Additionally depicted by Invoice McBride at Calculated Danger – MBA: “Mortgage Delinquencies Increase in Q2 2024”

WASHINGTON, D.C. (August 15, 2024) – The mortgage delinquency fee for mortgage loans on one-to-four-unit residential properties elevated to a seasonally adjusted fee of three.97 % of all loans excellent on the finish of the second quarter of 2024, based on the Mortgage Bankers Affiliation’s (MBA) Nationwide Delinquency Survey.

The delinquency fee was up 3 foundation factors from the primary quarter of 2024 and up 60 foundation factors from one 12 months in the past. The share of loans on which foreclosures actions have been began within the second quarter fell by 1 foundation level to 0.13 %.

Marina Walsh, CMB, MBA’s Vice President of Trade Evaluation . . .

“Mortgage delinquencies increased across all product types compared to this time last year. While delinquencies are still low by historical standards, the recent increase corresponds with a rising unemployment rate. Both have been historically closely correlated with mortgage performance.”

Walsh added,

“The composition of mortgage delinquencies by stage has evolved. As of the second quarter of 2024, the earliest stage delinquencies – those loans 60 days or less delinquent – accounted for the entire increase from the previous year. Meanwhile, seriously delinquent loans – those loans 90 days or more delinquent or in foreclosure – fell to their lowest levels since 1984 as servicers are helping at-risk homeowners avoid foreclosures through loan workout options that can mitigate temporary distress.”

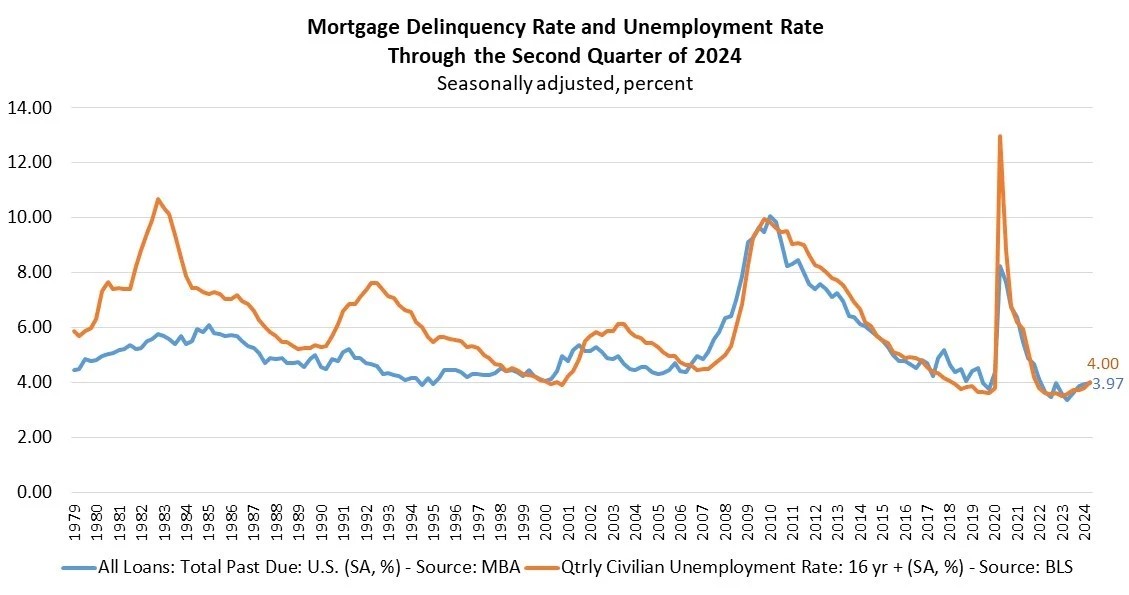

This graph exhibits all mortgage delinquencies (blue) and the Civilian Unemployment Fee (gold.). Invoice McBride’s graph at Calculated Danger refines the numbers to 30, 60, and 90 days delinquent and in foreclosures. General delinquencies elevated in Q2. The sharp improve in 2020 within the 90-day bucket was as a result of loans in forbearance (included as delinquent, however not reported to the credit score bureaus).

Key findings of MBA’s Second Quarter of 2024 Nationwide Delinquency Survey:

- In comparison with final quarter, the seasonally adjusted mortgage delinquency fee elevated for all loans excellent. By stage, the 30-day delinquency fee elevated 1 foundation level to 2.26 %, the 60-day delinquency fee elevated 3 foundation factors to 0.70 %, and the 90-day delinquency bucket decreased 1 foundation level to 1.01 %.

- By mortgage sort, the full delinquency fee for standard loans elevated 2 foundation factors to 2.64 % over the earlier quarter. The FHA delinquency fee elevated 21 foundation factors to 10.60 %, and the VA delinquency fee decreased 3 foundation factors to 4.63 %.

- On a year-over-year foundation, whole mortgage delinquencies elevated for all loans excellent. The delinquency fee elevated 35 foundation factors for standard loans, elevated 165 foundation factors for FHA loans and elevated 93 foundation factors for VA loans from the earlier 12 months.

- The delinquency fee consists of loans which are at the very least one fee late however doesn’t embody loans within the technique of foreclosures. The share of loans within the foreclosures course of on the finish of the second quarter was 0.43 %, down 3 foundation factors from the primary quarter of 2024 and 10 foundation factors decrease than one 12 months in the past.

- The non-seasonally adjusted critically delinquent fee, the share of loans which are 90 days or extra late or within the technique of foreclosures, was 1.43 %. It decreased 1 foundation level from final quarter and decreased 18 foundation factors from final 12 months. The critically delinquent fee decreased 2 foundation factors for standard loans, decreased 1 foundation level for FHA loans, and elevated 6 foundation factors for VA loans from the earlier quarter. In comparison with a 12 months in the past, the critically delinquent fee decreased 13 foundation factors for standard loans, decreased 54 foundation factors for FHA loans and decreased 8 foundation factors for VA loans.

- The 5 states with the biggest quarterly will increase of their total delinquency fee have been: Mississippi (58 foundation factors), Louisiana (54 foundation factors), Indiana (53 foundation factors), Ohio (53 foundation factors) and West Virginia (52 foundation factors).

For the needs of the survey, MBA asks servicers to report loans in forbearance as delinquent. If funds weren’t based on the unique phrases of the mortgage.

NOTE: For non-seasonally-adjusted (NSA) supplemental data on the efficiency of servicing portfolios by investor sort, loans in forbearance by investor sort, and the standing of post-forbearance exercises, in addition to servicer name quantity metrics, please discuss with MBA’s Month-to-month Mortgage Monitoring Survey at www.mba.org/lms. July 2024 outcomes will likely be launched on Monday, August 19, 2024.

")