Report on the impression from the expanded unemployment insurance coverage, financial impression funds, assist to states and localities, little one tax credit, and momentary safety from eviction amongst different measures as reported by the authors. These actions supplied aid to staff and their households to assist them climate the recession. These measures additionally fed the surge in employment, wages, and gave low-wage staff higher job alternatives and leverage to see robust wage progress.

The graphs reveal the impression of the packages, The phrases element the outcomes So sure there may be some studying concerned apart from the graphs. I minimized as a lot of it as attainable with out impeding the report’s integrity.

~~~~~~~

Quickest wage progress during the last 4 years amongst traditionally deprived teams

by Elise Gould and Katherine deCourcy

Financial Coverage Institute

Quickest wage progress during the last 4 years amongst traditionally deprived teams: Low-wage staff’ wages surged after a long time of gradual progress, Financial Coverage Institute.

Actual wage progress on the Tenth percentile was exceptionally robust, even within the face of excessive inflation

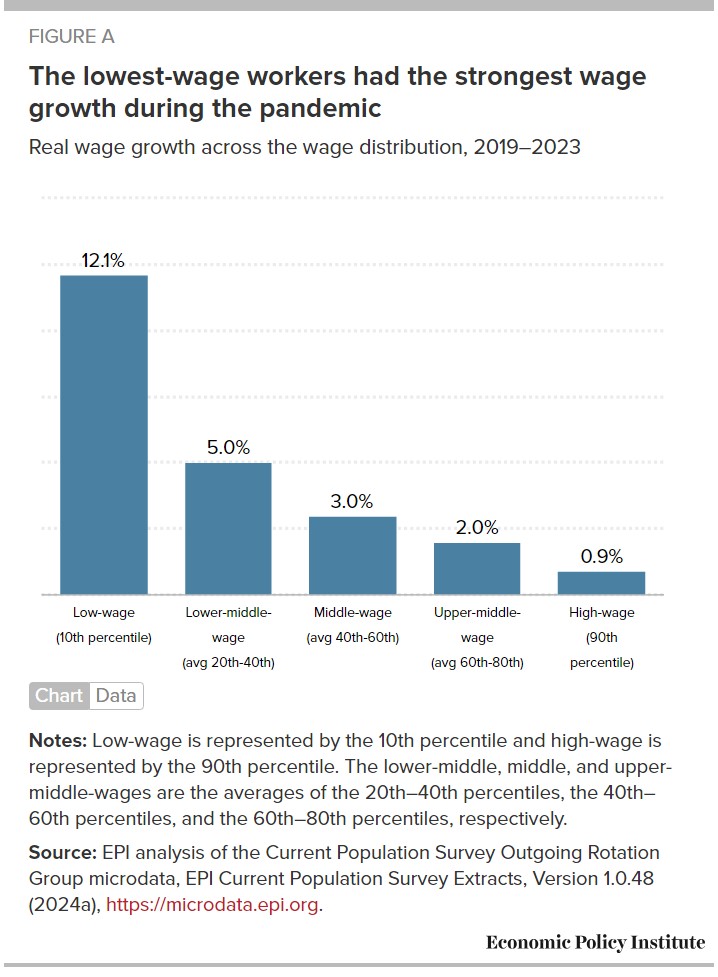

Wage progress strongest for low-wage staff between 2019 and 2023

On this evaluation, we divide the wage distribution into roughly 5 teams to uncover current wage tendencies at completely different wage ranges. Determine A shows wage progress on the Tenth percentile (“low-wage”), the typical of the twentieth–fortieth percentiles (“lower-middle-wage”), the typical of the fortieth–sixtieth percentiles (“middle-wage”), the typical of the sixtieth–eightieth percentiles (“upper-middle-wage”), and the Ninetieth percentile (“high-wage”) utilizing Present Inhabitants Survey (CPS) Outgoing Rotation Group microdata (EPI 2024a). Gould and deCourcy (2023) present a extra detailed dialogue of those information measures and their robustness. Notice that the Ninetieth percentile as “high-wage” doesn’t seize the earnings of these on the very prime and is best captured with different information units that are mentioned briefly afterward.

Our evaluation focuses on modifications in actual wages between 2019 and 2023, in addition to historic comparisons of actual wage modifications between 1979 and 2019. Our give attention to 2019 and 2023 permits us to largely ignore the dramatic swings in employment and wages in 2020 and 2021, which have been most impacted by the pandemic recession and preliminary restoration.1

Actual wage progress on the Tenth percentile was exceptionally robust—even within the face of excessive inflation

Between 2019 and 2023, hourly wage progress was strongest on the backside of the wage distribution. The Tenth-percentile actual hourly wage grew 12.1% over the four-year interval. To be clear, these are actual (inflation-adjusted) wage modifications. Total inflation grew almost 20%, or about 4.5% yearly, between 2019 and 2023. Even with this traditionally quick inflation, notably within the fast aftermath of the pandemic recession, low-end wages grew considerably sooner than worth progress. Nominal wages (i.e., not inflation-adjusted) rose by roughly 34% cumulatively since 2019.

Throughout the wage distribution, we see the tempo of wage progress declining for every successive wage group. In contrast with the 12.1% wage progress on the backside, progress was lower than half as quick for lower-middle-wage staff (5.0%) and fewer than one-third as quick for middle-wage staff (3.0%) between 2019 and 2023. Higher-middle wages grew 2.0% over the four-year interval, whereas the Ninetieth-percentile wage grew even slower at 0.9%.

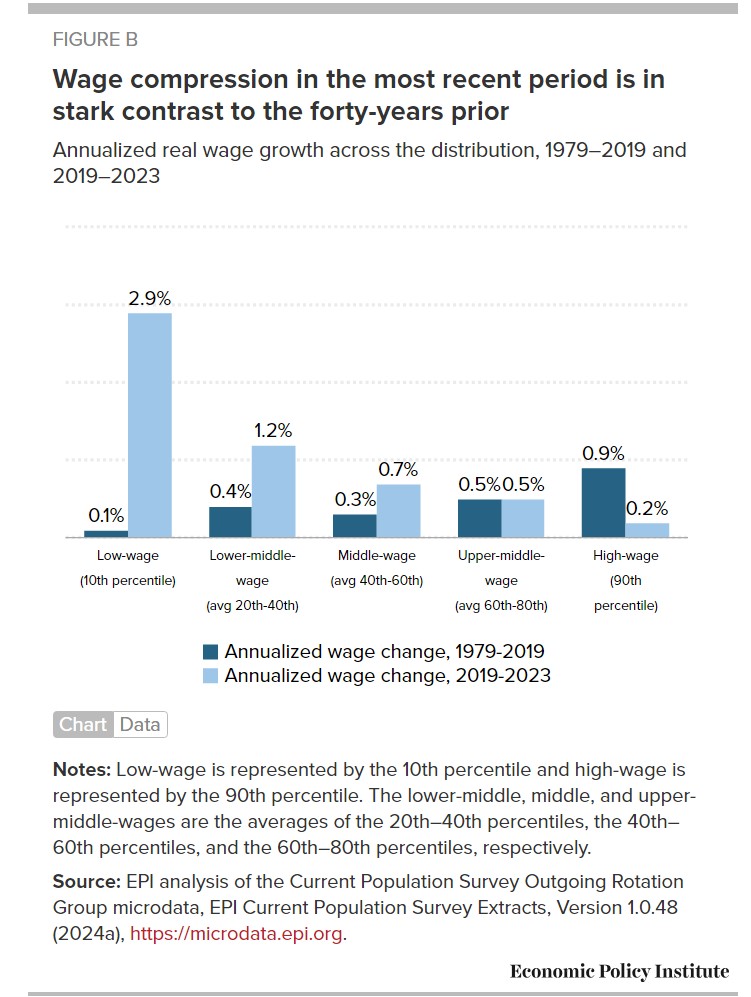

Wage compression in the latest interval contrasts sharply with prior 40 years

As a result of wages grew a lot sooner on the Tenth percentile than on the different 4 factors, we measure inside the twentieth to Ninetieth percentiles, wage compression has occurred. These findings—disproportionately robust wage progress on the backside resulting in wage compression—are according to the opposite analysis (see, as an illustration, Autor, Dube, and McGrew 2023).

This wage compression between 2019 and 2023 is in stark distinction with the expertise of staff within the prior 4 a long time. Determine B shows wage progress between 2019 and 2023 in comparison with wage progress between 1979 and 2019 for a similar 5 wage groupings: low-wage, lower-middle-wage, middle-wage, upper-middle-wage, and high-wage. This time we report annualized wage modifications in wages—which permit for comparability throughout intervals which span completely different numbers of years, e.g. a four-year span versus a forty-year span.2

The variations in wage progress between these intervals are hanging. Whereas in the latest interval wage progress was stronger amongst every successive decrease wage group, the alternative sample happens within the earlier forty-year interval. Every successive greater wage group shows wage progress not less than as quick because the earlier one, aside from between the lower-middle to the middle-wage group the place there’s a small lower.

In the latest interval, middle-wage staff expertise progress greater than three-times sooner than excessive wage staff, however within the 1979-2019 interval their wage progress was one-third as quick. The distinction is much more excessive for the bottom wage staff: near zero progress over the forty-year interval versus almost 3% annualized progress over the previous 4 years. Apart from the Ninetieth percentile, all wage teams skilled wage progress not less than as quick in the latest interval as between 1979 and 2019, and far sooner amongst roughly the underside half of the wage distribution.

The very prime continues to amass bigger shares of the general pie

Adjustments on the very prime of the wage distribution can’t be measured utilizing the CPS, however Social Safety Administration (SSA) information reveal what’s taking place inside the prime 10%, 5%, 1%, and even 0.1% of the annual earnings distribution. Between 1979 and 2019, the underside 90% grew 0.6% on an annualized foundation, whereas the highest 5% grew 2.0% and the highest 0.1% grew 3.8% (Gould and Kandra 2023). There are huge variations not solely between the highest and the overwhelming majority, but additionally inside the prime of the earnings distribution.

The newest SSA information solely extends to 2022. The 2019–2022 interval is characterised by comparatively even progress. Primarily inventory market declines in 2022 drove losses among the many highest earners. After dropping considerably in 2022, the inventory market rebounded drastically in 2023 (Trackinsight 2024). Due to this fact, very prime earnings are more likely to present a stable rebound in 2023, persevering with the focus of wages on the excessive finish.

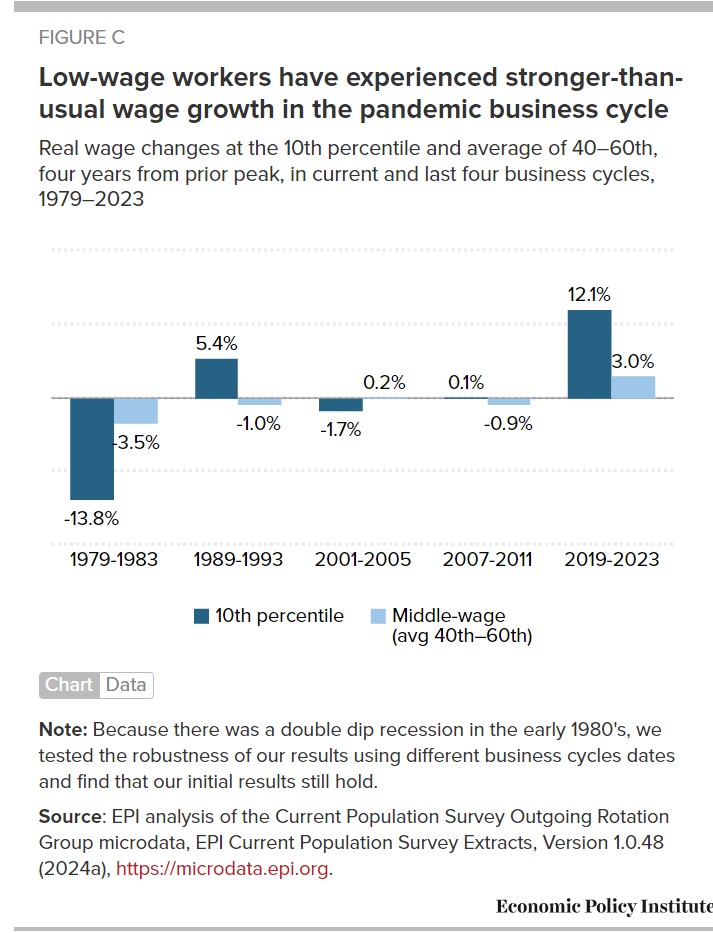

Determine C reveals how distinctive this restoration has been in reaching robust wage progress for low-wage staff. The determine presents the true modifications within the Tenth-percentile wage and the center wage 4 years from the prior peak in every enterprise cycle since 1979. Wage progress on the Tenth percentile within the present enterprise cycle is greater than twice as quick as the following closest interval during the last 40 years.

Center-wage staff, staff between the fortieth and sixtieth percentiles of the wage distribution, skilled slower good points within the current enterprise cycle in comparison with low-wage staff. Nevertheless, the slower middle-wage progress during the last 4 years was considerably sooner than discovered within the 4 prior enterprise cycles.

Sooner progress for low-wage staff was pushed by coverage choices and a decent labor market

The quick progress during the last 4 years (notably for low-wage staff) didn’t occur by luck. It was largely the results of intentional coverage choices addressing the pandemic and subsequent recession on the scale of the issue. Policymakers discovered from the aftermath of the Nice Recession (2008). Wherein, the pursuit of austerity led to a gradual and extended financial restoration.

A number of massive spending payments have been handed within the first 12 months of the pandemic. It supplied enhanced and expanded unemployment insurance coverage, financial impression funds, assist to states and localities, little one tax credit, and momentary safety from eviction, amongst different measures (Gould and Shierholz 2022). These actions supplied aid to staff and their households to assist them climate the recession. These measures additionally fed the surge in employment, which gave low-wage staff higher job alternatives and leverage to see robust wage progress.

Unemployment fell to three.6% in 2022 and held regular in 2023 as each the labor drive and employment grew. The share of the inhabitants ages 25-54 with a job (the prime-working-age employment to inhabitants ratio (EPOP)) rose to 80.7% in 2023. It surpassed even the pre-pandemic excessive of 80.0% in 2019. In actual fact, we’ve got to return to 2000 to discover a prime-working-age EPOP exceeding the extent reached in 2023.

This tightening labor market additional bolstered staff’ leverage. Low unemployment means staff are comparatively scarce. The consequence requires employers to work tougher to draw and retain staff and lessens their discretion to discriminate with out dealing with a profitability penalty. In low-unemployment labor markets, lower-wage and traditionally marginalized staff expertise higher labor market outcomes and sooner wage progress (Bivens and Zipperer 2018; Wilson and Darity 2022).

Moreover, the sudden lack of thousands and thousands of low-wage jobs at first of the pandemic, adopted by the terribly quick employment restoration, meant the frictions tying staff to specific jobs or the obstacles usually holding staff from looking for higher employment alternatives weren’t constraining staff on the lookout for work on this interval. This “severed monopsony” in a time of livid re-hiring lowered the traditional drag on wage progress imposed by these frictions (Bivens 2023). Excessive numbers of low-wage staff stop and located higher jobs, rising churn within the low-wage labor market. This phenomenon elevated low-wage staff’ leverage, which additional contributed to sooner wage progress. Employers merely needed to work tougher to draw and retain the employees they needed.

I’m going to cease right here as the remainder of this report goes past what was achieved in the course of the Pandemic. Not that what’s being mentioned is unhealthy. It’s the subsequent degree of wage enhancements (comparable to improved minimal wage legal guidelines, and so on,). My focus was on the pandemic.

~~~~~~~~

1. In 2020, the underside dropped out of the labor market as low-wage and low-hours staff misplaced their jobs in disproportionate numbers (Gould and Kandra 2021; Gould and Kassa 2021). Because the restoration took maintain in 2021, swings within the composition of the workforce by gender, race/ethnicity, training, work hours, business, and occupation made it essential to account for these variations in measuring wage modifications within the pandemic labor market (Gould and Kandra 2022). By 2022, the dramatic compositional shifts within the pandemic labor market had principally resolved (Gould and DeCourcy 2023). Within the newest 12 months of information, most measurable spikes within the workforce by demographic and job traits normalized within the final 12 months. As a p.c of the workforce, white staff, staff with decrease levers of instructional attainment, and leisure and hospitality staff are discovered at barely decrease charges in 2023 than in 2019.

2. Appendix Determine A supplies a take a look at cumulative actual wage modifications over your complete interval, 1979 to 2023, to get a way of general wage tendencies. Though the latest interval exhibited wage compression, it’s clear that the for much longer forty-year interval of unequal progress stays essentially the most hanging discovering from the general interval.

As talked about within the Atlantic by Rogé Karma, in assist of his article “The U.S. Economy Reaches Superstar Status.”