Jeanna Smialak Writes

“The Federal Reserve cut interest rates on Wednesday by half a percentage point, an unusually large move and a clear signal that central bankers think they are winning their war against inflation and are turning their attention to protecting the job market.”

I (and Brad DeLong) marvel why the Fed forecasts extra charge cuts to come back as an alternative of implementing them now? I’m wondering why is an 0.5% reduce thought of massive? The reply to my fake naivety is that it was not clear till yesterday if the speed could be reduce by 0.25% or 0.5%. The truth that it was not reduce by greater than 5% was not information and never reported.

The not naive query of why forecast cuts relatively than implementing them now and probably reversing them is more durable to anser if one doesn’t settle for “that’s the way it has always been” as an reply. Brad has famous that a facet of optimum management is that future shifts are usually not predictable (this can be a characteristic of optimum management beneath a broad set of straightforward assumptions and never a consequence primarily based on a selected mannequin). The solutions have been one thing about credibility and the expections channel (in different phrases ‘I don’t know both professor’).

I’ve two guesses. First it is vital that everybody be taught of the FED’s transfer on the similar time to keep away from insider buying and selling. It’s more durable to handle this (there’s a suspicion that it was not managed final week reported within the free a part of Brad’s substack publish) “That afternoon, however, Wall Street Journal reporter Nick Timiraos released an article . . . Financial Times reporter Colby Smith followed up . . . and markets perceived that as confirmation that the Fed had engaged in covert communications during the blackout.” Avoiding unlawful communication turns into harder the extra billions early discover is value. Avoiding the insinuation that this has occurred made by burned bond merchants turns into not possible. One other rationalization is that the FED simply doesn’t need too many billions of positive aspects and losses to comply with an announcement.

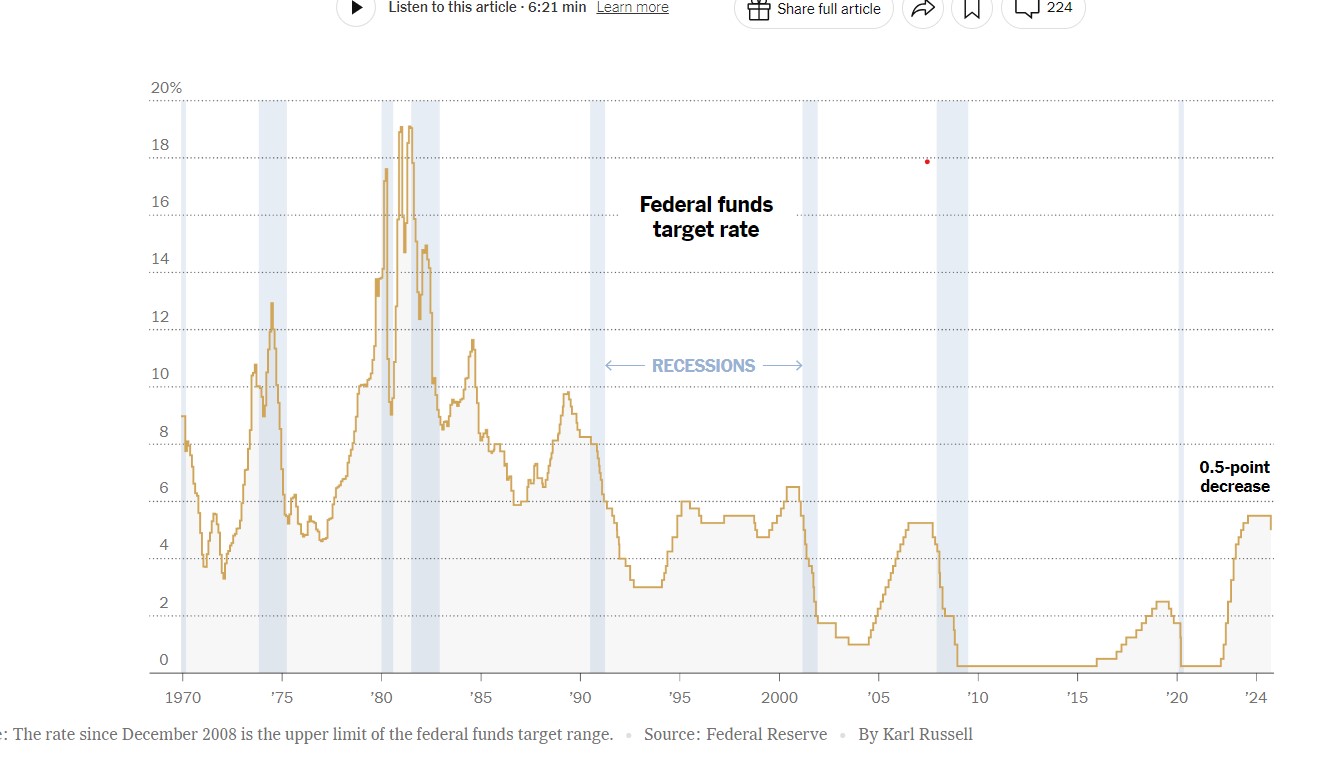

Right here is the Federal Funds charge. Be aware the upward and downward traits, particularly the upward traits throughout 94-5, 99-200, 94-97, 17-19 in response to low unemployment and the worry of future inflations with many very predictable small steps.

I assert that neither concern is expounded to the twin mandate to hunt worth stability and full employment. I do know there are counterarguments associated to credibility and the expectations channel (which I name BS). I believe the FED worries about bond merchants nearly as a lot because the bond merchants fear in regards to the FED. It’s actually clever for bond merchants to fret in regards to the FED. I believe the eye going the opposite means is improper.

Now rates of interest and future anticipated rates of interest do matter loads. Nonetheless their impact is nearly exlusively via the mortgage rate of interest, demand for homes, relative worth of homes, residential funding channel. It’s a incontrovertible fact that the partial correlation of rates of interest and nonresidential funding is statistically insignificant and invisible even to the attentive sample looking for eye. This element has been banished from (nearly all) of the educational macroeconomics literature which has superior by suppressing the excellence between various kinds of funding.

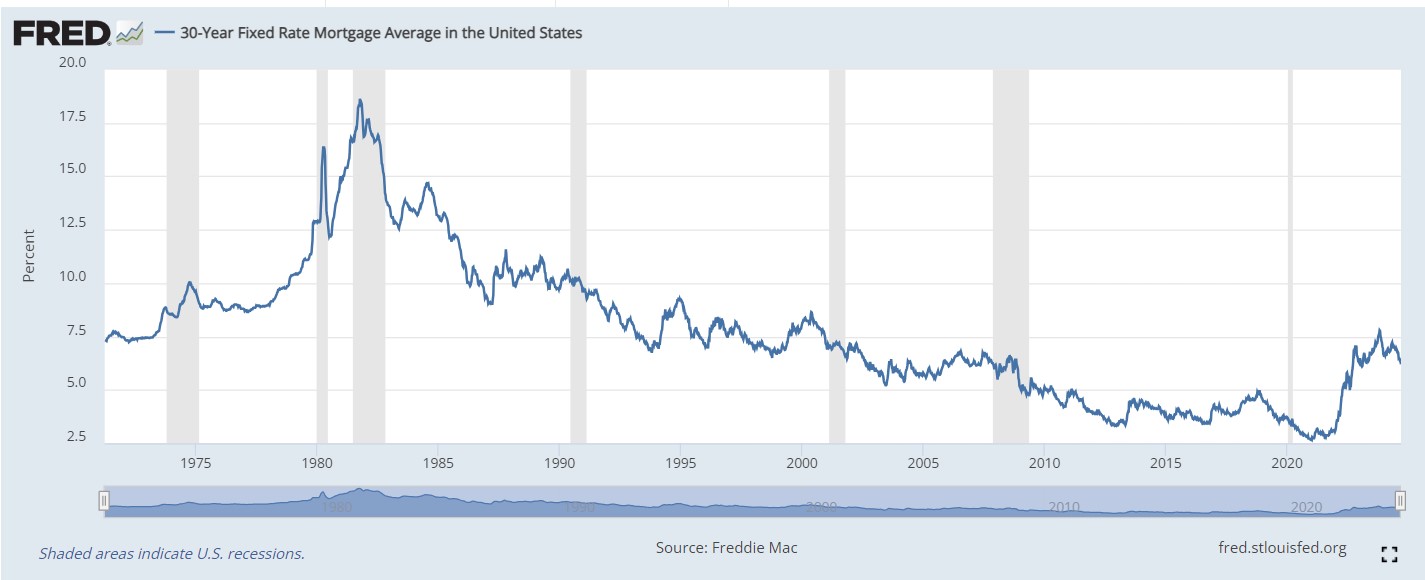

Right here is the 30 12 months mounted mortgage charge sequence.

It’s by no means so extemely predictable within the quick run. It has a transparent damaged long run development up after which down down down then what occurred in 2022? It responds to the Federal funds charge to an extent which is tough to see but in addition bizarrely massive given the distinction in durations and threat premia and all the pieces. I possibly ought to present treasury invoice fixed maturity charge sequence with intermediate durations and tiny threat premia, however I received’t fearing that I would bore you (and being supremely lazy). The sequence clearly displays anticipated future quick time period charges which replicate future anticipated inflation each via the automated demand for bonds fischer impact and the anticipated future FED anti inflation coverage impact.. I’m not satisfied that such expectations may be managed by the FED. I see no trace of a bonus of many small shifts within the Federal Funds charge versus a couple of massive shifts.

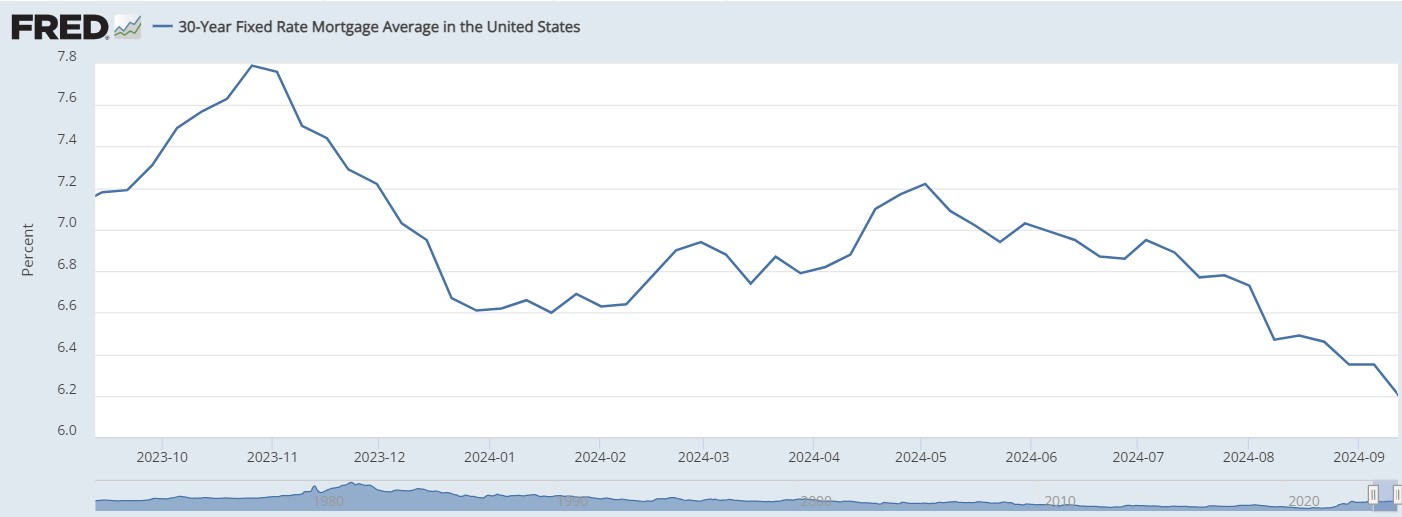

Now take a look at the previous 12 months. I don’t see something reflecting the various latest shifts in expectations of subsequent months Fed Open Market Committee (FOMC) decisions.

I see a downward linear development beginning in Could. I believe that is the rate of interest which impacts combination demand. I don’t suppose Powell’s speaches or monthy FOMC choices have an effect on it a lot.

Appendix: extra traditional Robert boring rants

They are saying “expectations” I ask whose expectations? Once more, one other advance of recent macro is the selection to mannequin aggregates as decisions of a consultant agent (trendy that means since about 1980 after 7 years of precise debate). This suggests that there’s one worth of subjective expectations which is similar for all brokers. It is a theoretically sound assumption if one makes one in all a only a few extraordinarily robust assumptions about utility capabilities or the distribution of earnings and wealth. One doable assumption is that everybody has similar preferences, earnings, and wealth. I believe one attraction of the consultant agent to a few of its outstanding advocates is that every one dialogue of earnings distribution is assumed away. The robust assumptions are simply examined and overwhelmingly rejected by the info. The purpose (if any) right here is that, if one doesn’t assume that everybody is similar, one shouldn’t speak about anticipated rates of interest or inflation or GDP with out specifying whose expectations. For the mortgage charges they’re the expectations of bankers proposing mortgage charges and potential home consumers deciding whether or not to purchase now or wait. I believe because of this these expectations matter for combination demand. Neither, not even retail bankers, are like bond merchants. The expectations which obsess financial coverage makers and which may be learn off from asset costs are fairly completely different from the expectations which have an effect on combination demand.

The inflation expectation which impacts demand for homes is the anticipated inrease within the worth of homes. That is measured barely in any respect (so far as I do know only a bit for a couple of cities by Robert Shiller et al). This can be very necessary. The few observations present big shifts, for instance from 2005 to 2008. Correlation just isn’t causation, however come on, this clearly made an enormous distinction.

Different medium time period inflation expectations have a giant impact on precise inflation. Corporations attempt to not change costs too usually and to not change backwards and forwards. Which means present worth setting choices depend upon anticipated medium future worth modifications by rivals and suppliers. Corporations and staff sometimes set wages for some time (3 years in formal contracts). Future anticipated inflation issues to them.

Each are strongly relatd to inflation and worth stability. Neither clearly associated to employement (I explicitly assert that is true for aggregat common wages and combination employment within the USA).

The expectations of worth setters and wage setters (or wage negotiators and each exist) matter. Are they affected by the FEDs efforts to handle expectations. I (possibly being ignorant) know of no proof about that and I strongly suspect that the reply just isn’t a lot.