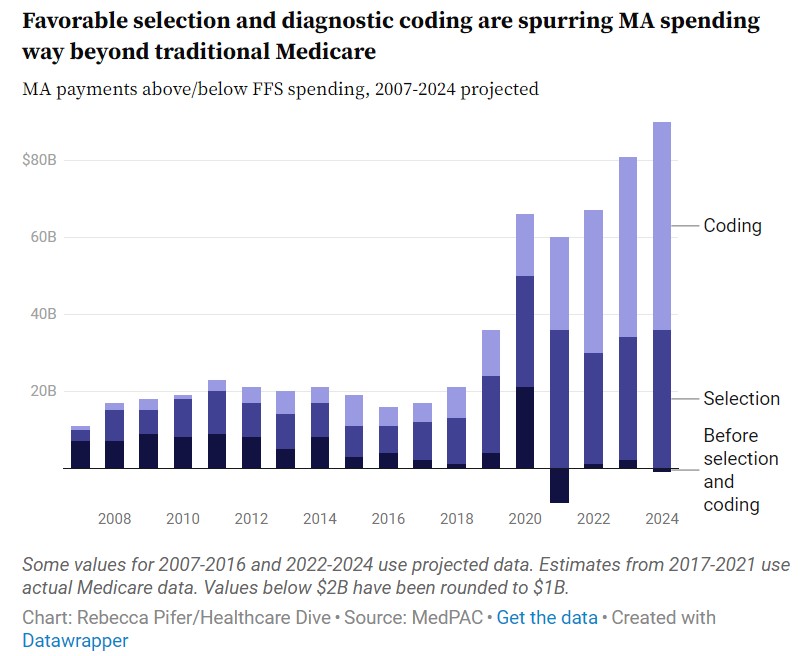

Medicare Benefit Plans are funded by Conventional Medicare which is slowly being depleted. A lot of what MA does which proves to be so pricey is because of MA up coding of its sufferers. It’s estimated this may price an ~$88 billion in 2024. That is up from $80 billion in 2023.

Research have discovered proof of upcoding and favorable collection of sufferers are driving important overpayments to MA plans. MedPAC additionally mentioned this system’s high quality bonus system isn’t an excellent measure of plan high quality, becoming a member of different analysis teams who say the program wants reform.

But, main payers in MA are pushing again towards regulatory adjustments which might upset their golden goose. (MA will be twice as worthwhile for insurers than different kinds of plans). Suppose United Healthcare.

How Inexpensive is Medicare Benefit?

Healthcare insurance coverage supplier Elevance is suing the federal authorities to cease adjustments to how MA calculates high quality bonus rankings, whereas Humana is suing to halt cost audits.

The affordability of well being care companies has grow to be a serious subject for insured People due to limitations on protection. Regardless of their assured public protection, folks with Medicare additionally face affordability considerations. A full 19% of Medicare beneficiaries are thought-about underinsured, which means they spend at the very least 10% of their earnings on well being care bills apart from premiums.1 Certainly, 1 of the obvious causes for the recognition of Medicare Benefit (MA) plans, which now enroll greater than half of Medicare beneficiaries, is that they promise to make care extra inexpensive for his or her enrollees.2 With the vast majority of beneficiaries enrolled in MA as we speak being people with a low earnings, the affordability of care in MA is much more necessary. Nonetheless, a number of latest surveys increase questions on whether or not MA is succeeding on this regard.

MA plans help with the affordability of care by a number of mechanisms. In contrast to conventional Medicare (TM), MA plans should cap out-of-pocket bills below Elements A and B of Medicare. They need to additionally use their federal rebates to cut back enrollees’ bills, both straight by decrease premiums and cost-sharing or not directly by offering supplemental advantages that might cut back the prices of dental, imaginative and prescient, and different companies that TM doesn’t cowl. Along with additional funds for high quality, favorable choice, and intensive diagnostic coding, these extra funds end in MA plans costing the federal authorities roughly $2500 extra per beneficiary in 2024 than what it could have price to cowl related beneficiaries in TM.3

Nonetheless, a number of surveys of Medicare beneficiaries point out that the proportion of beneficiaries who discover their care inexpensive is not any higher in MA than in TM. In a 2022 survey of 1604 Medicare beneficiaries aged 65 years and older, 41% of MA enrollees mentioned they’d issues accessing well being care because of its prices, in contrast with 35% of beneficiaries in TM.1 This lack of serious variations between MA and TM persevered after stratifying by beneficiaries’ earnings. Related outcomes had been present in different research.4

In actual fact, some proof signifies that MA enrollees might have extra issues affording well being care. A 2024 survey of 3280 Medicare beneficiaries discovered a considerably bigger proportion of enrollees in MA than in TM mentioned they might not afford well being care they wanted due to co-payments or deductibles (12% vs 7%).5 A considerably bigger share of older adults in MA than in TM reported issues paying medical payments and paying off medical debt (21% vs 14%), which was notably true for older adults with center incomes (27% vs 16%).1 MA enrollees are additionally considerably extra possible than beneficiaries in TM to report delays in accessing companies due to the necessity for pretreatment approval, equivalent to prior authorization (22% vs 13%).5

One exception to this sample is amongst folks with low incomes who’re dually eligible for Medicare and Medicaid. A bigger share of dually eligible beneficiaries in TM than these in MA mentioned they delayed care because of its prices (10% vs 6%).6 But, by different affordability metrics, together with issues paying medical payments and bother getting wanted care, the share of dually eligible beneficiaries going through challenges affording wanted care is comparable between MA and TM.6

Survey outcomes additionally increase questions on whether or not the protection of supplemental companies supplied by MA plans is making these companies extra inexpensive. Though protection for dental care is offered in nearly all MA plans and never in TM, older adults in MA are simply as possible as these in TM to say they didn’t use dental companies due to the prices (30% vs 24%), a discovering confirmed in different analysis.5,7 Likewise, dually eligible beneficiaries in MA had been as possible as these in TM to say they might not get wanted dental care (20% vs 18%).6 Nonetheless, this might not be true for different supplemental companies since dually eligible beneficiaries in MA had been considerably much less possible than these in TM to say they might not get wanted imaginative and prescient (7% vs 12%) or listening to (4% vs 8%) care.6

A number of elements might clarify these findings. Of TM enrollees with each Medicare Elements A and B, 41% have Medigap plans, which considerably help with the prices of Medicare deductibles and co-pays.3 Beneficiaries who both can not afford Medigap protection or can not get hold of this protection due to underwriting and preexisting circumstances might discover well being care extra inexpensive below MA plans. Beneficiaries with disabilities aged 65 years or youthful, who sometimes have decrease incomes than different beneficiaries, are one of many teams most affected by underwriting as a result of most states would not have assured subject rights for Medigap till beneficiaries flip age 65 years.

When accessing supplemental companies, MA enrollees could also be incurring related, surprising out-of-pocket prices. Sadly, there are scant accessible information on the generosity of protection accessible for supplemental advantages inside MA, the networks or circumstances that should be met for the profit to be coated, or the proportion of enrollees who incur out-of-pocket bills in utilizing them. Whether or not because of an incapacity to afford and entry the profit or lack of want for it, 30% of MA enrollees report not utilizing supplemental advantages of any sort.5

Restrictions on the suppliers utilized by beneficiaries in MA might trigger extra beneficiaries to hunt out-of-network companies for which they’ve little or no protection. TM sufferers don’t face such restrictions.

Denials or delays in protection ensuing from necessities for prior authorization below MA might trigger extra MA sufferers to pay out of pocket for denied or delayed companies. Right here once more, prior authorization is usually not required for companies coated by TM.

Caps on out-of-pocket bills in MA plans below Elements A and B of Medicare are excessive sufficient in most plans that solely a small proportion of enrollees exceed them. Thus, few MA enrollees profit from this plan requirement.3

Unmeasured affected person traits and expectations might issue into the survey outcomes. Favorable choice into MA and the advertising of plans as extra inexpensive might end in MA enrollees having totally different baseline expectations and perceptions of affordability than beneficiaries in TM. Since a bigger share of individuals with low incomes are enrolled in MA, the survey outcomes of MA enrollees might mirror the higher challenges that this inhabitants faces in affording care. But, even amongst folks with low incomes, the survey outcomes present few variations within the affordability of care between MA and TM.

Any shortcomings of MA plans in fixing the affordability downside shouldn’t obscure their sturdy factors. Survey respondents in TM and MA report related ranges of general satisfaction with their protection.5 For individuals who use them, the supplemental companies accessible below MA plans might have necessary well being and high quality of life advantages. Proof additionally means that MA plans could also be making some supplemental companies extra accessible for dually eligible beneficiaries.

However, given the upper prices of MA, and the requirement below federal legislation that plans use these additional funds to cut back enrollees’ bills, one may anticipate the perceived affordability of care below MA to be higher than below TM. Additional analysis ought to establish the explanations for this discovering, and what the federal authorities and well being plans can and will do to meet MA’s promise to make care extra inexpensive for its sufferers.

1. Leonard F, Jacobson G, Collins SR, Shah A, Haynes LA. Medicare’s affordability downside: a have a look at the price burdens confronted by older enrollees. Commonwealth Fund. September 19, 2023. Accessed July 3, 2024. https://www.commonwealthfund.org/publications/issue-briefs/2023/sep/medicare-affordability-problem-cost-burdens-biennial

2. Leonard F, Jacobson G, Haynes LA, Collins SR. Conventional Medicare or Medicare Benefit: how older People select and why. Commonwealth Fund. October 17, 2022. Accessed July 3, 2024. https://www.commonwealthfund.org/publications/issue-briefs/2022/oct/traditional-medicare-or-advantage-how-older-americans-choose

3. Medicare Cost Advisory Fee. Report back to the congress: Medicare cost coverage. March 2024. Accessed July 3, 2024. https://www.medpac.gov/wp-content/uploads/2024/03/Mar24_Ch12 MedPAC_Report_ To_Congress_SEC.pdf

4. Jacobson G, Cicchiello A, Sutton JP, Shah A. Medicare Benefit vs. conventional Medicare: how do beneficiaries’ traits and experiences differ? Commonwealth Fund. October 14, 2021. Accessed July 3, 2024. https://www.commonwealthfund.org/publications/issue-briefs/2021/oct/medicare-advantage-vs-traditional-medicare-beneficiaries-differ

5. Jacobson G, Leonard F, Sciupac E, Rapoport R. What do Medicare beneficiaries worth about their protection? Commonwealth Fund. February 22, 2024. Accessed July 3, 2024. https://www.commonwealthfund.org/publications/surveys/2024/feb/what-do-medicare-beneficiaries-value-about-their-coverage

6. Sutton J, Jacobson G, Leonard F. The well being care experiences of individuals dually eligible for Medicare and Medicaid: evaluating conventional Medicare and Medicare Benefit. Commonwealth Fund. June 27, 2024. Accessed July 3, 2024. https://www.commonwealthfund.org/publications/2024/jun/health-care-experiences-people-dually-eligible-medicare-medicaid

7. Simon L, Cai C. Dental use and spending in Medicare Benefit and conventional Medicare, 2010-2021. JAMA. 2024;7(2):e240401. doi:10.1001/jamanetworkopen.2024.0401 Article PubMed Google Scholar