Huge Image – Offended Bear")

Scenes from Friday’s jobs report: the (completely contradictory) Huge Image

– by New Deal democrat

There isn’t a necessary financial information at the moment, so let’s take a better have a look at a number of the noteworthy objects from Friday’s jobs report. I’ll begin out with the Institution Survey facet after which flip to the Family Survey facet.

Items producing vs. service offering

Previously, a turndown in items producing job has at all times preceded a recession. Any turndown within the service sector has occurred a lot later. So I’ve been specializing in the previous.

In February, the products producing facet added 34,000 jobs, its greatest exhibiting since June of 2023. On a YoY foundation, items producing jobs are up by 0.4%, whereas service offering jobs are larger by 1.4%. The beneath graph norms every of these ranges to zero:

Huge Image – Offended Bear")

The tempo of decline in every sector is decelerating. Whether or not it has stopped could be very a lot open to query.

The norming of present YoY ranges to zero was for the aim of exhibiting the long run historic comparisons, as beneath, first from 1948 to 1982:

And secondly from 1982 by means of 2019:

The very first thing to note is that the products producing sector has *at all times* turned damaging first, with the only exception of the 1982 Volcker-induced recession, once they each turned down concurrently. Word additionally that there have been 5 events when the products producing sector turned damaging YoY with no recession occurring.

Second, whereas earlier than 1982 the products producing sector won’t flip decrease than its present YoY degree till after a recession had begun, since then items producing jobs have at all times been decrease by about -2% greater than its present degree earlier than the onset of a recession – and typically decrease than its present YoY degree for over a 12 months.

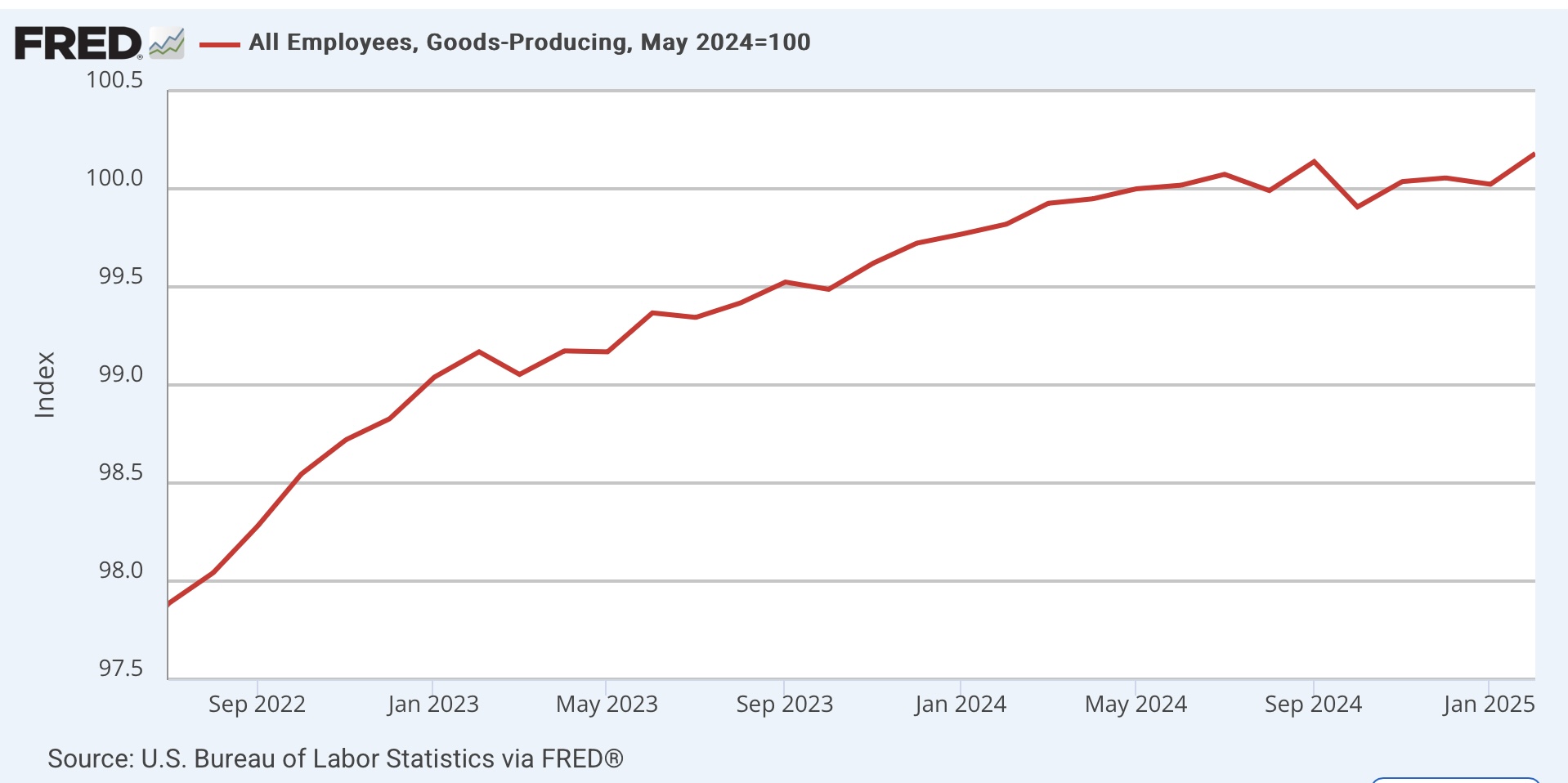

How shut are we to that? Right here is absolutely the degree of products producing jobs, normed to 100 as of final Could:

With the leap in February, this sector is larger by 0.2% than 9 months in the past. Probably the most cheap pessimistic case is that it received’t be decrease YoY till a minimum of Could – and even when it turns down, it could possibly be for much longer than that.

The underside line is that employment within the items producing sector just isn’t forecasting a recession any time quickly.

Housing building

There’s one sub-sector that I’ve been paying explicit consideration to, as a result of though I received’t trouble with the graph, manufacturing jobs have been down since February of 2023. It has been building, and particularly housing building, which has been holding up the products producing sector. And as I’ve not too long ago written, though housing permits, begins, and gross sales turned down way back, housing models below precise building levitated for a lot of months thereafter earlier than lastly turning down final 12 months. I identified that normally jobs in housing building have sometimes levitated for a lot of months after that.

And the levitation of employment in housing building continued in February, nonetheless up by over 2.5% YoY (pink, left scale within the graph beneath) though solely 100 jobs had been added (blue, proper scale):

In different phrases, the upward pattern in housing building doesn’t even present any indicators of slowing down but.

In abstract, that’s why the Institution report on Friday was optimistic. Now let’s flip to the Family survey facet, which was horrible – in different phrases, as soon as once more it was recessionary.

Unemployment and Underemployment

The headline was that the unemployment charge ticked up by 0.1% to 4.1%, and the broader underemployment charge spiked larger by 0.5% to eight.0%, the best degree in over 3 years.

As with the above, I’m going to deal with YoY comparisons. On that foundation, the unemployment charge was larger by 0.2%, and the underemployment charge larger by 0.7%. Once more, for historic functions right here is that graph for the final a number of years, normed to zero as of the most recent readings:

Whereas the U6 underemployment ranges are noisier than the unemployment charge ranges, the YoY will increase in every has decelerated in latest months, which is an efficient signal.

However now let’s have a look at that traditionally. As a result of the U6 information didn’t begin till 1994, right here is the unemployment charge YoY earlier than than:

And now right here is the document for each from 1994 till the pandemic:

With respect to the unemployment charge, whereas far as a rule even a 0.2% improve YoY has meant recession, there have been a lot of false positives, together with within the Fifties, Nineteen Sixties, one month within the Nineteen Eighties, and the close to “double dip” in 2002.

However with respect to the underemployment charge, being larger YoY by the present degree has meant recession in every case apart from the 2002 close to “double dip.”

However since this previous month was a spike, let’s present the above graph once more, this time utilizing the typical of the final 3 months, which is a rise YoY of 0.43%:

We nonetheless get the identical consequence.

In different phrases, the adjustments in each the unemployment and underemployment charges are recessionary. However with the massive caveat that they’ve been so for the previous 12 months or so, and no recession has occurred. In different phrases, it appears like one other false optimistic.

The Employment Inhabitants Ratio

I carried out the identical train with the Labor Drive Participation Price, together with specializing in the prime age 25-54 charge, however to chop to the chase, it was of little worth due to distortions from the entry of girls into the labor pressure within the Nineteen Sixties by means of the Nineties, and likewise as a result of demographics of the Child Growth adopted by the Gen X bust, adopted by the Millennial Growth.

However the employment inhabitants ratio does give significant data, significantly once we have a look at the prime age element. This declined -0.2% in February to 80.5%, which is down -0.4% from its latest peak final summer season.

As soon as once more I appeared YoY, and since this information can also be noisy, I used the typical the final three months, which was -0.033%. The beneath graph exhibits this information month-to-month (blue), and on a quarterly common foundation (pink):

Once more, it’s damaging, however the tempo of decline has stopped in latest months.

Now right here is all the historic look, additionally normed to zero as of the present 3 month common:

Except a number of months within the Fifties, a number of months in 1995 and 1998, and the 4th Quarter of 2013, the present YoY decline within the prime age employment inhabitants ratio has *at all times* beforehand meant recession. However once more, now we have been at this degree for practically a 12 months, and no recession has occurred – a minimum of not but.

I ought to add that I’ve two main issues, one for every survey.

As to the Institution Survey, the QCEW, which is the gold customary, on a preliminary foundation signifies that employment positive factors final 12 months by means of Q3 had been about 500,000 lower than at present proven. So this survey is prone to look weaker when rebenchmarked utilizing that information – except the preliminary QCEW information is itself revised larger.

As to the Family Survey, I stay involved that it nonetheless just isn’t correctly accounting for the large immigration wave of the a number of years instantly following the COVID pandemic. What i actually imply is that the will increase within the unemployment and underemployment charges, in addition to the downturn within the prime age employment inhabitants ratio, may actually be about latest immigrants discovering it more durable to achieve employment than a number of years in the past. Which signifies that the financial system continues to be rising, simply not quick sufficient to digest all the new entrants to the market.