Labor market stays robust. Even so, the Fed ought to minimize charges in September (EPI)

Two issues are true proper now for the U.S. financial system:

- The labor market is awfully robust when judged by any historic benchmark.

- The Federal Reserve is behind the curve in chopping rates of interest and will begin chopping charges on the Federal Open Market Committee (FOMC) assembly subsequent week. To goal for one thing like a federal funds price that’s no less than two share factors decrease by mid-2025.

These may strike some as being in rigidity, usually we wish the Fed to chop rates of interest to stimulate a weak financial system. Why then, if the labor market is sort of robust, do we’d like them to chop?

Merely put, the rates of interest the Fed controls at the moment are at ranges which can be extremely contractionary. They’re charges you’d need in case your purpose was to considerably gradual the tempo of combination demand development (say since you had been attempting to rapidly scale back inflation). There’s a entire debate available about whether or not or not the Fed ought to have raised charges this excessive and this quick in an effort to fight the post-pandemic inflation. No matter the place you landed in that debate, it appears far clearer, right this moment’s financial system doesn’t want a fast discount in combination demand.

The labor market is powerful, however it isn’t inflationary. To summarize its power, we might observe that the prime-age employment-to-population ratio (the share of adults ages 25–54 who’re employed) remained in August at its highest degree since 2001. However this power comes whilst inflation has been quickly decelerating since mid-2022. The value index for private consumption expenditures excluding meals and vitality costs (the measure of “core” costs that ought to be the Fed’s goal) noticed its development price fall by greater than 1.5 share factors simply prior to now yr. It’s now nearly a half-point above the Fed’s long-run goal, and it’s falling quick.

Crucially, this fast disinflation has occurred even because the labor market stays robust. Therefore, there isn’t any purpose why the Fed ought to be trying to generate a weaker labor market, however latest months have seen indicators of a slight softening on the labor markets on the margin. Continued contractionary financial coverage will exacerbate this labor market weakening. This occurring even because the final two years present such weakening is clearly not wanted to get the final little bit of extra inflation wrung out of the system.

Nominal wage development is beneath 4%—a tempo totally in step with the Fed’s long-run 2% inflation goal.

Additional, many labor market indicators look about the identical as they did pre-pandemic, and rates of interest on this interval had been considerably decrease than right this moment, and the Fed even minimize charges in 2019.

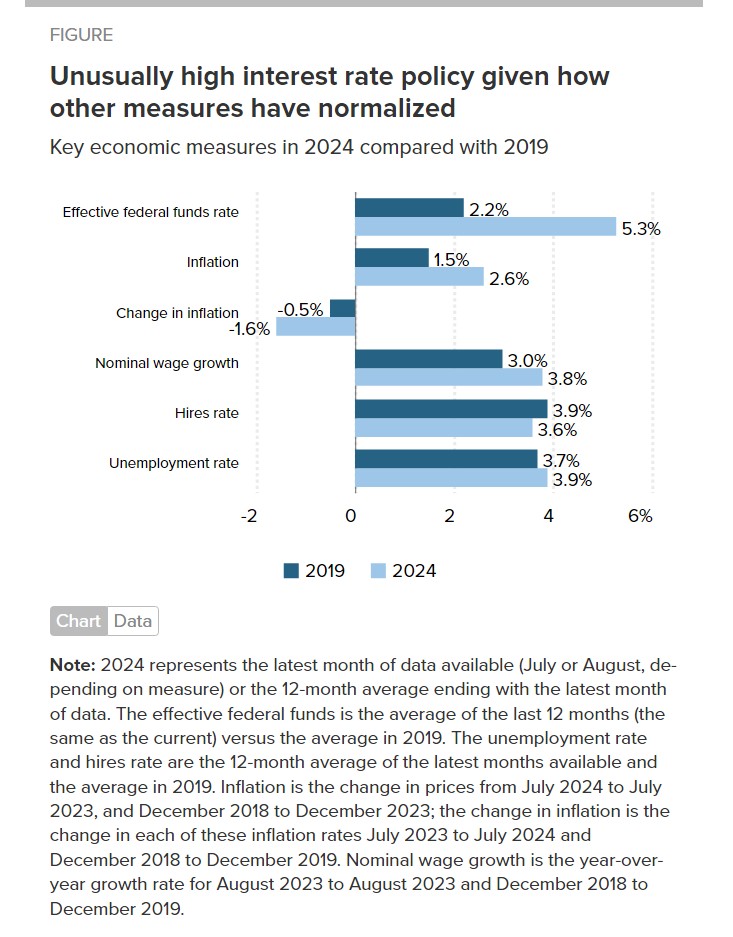

The determine shows a collection of financial indicators—together with the federal funds price—in the newest interval in contrast with 2019. Most metrics we’re experiencing right this moment are consistent with the robust 2019 labor market. Over the yr, the unemployment price has averaged just under 4%, whereas the hires price has come down significantly and is just under 2019 ranges. Nominal wage development hasn’t fallen to pre-pandemic development charges, however that’s an affirmatively good factor—it means staff are receiving actual (inflation-adjusted) wage good points whereas nonetheless having nominal wage development that may enable a full normalization to pre-pandemic inflation charges. Additional, whereas inflation was greater prior to now yr than it was in 2019, it has decelerated far sooner than in 2019, when this inflation deceleration contributed to a Fed determination to chop rates of interest.

In brief, now we have a powerful labor market that can be not inflationary. That means, we don’t want expansionary or contractionary coverage. This implies rates of interest ought to be a lot nearer to impartial ranges than they’re right this moment.

The place precisely is the “neutral” price for the Fed (within the jargon individuals name this R*, or R-star)? No one actually is aware of. However everyone is aware of it’s nowhere close to the 5.3% efficient federal funds price the Fed is sustaining right this moment. 3-3.5% can be rather a lot nearer to impartial, so getting nearer to this vary—and fairly quickly—ought to be the Fed’s purpose till one thing vital modifications within the financial system.

Decrease charges won’t simply preserve right this moment’s wonderful labor market from undesirably softening. It would additionally assist long-run investments in housing and clear vitality change into extra viable and carry off sooner in coming years, that are each massively vital objectives.