– By Jasmine Cui and Matthew Danbury

Throughout the nation, the prospect of residence possession is slipping out of attain for the strange purchaser.

The affordability hole — an estimate of the distinction between an space’s median family revenue and the way a lot revenue is important to afford funds on a median-priced residence in that space — is close to a 10-year excessive within the U.S., in response to an NBC Information evaluation of housing knowledge. The evaluation and the most recent numbers from the NBC Information Residence Purchaser Index present what consultants say is a housing market inaccessible to a rising variety of individuals.

NBC Information’ evaluation reveals:A family incomes the native median revenue would be capable of afford a house in additional than 60% of counties nationwide. 5 years in the past, it might have been capable of afford a house in simply over 90%.

Affordability is dropping even in counties with lower-priced houses.

NBC Information’ Residence Purchaser Price Index — which measures how costs, mortgage charges and incomes have an effect on residence searches — is approaching highs final seen throughout a traditionally frenzied 2022 market.

The Price Index has elevated in 89% of U.S. counties over the previous 5 years as excessive rates of interest and low development have pushed up costs.

The median residence sells for practically $70,000 greater than the typical family can afford, pinching some consumers’ family budgets.

It’s the third-worst the affordability hole has been within the 10-plus years of information.

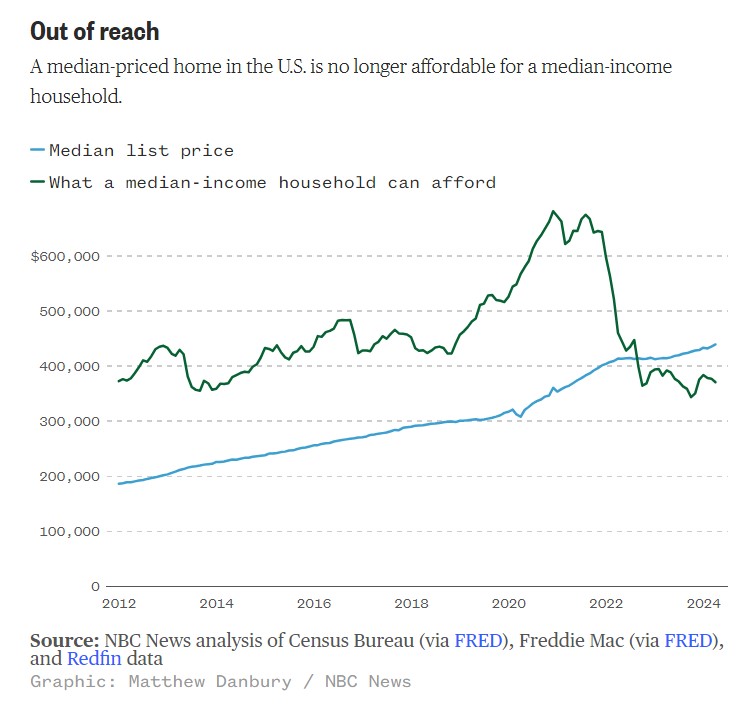

Out of attain

A median-priced residence within the U.S. is now not inexpensive for a median-income family.

“It’s pretty much an impossible market, even for middle-income households,” mentioned Alexander Hermann, a senior analysis affiliate at Harvard’s Joint Middle for Housing Research. From April 2019 to April 2024 in counties the place knowledge is obtainable, the median listing value rose 55% to $102,850, in response to an NBC Information evaluation of Redfin knowledge.

Hermann attributes the persistent value stress to provide shortages. Nationwide, in response to Redfin knowledge, stock has decreased greater than 30% since 2019, and has declined in 7 out of each 10 of the counties measured.

Many monetary advisers think about a house inexpensive if mortgage funds, taxes and insurance coverage prices don’t exceed 30% of a family’s month-to-month price range. In 2019, a family incomes the native median revenue may afford to purchase the median-priced residence in 94% of U.S. counties. As we speak, that may be mentioned of solely 63% of counties.

The conservative estimate assumes a 20% down fee on a 30-year mortgage wherein every month-to-month fee is not more than 30% of the family’s month-to-month pretax revenue.

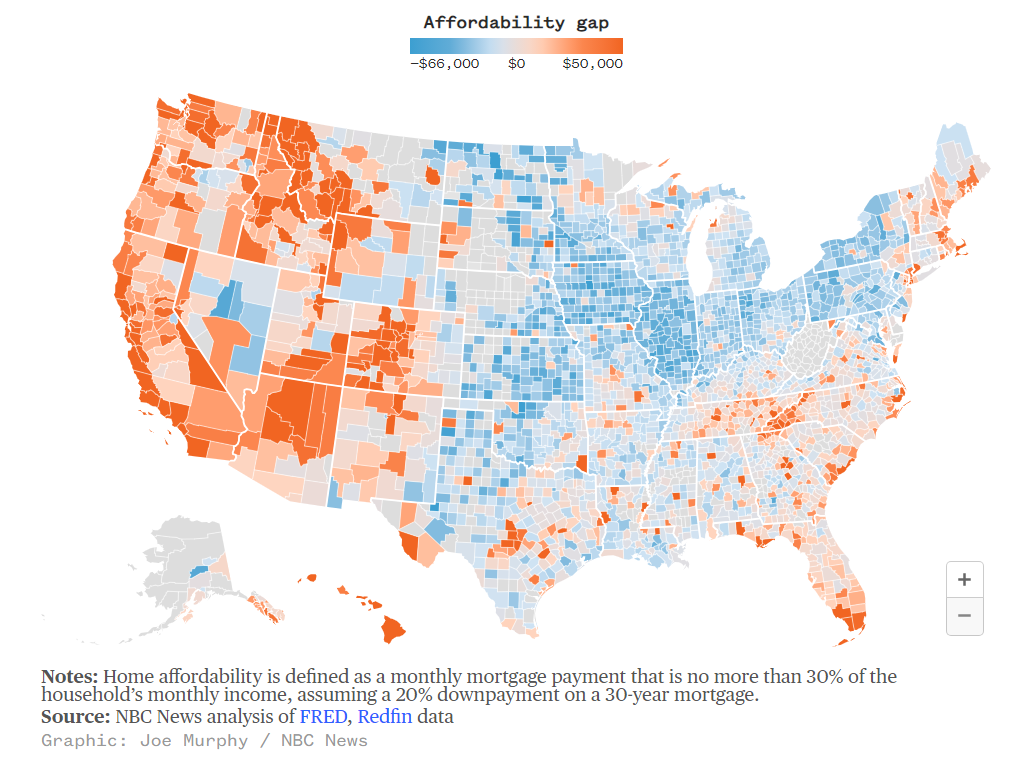

The hole between revenue and residential value is especially pronounced within the West.

It’s worse out West

The hole between a county’s median revenue and the revenue wanted to afford the median residence value there may be largest within the West, the place the median revenue is usually lower than the revenue wanted.

Within the San Francisco Bay Space county of Alameda, which incorporates the cities of Oakland and Alameda, the hole between what consumers can afford and what houses promote for is sort of $73,000. Alan Teague, who lived within the Bay Space for practically 40 years and was on town of Alameda’s planning board, mentioned a number of the area’s affordability hole will be blamed on a scarcity of obtainable houses, because the tempo of constructing is much under demand.

“The sheer cost of houses has gone up, you know, an order of magnitude in the time that I’ve been here,” Teague mentioned. “The supply has not kept up.”

New development would assist ease the hole, Teague mentioned, however he added that the worth of constructing within the area stays excessive. “We were being told that an affordable unit costs a million dollars per unit or more,” Teague mentioned. “That’s mind-boggling.”

Even in counties that, by the numbers, look inexpensive, issues are shifting

The place adjustments in possession prices are affecting homebuying issue

The Residence Purchaser Price Index measures shopping for issue attributable to mortgage charges, insurance coverage prices, and listing costs which might be excessive relative to native median incomes. Larger values point out larger issue.

Extra pages to the above will be discovered at this hyperlink: NBC Information Residence Purchaser Index

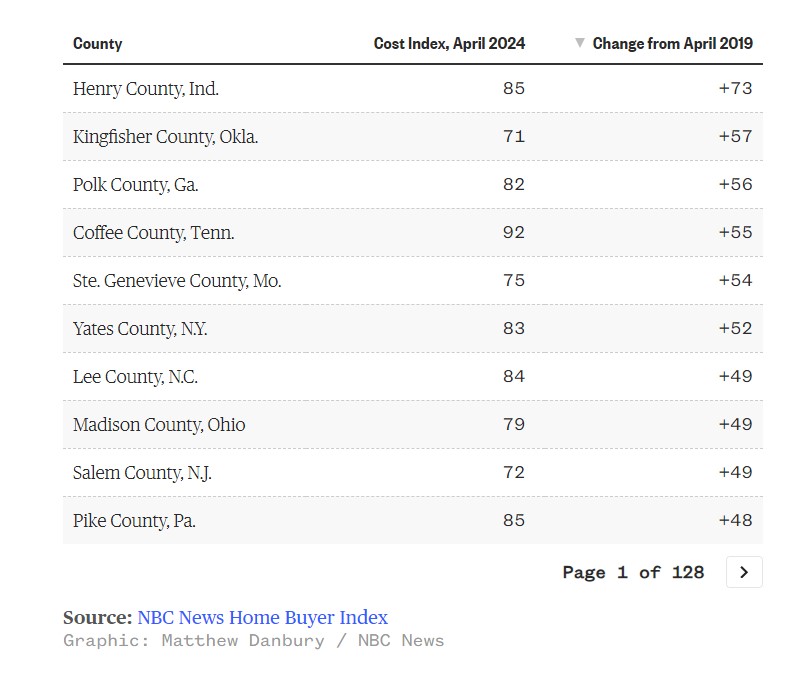

In Henry County, Indiana, east of Indianapolis, the median listing value is $190,000, lower than half the nationwide median. However costs in Henry have greater than doubled since 2019 — taking the county from being one of the vital inexpensive locations to purchase to at least one the place houses are edging out of attain for locals. Reflecting that, the county’s Residence Purchaser Price Index elevated extra from 2019 to 2024 than that of some other county NBC Information measured.Hart Summeier, proprietor of Stage Up Actual Property Group, mentioned the consumers in Henry County who’re feeling squeezed essentially the most are first-time consumers and people on mounted incomes, just like the aged. In response, Summeier mentioned, consumers have began “biting the bullet” and accepting houses with trade-offs they wouldn’t have accepted in earlier years.

“OK, I will drive 40 minutes to work each day each way to not have to pay another $1,000 more monthly to be close to my job,” he mentioned.

Sydney Personett skilled that squeeze firsthand attempting to purchase a house in 2024. On the time, Personett, 24, and her husband, Tucker, had been attempting to purchase a house someplace east or northeast of Indianapolis. Hamilton County was “extremely expensive,” she mentioned, which left Henry County and Hancock County.

The couple discovered themselves thwarted in Henry by a scarcity of provide, they usually finally stomached greater residence funds and acquired in Hancock.

“We both made a lot of sacrifices in college, kind of preparing ourselves, you know, doordashing on the side just to get in some extra cash,” Personett mentioned. “We both knew that our end goal was to buy a home together and kind of build this life for each other.”