– by New Deal democrat

The JOLTS survey parses the roles market on a month-to-month foundation extra totally than the headline employment numbers within the jobs report. In July, it painted an image of what seems to be like fairly relentless deterioration.

The theme for 3 of the 4 knowledge collection I monitor was the identical: job openings, hires, and quits, all had their lowest or second lowest readings because the begin of 2021. Within the case of the “second worst” hires and quits numbers, it was solely as a result of final month’s numbers had been even decrease.

Particularly, job openings (blue within the graph beneath), a gentle statistic that’s polluted by imaginary, everlasting, and trolling listings, declined 227,000 to 7.623 million. Precise hires (pink) rose 273,000 to five.521 million (vs. a pre-pandemic peak of 6.0 million). Voluntary quits (gold) rose 63,000 to three.277 million. Within the beneath graph, they’re all normed to a stage of 100 as of simply earlier than the pandemic:

Each hires and quits are considerably beneath their rapid pre-pandemic readings, by -7.9% and -5.4% respectively.

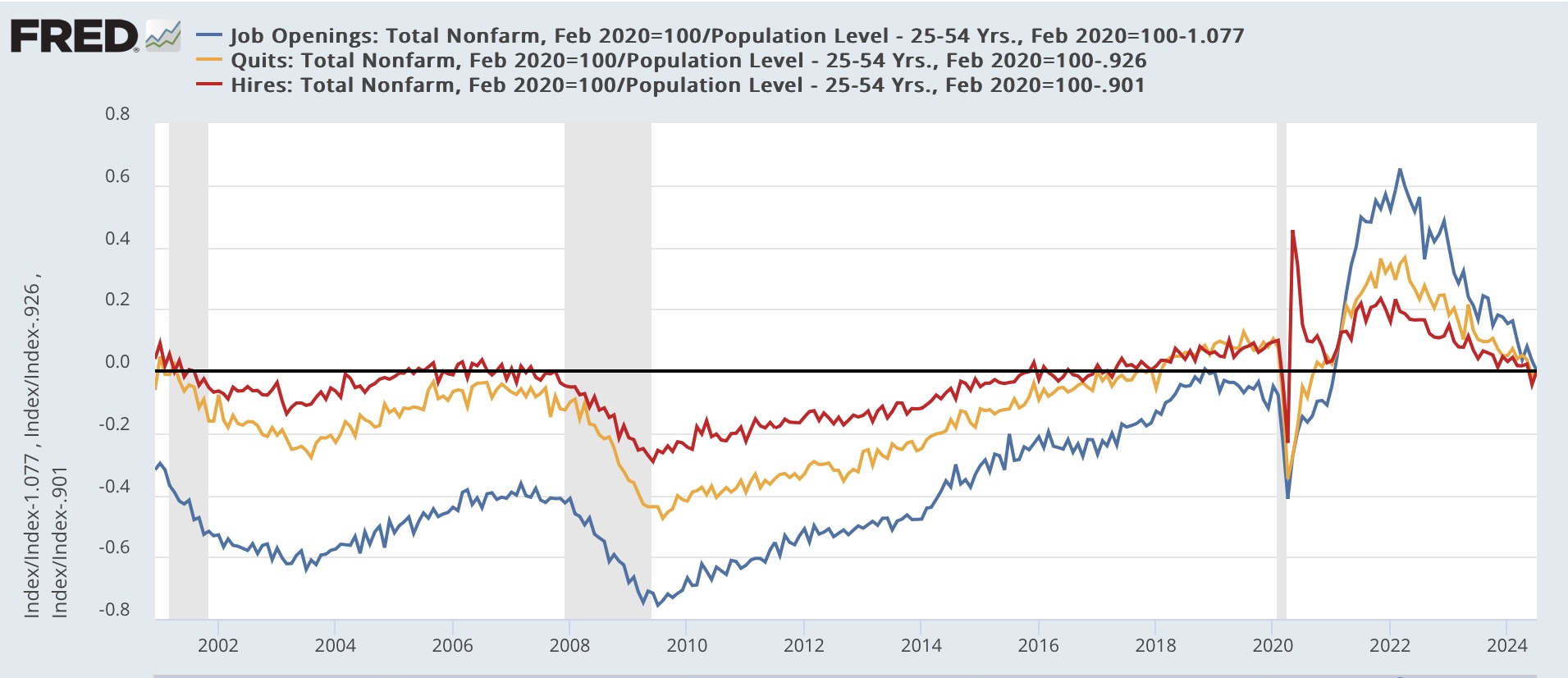

To place them in a wider historic context the beneath graph reveals all three collection from their inception in 2001. However as a result of the US inhabitants has grown nearly 20% since then, I divide by the prime age inhabitants over the identical time. I’ve additionally normed the present values to the zero line to higher present the historic comparability:

On the one hand, hires, even on a inhabitants adjusted foundation, are higher than nearly any time earlier than the pandemic besides 2005-06 and 2017-19. However notice they’re additionally at a stage equal to through the 2001 recession. Quits are higher than at any time earlier than the pandemic aside from simply earlier than the 2001 recession and 2018-19. This means to me that the actual, “hard data” jobs market remains to be optimistic, and never weak by historic requirements. It’s simply not as robust as we’ve turn out to be accustomed to over the previous a number of years.

In the meantime, layoffs and discharges elevated to their highest stage since late 2020 aside from a number of months in early 2023:

The above graph additionally reveals the month-to-month common of preliminary jobless claims (pink). It seems that layoffs and discharges did choose up the post-pandemic seasonality proven within the summer season enhance throughout Could by July.

Lastly, the quits charge (blue within the graph beneath) has a file of being a number one indicator for YoY wage features (pink). For over half a yr the quits charge had stabilized. That has now not been the case prior to now two months, because it is also at its lowest level since late 2020:

As you may see above, this forecasts continued deceleration in nominal wage features, down to three.5% YoY and even decrease within the coming months. Until shopper inflation moderates additional as nicely, it will put some monetary strain on odd employees (not a unfavourable, simply considerably much less optimistic).

Jobs Report July 30, 2024. Time for the FED to Decrease Fed Charges – Indignant Bear