by Steve Roth

Initially Posted at Wealth Economics (June 2023)

Current headline inflation prints are beneath the Fed’s goal, and falling. That information is a strong instrument for controlling expectations, however the Fed’s not utilizing it.

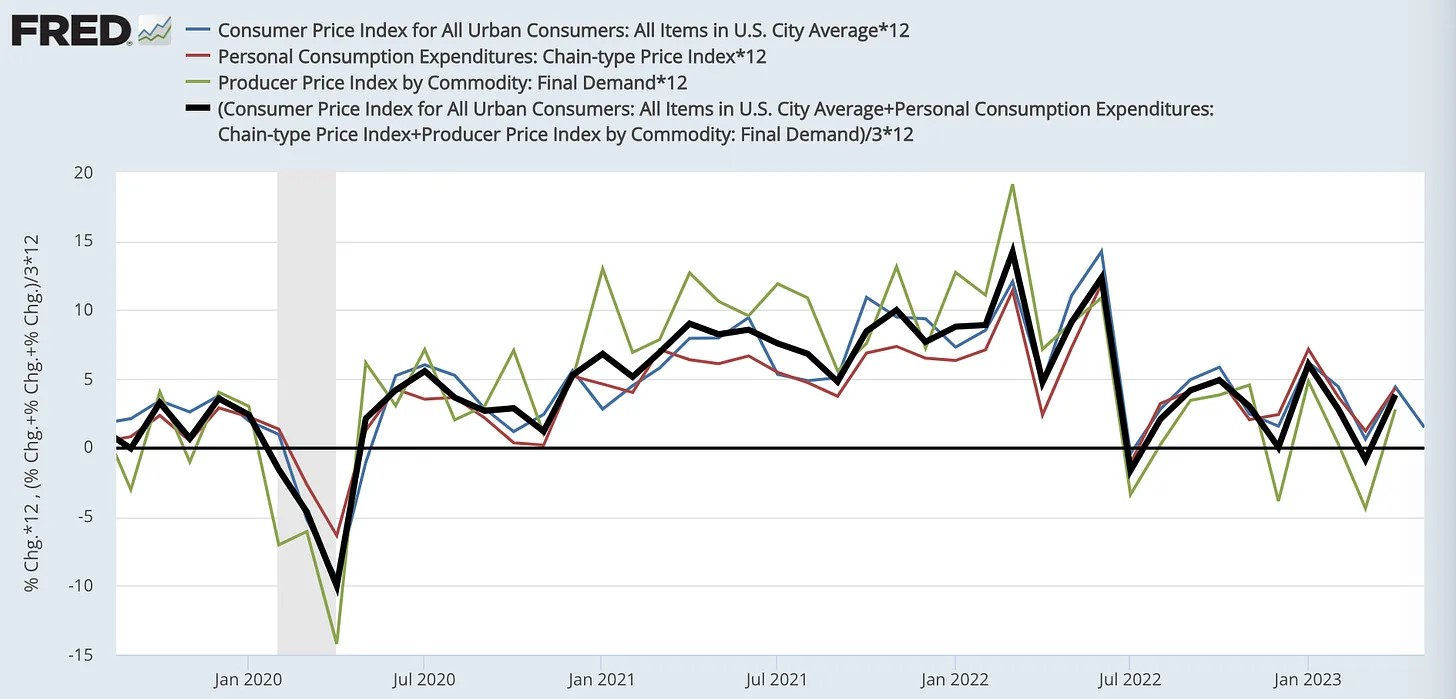

1.5%. That’s the most recent headline inflation price within the U.S. per the Could CPI launch, and likewise in accordance with a three-month common of three completely different inflation indexes that use considerably completely different knowledge, baskets, and weightings.

It looks like this low inflation ought to do a lot to tame folks’s inflation expectations: the Fed’s bugbear. They need to be shouting this from the rooftops, proper?

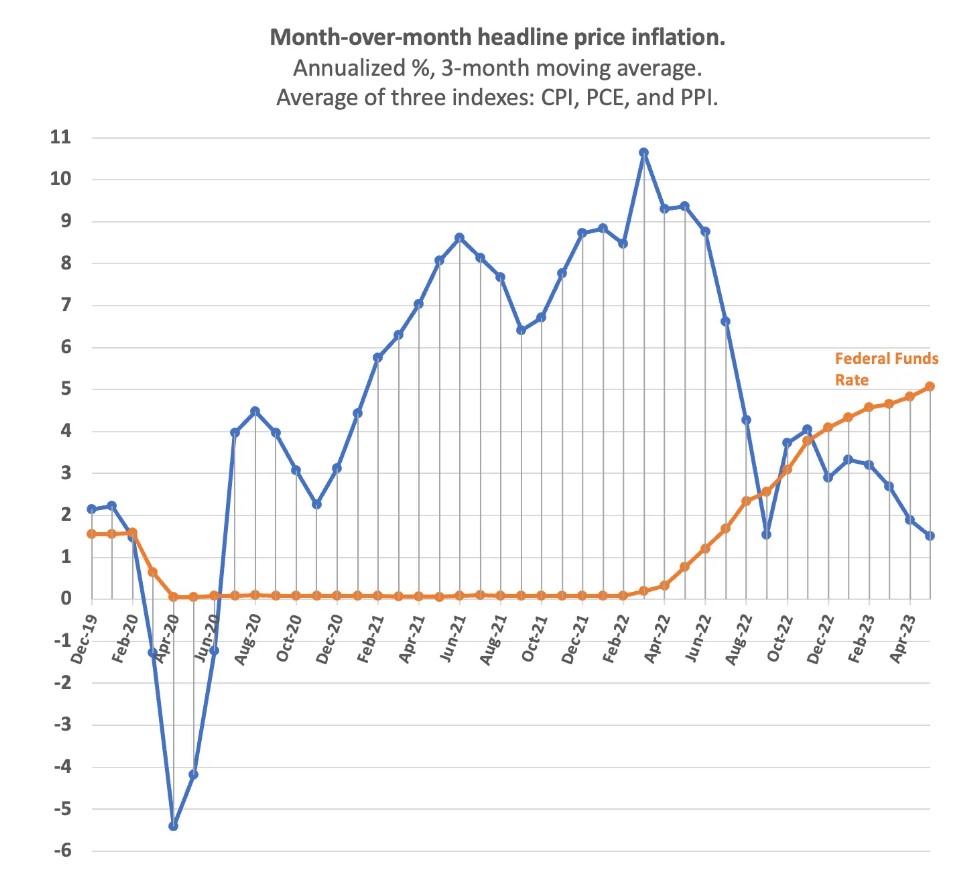

By this multi-index quarterly measure, which smooths out unstable, random, and “head-fake” outcomes with out resorting to the distorting extremes of twelve-month year-over-year averaging or pessimistic slices of the information, the information is superb certainly. The measure’s been declining, with one small uptick, for six months. (Following the energy-price-driven cliff-dive in July.) It’s been at or beneath 4% for 9 months. In one other key benchmark, the fed funds price has been (more and more) above the inflation price for six months.

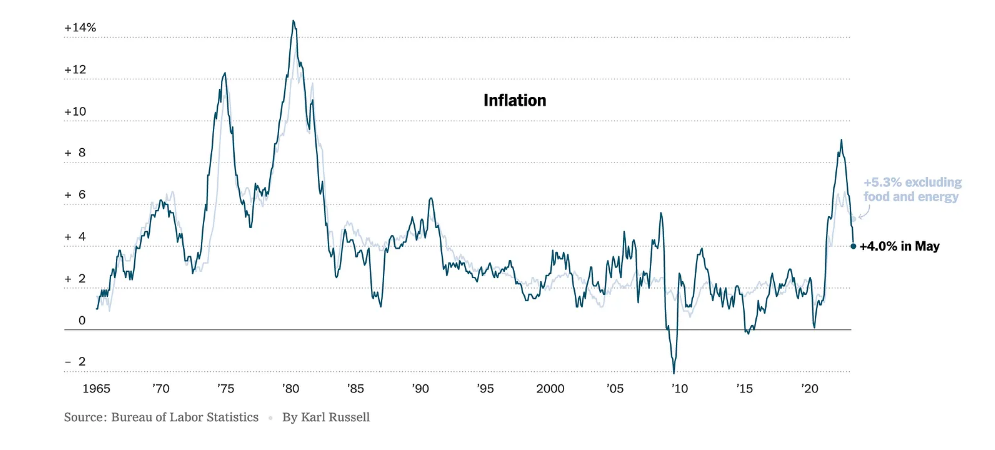

However what does the press report? Right here from the June 13 New York Occasions article, headlined “May Inflation Report.” Washington Put up delivers the very same graph.

This isn’t Could inflation. It’s (silently) reporting year-over-year (common) inflation for the twelve months June ’22 by means of Could ’23.1 The 14.3% June ’22 print, for example skews this “May” inflation price unrealistically upward. The true “headline news” is that month-to-month inflation is printing at pre-pandemic ranges, properly beneath the Fed’s 2% goal.

The Occasions doesn’t simply bury the lede; they don’t even report it within the article. (The Put up does present a chart of month-to-month adjustments, although not annualized and with out dialogue.) They usually’re not alone. Ask Google, for example: “what was the CPI inflation rate for May 2023?”

Whither goes the Fed…

The Fed constantly does likewise. In his statements following FOMC price selections, for example, Chairman Powell by no means mentions current months’ adjustments — solely yr over yr. This week’s June 14 assertion:

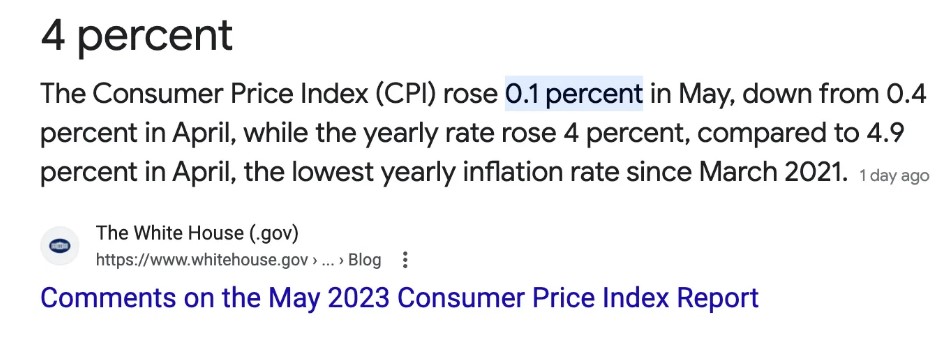

Inflation stays properly above our longer-run 2 % aim. Over the 12 months ending in April, complete PCE costs rose 4.4 %; excluding the unstable meals and power classes, core PCE costs rose 4.7 %. In Could, the 12-month change within the Client Value Index got here in at 4.0 %, and the change within the core CPI was 5.3 %. Inflation has moderated considerably because the center of final yr.

“Somewhat”? Final June, the PCE and CPI month-to-month prints have been at 11.9% and 14.3% respectively. The Fed’s and Fed-watchers’ “preferred” and more-pessimistic “core” inflation, and different more and more slim measures, simply amplifies the tendency embodied in YoY averaging when inflation’s falling. There’s at all times some measure that appears extra worrying, at the same time as the excellent news rolls in.

A cynical view may recommend that the Fed governors are performing out a Seventies/80s childhood trauma, despite the fact that immediately’s situations — together with (un)employment, bond yields/costs, and fairness costs — are vastly completely different. PTSD as financial coverage, with the press blithely following alongside?

To some larger or lesser extent, folks’s inflation expectations are at all times going to be powerfully affected by present (current) inflation charges. If controlling expectations to forestall the dreaded “wage-price-spiral” is a key aim for the Fed, aren’t they leaving a strong coverage instrument mendacity on the bottom, mouldering? It’s a thriller.

As at all times, ideas and options from my light readers are a lot appreciated.

1 Since this display seize, the Occasions has up to date the tremendous print on the backside, including “Year-over-year change in the Consumer Price Index.” WaPo hasn’t.