– by New Deal democrat

The FHFA and Case Shiller repeat gross sales indexes are the final residence gross sales and value knowledge for the month.

Two months in the past I wrote that “for the next seven months the comparisons will be against an average 0.7% increase per month in 2023. Because house price indexes have shown a demonstrated lead over shelter costs as measured in the CPI, if present trends continue, as these YoY comparisons drop out, the YoY deceleration in OER in the CPI index should continue towards its more typical rate of between 2.5% to 4% YoY in the ten years before the pandemic.” Final month I reiterated that “I continue to believe that CPI for shelter will continue to decelerate on a YoY basis, but more slowly than before.”

Each of these tendencies had been burne out with this month’s launch for repeat gross sales by means of March. The FHFA buy solely value index, after a pointy 1.2% enhance in February, solely elevated 0.1% in March. In the meantime the Case Shiller Nationwide index rose 0.3%, down from its 0.5% enhance in February. Conserving in thoughts that mortgage charges lead gross sales, which in flip lead costs, right here’s what the month-to-month numbers seem like for the previous 5 years, in contrast with mortgage charges (purple, proper scale) averaged month-to-month:

The comparatively large lower in mortgage charges between final November and this January led to a giant enhance in gross sales with a rise in costs as nicely. As mortgage charges have climbed previously few months since then, gross sales have declined considerably, and costs have began to observe go well with.

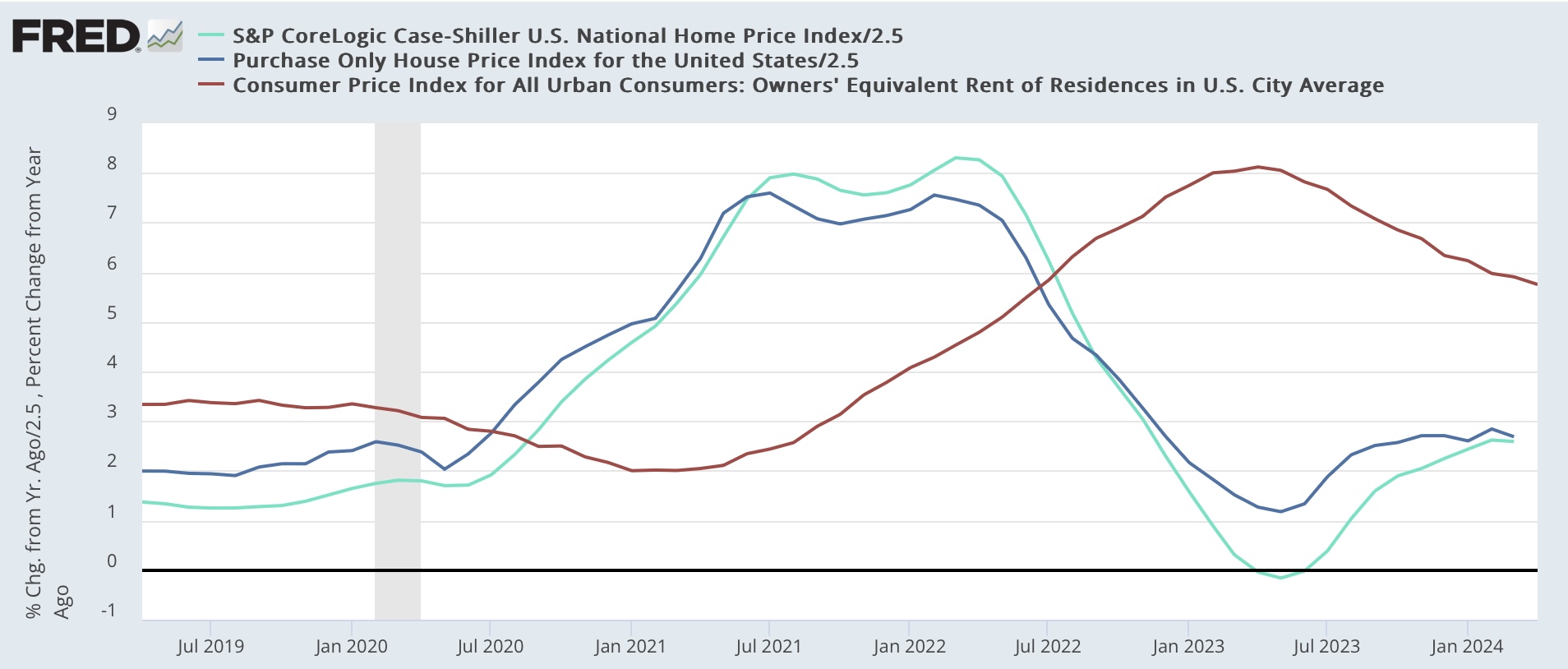

Subsequent, right here is the long run YoY graph of each of them under, in contrast with the CPI for house owners’ equal rend (purple, *2.5 for scale) which continues to point out that the YoY good points are literally not out of line in contrast with good points throughout nearly all of the previous 25 years outdoors of recessions:

Right here’s the close-up view of the final 5 years, higher to point out the present pattern in each costs and shelter inflation for house owners:

On a YoY foundation, the FHFA index decelerated from a 7.0% enhance to six.7%. The Case Shiller Index declined by lower than -0.1% so rounded to an unchanged 6.5% YoY enhance. For the reason that FHFA has had a historic tendency to guide the Case Shiller knowledge by one month, I usually pt just a little extra weight on that index.

The underside line stays that there was no important YoY acceleration within the FHFA repeat gross sales index for the previous six months, and appreciation within the Case Shiller Index has possible halted, with a lag, as nicely. As a result of, as I wrote on the outset, the subsequent 5 months knowledge will likely be in contrast with 0.7% common month-to-month good points final 12 months (as you possibly can see from the primary graph above), I count on the YoY comparisons to point out renewed deceleration, which is able to in the end – with a determined lag – present up within the shelter element of CPI as nicely.

Lastly, do not forget that these are all current residence gross sales, which have been severely constrained by owners being locked into the golden handcuffs of three% mortgages. With restricted stock available on the market, there may be extra competitors amongst potential patrons transferring up from leases, and thus there may be extra value appreciation than would usually be the case.

Repeat residence gross sales value declined barely in January; count on deceleration within the CPI measures of shelter to proceed, Indignant Bear by New Deal democrat