There are seventy-one pages to this FTC report. My commentary seems at 5 edited (mine) pages of the report. The intent is to introduce you to Pharmacy Profit Managers (PBMs) and the management they’ve over the market. The companies they supply has been built-in with the healthcare insurance coverage corporations. Which makes this a dynamic twin for costs and earnings. Extra of the knowledge is depicted within the three charts I included under. Under no circumstances is this whole. The primary chart will present the linkage between all of the gamers.

It’s simply an excessive amount of for me to incorporate the complete commentary in a single and even a number of commentaries. I counsel you do learn the entire FTC report. Take note of web page 71 of the report which is a quick summation.

~~~~~~~~

This Report particulars how prescription drug intermediary revenue on the expense of sufferers by inflating drug prices and squeezing Major Avenue pharmacies.

Pharmacy Profit Managers: The Highly effective Middlemen Inflating Drug Prices and Squeezing Major Avenue Pharmacies, Federal Commerce Fee

Over the previous 20 years, pharmacy profit companies have turn into more and more concentrated. In 2004, the highest three PBMs served a mixed 190 million individuals and managed 52 p.c of prescription drug claims. As we speak, the highest three PBMs—CVS Caremark, Categorical Scripts, and OptumRx (collectively, the “Big 3”) handle 79 p.c of prescription drug claims for roughly 270 million individuals. The subsequent three largest PBMs—Humana Pharmacy Options, MedImpact, and Prime plus the earlier 3 PBMs (the “Big 6”) now handle 94 p.c of prescription drug claims in america.

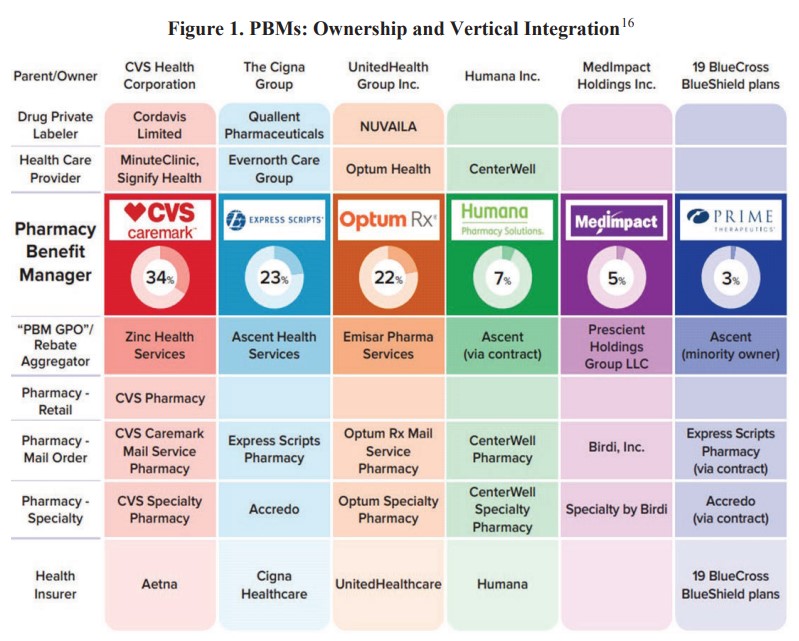

Moreover with this diploma of horizontal focus, the Large 6 PBMs have turn into vertically built-in inside large conglomerates present a broad vary of companies throughout the pharmaceutical provide chain and different segments of the healthcare sector Determine 1). Numerous PBMs at the moment are vertically built-in with upstream suppliers of products and companies, together with drug personal labelers and supplier teams. PBMs are additionally vertically built-in with midstream distributors, together with retail, mail order, and specialty pharmacies. Downstream, PBMs are vertically built-in with massive well being insurers which, by their well being plans and plan sponsor companies, present protection for a whole lot of thousands and thousands of People.

Determine 1 depicts such integration as recognized within the above paragraph.

This elevated focus and vertical integration ends in huge healthcare conglomerates exercising huge management over enormous swaths of the healthcare sector. 4 of the PBMs are a part of publicly traded healthcare conglomerates: UnitedHealth Group Inc. (“United” or “UHG”), CVS Well being Corp. (“CVS”), The Cigna Group (“Cigna”), and Humana Inc. (“Humana”).

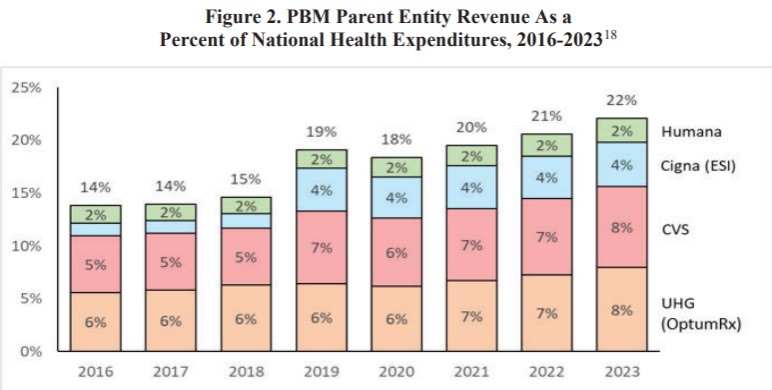

In 2016, the mixed income of those 4 conglomerates totaled $456 billion and equaled 14 p.c of nationwide well being expenditures in america. As we speak, their mixed income exceeds $1 trillion and equals 22 p.c of nationwide well being expenditures, as illustrated in Determine 2 under. On the similar time, the 4 entities additionally tremendously expanded their earnings as mixed adjusted working earnings and internet earnings grew by 133 and 159 p.c, respectively, over the 2016 to 2023 interval.

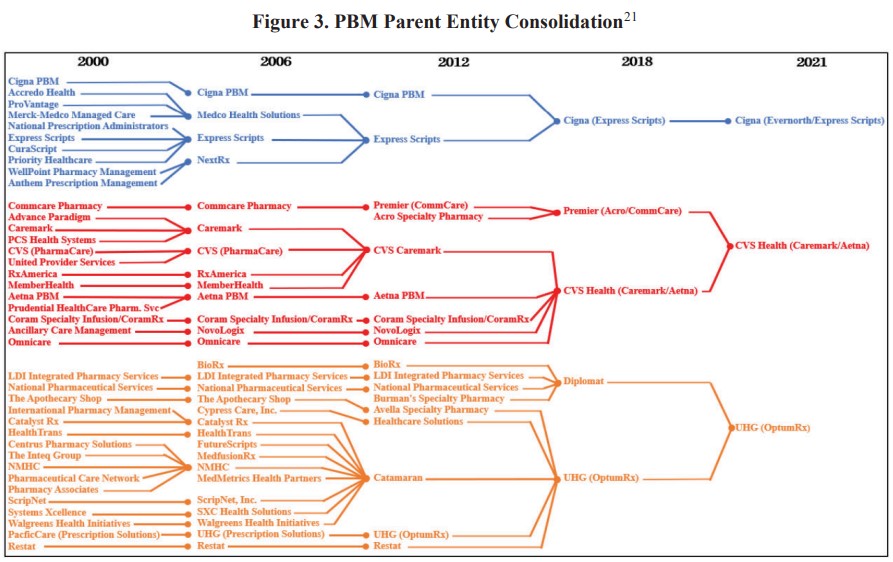

A lot of the expansion skilled by the 4 healthcare conglomerates in Determine 2 is pushed by mergers and acquisitions. In keeping with PitchBook, these 4 entities and their subsidiaries (which embrace the biggest PBMs) collectively engaged in additional than 190 transactions over the 2016 to 2023 interval (United, 88; CVS, 53; Humana, 39; and Cigna, 14). Illustrating the matter, the Arkansas Legal professional Common diagrammed among the mergers and acquisitions among the many Large 3 PBMs’ mum or dad entities between 2000 and 2021, as proven in Determine 3 under. For the 2 nonpublic PBMs in our research, PitchBook reported solely 4 acquisitions over the 2016 to 2023 interval (Prime, 3; MedImpact, 1)

Moreover, the healthcare conglomerates look like driving development by producing rising ranges of income from their vertically built-in associates. For instance, a research by the Brookings Establishment discovered that over the 2016 to 2019 interval, United’s share of spending related to its associates rose by greater than 250 p.c to 17 p.c of the corporate’s complete spending, and CVS’ share of affiliate spending elevated greater than five-fold to almost 13 p.c of complete spending.

Furthermore, there’s vital widespread possession of publicly traded shares of United, CVS, Cigna, and Humana, which might scale back incentives of corporations to compete and lift different aggressive considerations, because the Fee and the Division of Justice (“DOJ”) have beforehand defined. Shareholders with stakes in a minimum of three of those 4 corporations personal nearly one quarter of a trillion {dollars}, or 35.5 p.c, of the businesses’ mixed market worth, whereas shareholders with stakes in all 4 corporations personal 28 p.c.

The FTC does provide transient overviews of the companies supplied by PBMs and the varied vertically built-in items and companies provided by their mum or dad and affiliated entities. This may be discovered on web page 9 (beginning) of the FTC report.

")