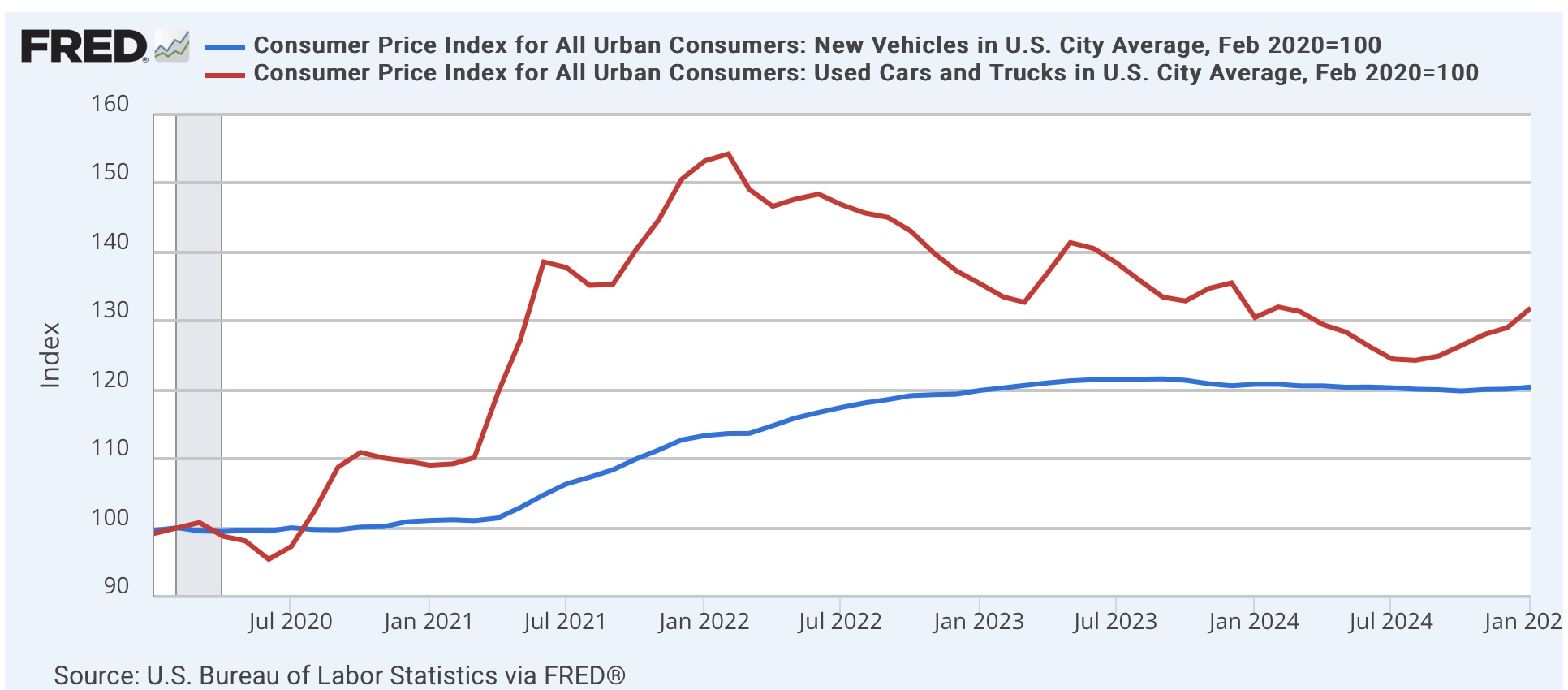

And the deflation in used automobile costs has positively ended, though new automobile costs are flat:

To sum up: whereas the very gradual deflation in shelter and to a lesser extent in transportation providers is useful, the definitive finish within the deflation of gasoline and used automobile costs, plus the spike in meals costs due primarily to hen flu has re-ignited shopper costs.

Lastly, right here’s an replace of certainly one of my favourite measures of common American well-being: actual mixture payrolls for nonsupervisory employees:

This declined in January and isn’t any higher than it was in September. On a YoY foundation, shoppers nonetheless have over 2% greater than they needed to spend a yr in the past:

And a multi-month stall like this isn’t unusual. However evidently, if it continues a number of extra months it’s going to start to flash an vital recession watch sign.

The Bonddad Weblog by New Deal democrat

December CPI: rebounds in gasoline and automobile costs outpace deceleration in shelter and insurance coverage laggards, Offended Bear by New Deal democrat