by Invoice McBride

Intro: Former Indignant Bear author Invoice McBribe taking over the problems of Mortgage Delinquency, Foreclosures, and Actual Property Owned (REO) foreclosed housing. The worth of which decreased within the second quarter to (what Invoice calls) a traditionally low complete. Learn on.

We are going to NOT see a surge in foreclosures that might considerably impression home costs (as occurred following the housing bubble) for 2 key causes: 1) mortgage lending has been stable, and a couple of) most owners have substantial fairness of their houses.

Final week, CoreLogic reported on house owner fairness: CoreLogic: US Owners See Fairness Features Proceed to Climb, however at a Slower Tempo in Q2

The report reveals that U.S. householders with mortgages (which account for roughly 62% of all properties) noticed residence fairness improve by 8.0% yr over yr, representing a collective achieve of $1.3 trillion and a median improve of $25,000 per borrower because the second quarter of 2023, bringing the entire web house owner fairness to over $17.6 trillion within the second quarter of 2024. . . .

From the second quarter of 2023 to the [second] of 2024, the entire variety of houses in unfavorable fairness decreased by 15%, to 1.1 million houses or 2.0% of all mortgaged properties.

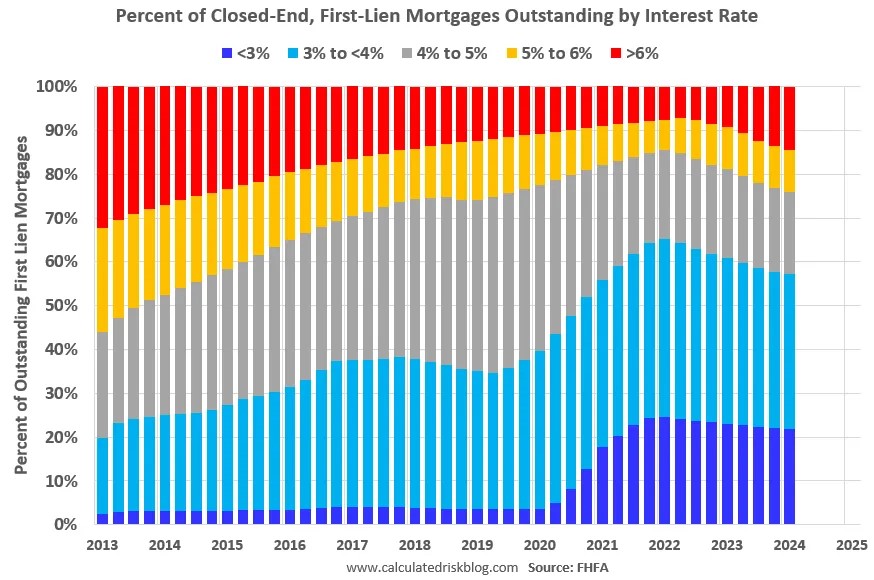

This reveals the surge within the % of loans beneath 3%, and likewise beneath 4%, beginning in early 2020 as mortgage charges declined sharply through the pandemic. At the moment 21.9% of loans are beneath 3%, 57.3% are beneath 4%, and 76.0% are beneath 5%.

With substantial fairness, and low mortgage charges (principally at a set charges), few householders could have monetary difficulties.

Some easy definitions (for housing):

Forbearance is the act of refraining from imposing mortgage debt.

Delinquency is the failure to make mortgage funds on a well timed foundation.

Foreclosures is when the mortgage lender takes possession of the property after the mortgagor didn’t make their funds. “In foreclosure” is the method of foreclosures.

REO (Actual Property Owned) is the quantity of actual property owned by lenders.

Right here is a few information on REOs by means of Q2 2024 . . .

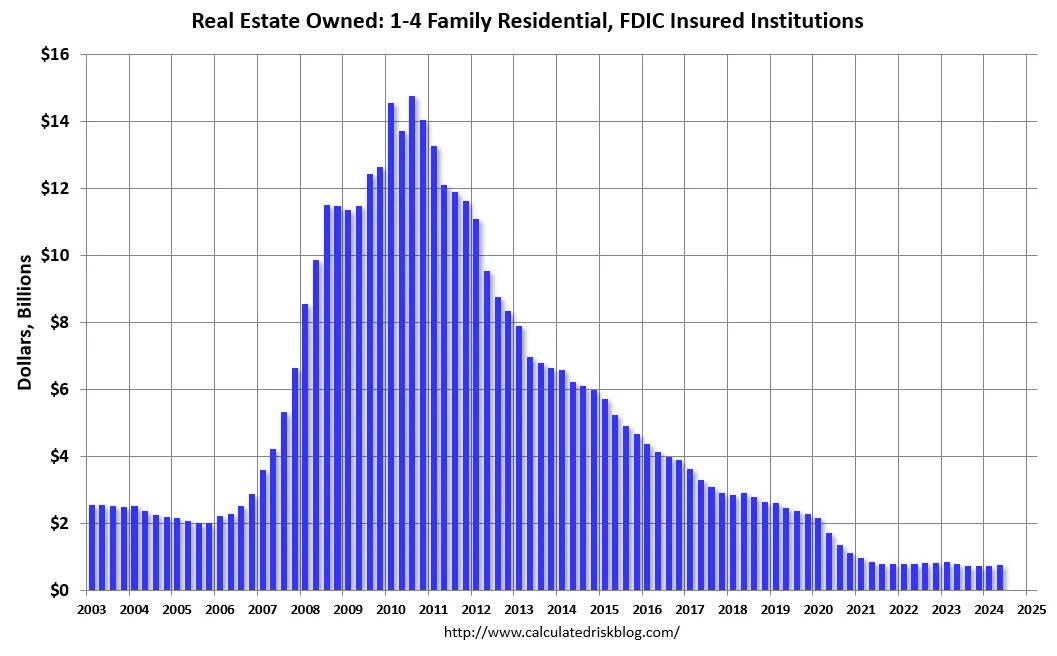

This graph reveals the nominal greenback worth of Residential REO for FDIC insured establishments based mostly on the Q2 FDIC Quarterly Banking Profile launched earlier this month. Word: The FDIC studies the greenback worth and never the entire variety of REOs.

The greenback worth of 1-4 household residential Actual Property Owned (REOs, foreclosures homes) decreased from $794 million in Q2 2023 to $766 million in Q2 2024. That is traditionally extraordinarily low.

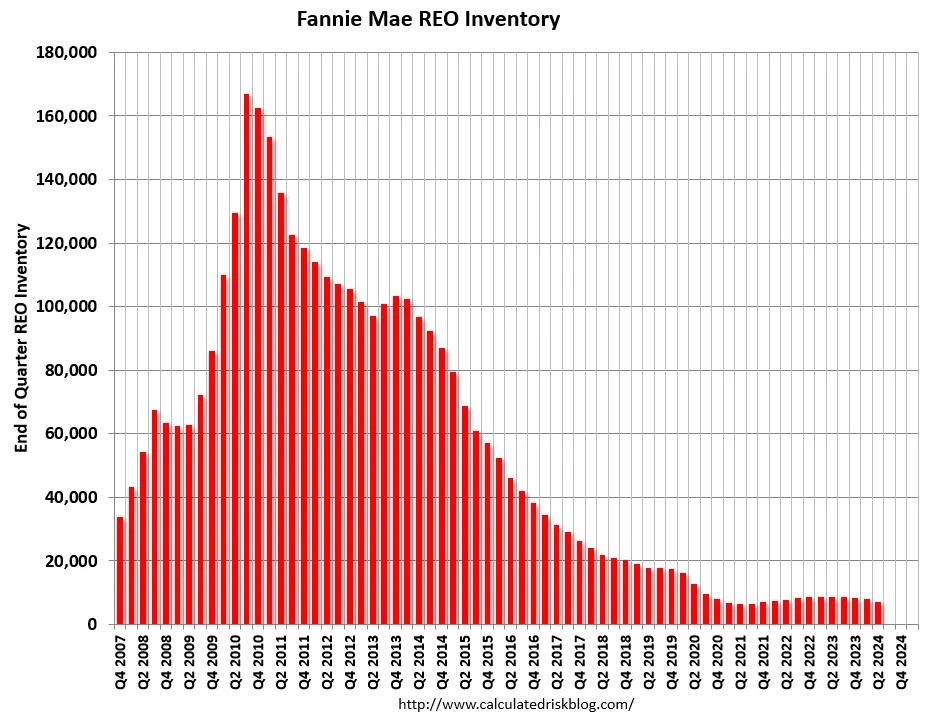

Fannie Mae reported the variety of REOs decreased to 7,179 on the finish of Q2 2024, down 10% from 7,971 on the finish of the earlier quarter, and down 17% year-over-year from Q2 2023. Here’s a graph of Fannie Actual Property Owned (REO).

That is very low and effectively beneath the pre-pandemic ranges. REOs are a lagging indicator. REOs improve when debtors battle financially and have little or no fairness, to allow them to’t promote their houses – as occurred after the housing bubble. That won’t occur this time.

Right here is a few information on delinquencies . . .

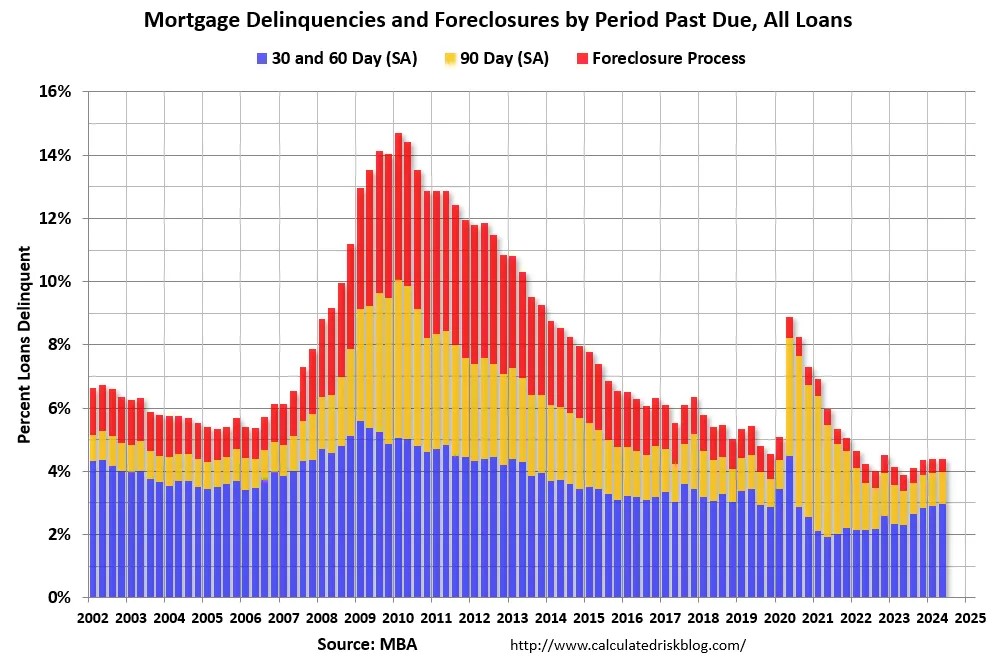

The % of loans within the foreclosures course of decreased year-over-year from 0.53 % in Q2 2023 to 0.43 % in Q2 2024 (crimson) and stays traditionally low. Loans in forbearance are principally within the 90-day bucket at this level, and that has declined not too long ago. From the MBA:

In comparison with final quarter, the seasonally adjusted mortgage delinquency fee elevated for all loans excellent. By stage, the 30-day delinquency fee elevated 1 foundation level to 2.26 %, the 60-day delinquency fee elevated 3 foundation factors to 0.70 %, and the 90-day delinquency bucket decreased 1 foundation level to 1.01 % …

The delinquency fee contains loans which are not less than one cost late however doesn’t embrace loans within the technique of foreclosures. The proportion of loans within the foreclosures course of on the finish of the second quarter was 0.43 %, down 3 foundation factors from the primary quarter of 2024 and 10 foundation factors decrease than one yr in the past.

emphasis added

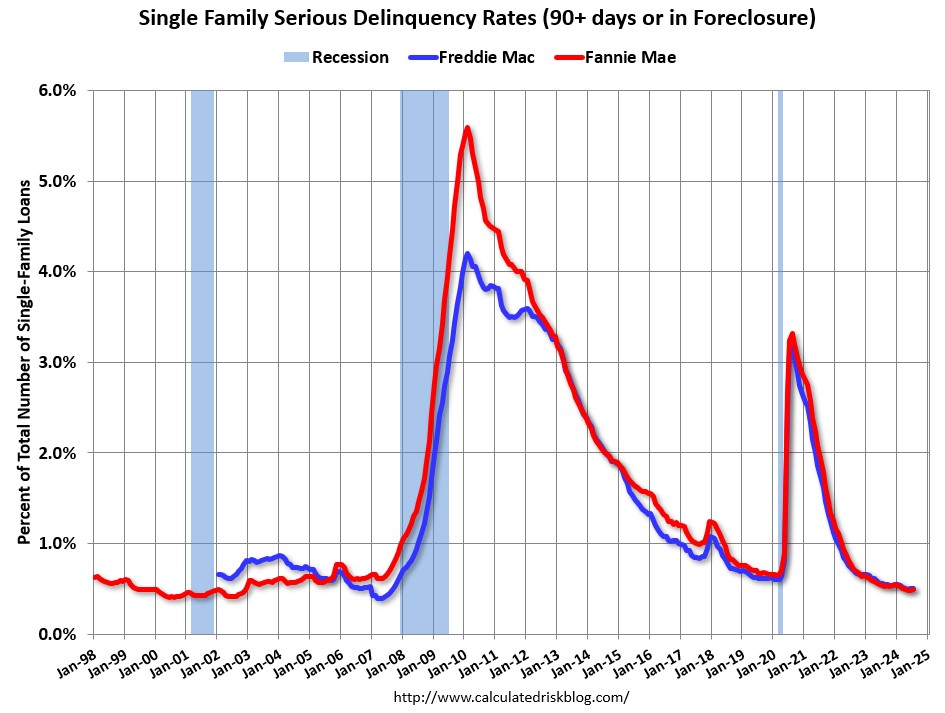

Each Fannie and Freddie launch severe delinquency (90+ days) information month-to-month. Freddie Mac reported that the Single-Household severe delinquency fee in July was 0.51%, up from 0.50% June. Freddie’s fee is down year-over-year from 0.56% in July 2023. That is beneath the pre-pandemic lows. Freddie’s severe delinquency fee peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 through the pandemic.

Fannie Mae reported that the Single-Household Critical Delinquency elevated to 0.49% in July from 0.48% in June. The intense delinquency fee is down year-over-year from 0.54% in July 2023. That is beneath the pre-pandemic lows. The Fannie Mae severe delinquency fee peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 through the pandemic.

This graph reveals the current decline in severe delinquencies:

The pandemic associated improve in severe delinquencies was very totally different from the rise in delinquencies following the housing bubble. Lending requirements have been pretty stable over the past decade, and most of those householders have fairness of their houses – and so they have been in a position to restructure their loans as soon as they have been employed.

And on foreclosures . . .

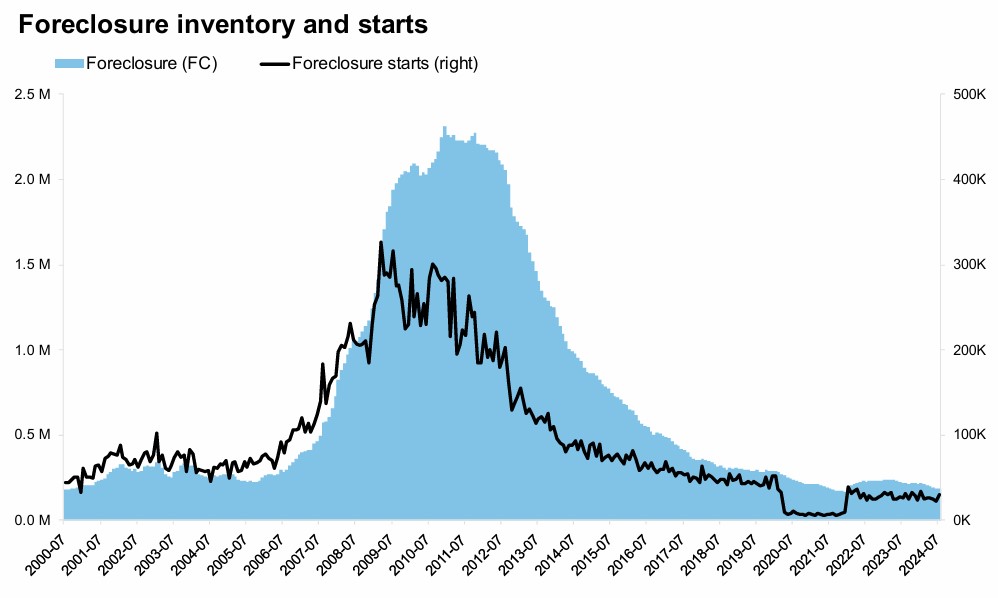

ICE reported that energetic foreclosures have decreased are close to the data. From ICE: ICE Mortgage Monitor: Fee drops make August most inexpensive month since February, as residence worth progress cools to 12-month low

- Foreclosures begins jumped by 32% in July, however that spike seems to be extra an indication of volatility in month-to-month referral volumes after coming off a submit moratorium low in June than a sign of broader danger out there

- Fewer than 30K loans have been referred to foreclosures within the month, which remains to be greater than 30% beneath 2019 ranges, with the variety of significantly delinquent mortgages additionally persevering with to run traditionally low

- Lively foreclosures stock nudged increased (+2K), however stays at its second-lowest degree since January 2022 and remains to be 34% beneath pre-pandemic ranges

- July foreclosures gross sales (5.5K) elevated +3.7% month-over-month, however have been down -9.6% from final yr and nonetheless lower than half of 2019 averages

- The nationwide foreclosures fee edged modestly increased in July as effectively, a month after hitting its lowest degree on document exterior of This fall 2021 on the tail finish of the nationwide foreclosures moratorium

The underside line is there won’t be an enormous wave of foreclosures as occurred following the housing bubble. The distressed gross sales through the housing bust led to cascading worth declines, and that won’t occur this time.