By Daniel Bergstresser

Second of two commentaries on Authorities Debt. This commentary does point out tax insurance policies since 2000 which lowered income. The newest handed in 2017 as advocated by trump and supported by Congress. It handed underneath Reconciliation. The failure to stability out the debt created by the tax discount with income achieved by financial development will drive a repeal of it.

Right here, the writer discusses the dreag on the financial system and residents because of growing debt not coated by income.

The Concern:

Curiosity funds on federal authorities debt are projected to succeed in $892 billion in 2024.

That is greater than the federal government is projected to spend on protection. It’s nearly a 3rd greater than what america spent on debt curiosity funds in 2023.

The rise displays the mix of the rise in US authorities debt and better rates of interest. Rates of interest are anticipated to inch decrease within the coming years as inflation subsides. Nonetheless the counter to this because the Congressional Funds Workplace (CBO) forecasts, curiosity funds as a % of GDP will proceed to rise. The extent of this enhance was not foreseen even within the current previous years. The CBO’s projections of the curiosity burden of the debt have been steadily growing.

Briefly, The Info:

The present excessive value of servicing the nationwide debt is partly a mirrored image of the traditionally giant dimension of the federal authorities debt.

Authorities debt is the sum of present and collected previous price range deficits in addition to the cumulative value of financing these deficits. There was a notable enhance in US authorities debt for the reason that financial downturn of the Nice Recession. Authorities debt required elevated federal spending which lowered tax revenues. It was adopted by the pandemic shock. As well as, there was a long-lasting downshift in authorities revenues because of adjustments in tax coverage since 2000, which has additionally considerably contributed to the mismatch between authorities revenues and authorities spending. Debt-to-GDP ranges have been greater than at any time for the reason that late Nineteen Forties. At $28.2 trillion, the entire federal debt held by the general public is projected to be 99% of GDP by the top of 2024.

The price of servicing the debt has additionally been rising because of growing rates of interest.

Rates of interest have been excessive because the Federal Reserve raised its benchmark Fed funds fee from close to zero in March of 2022 to a spread of 5.25-5.5% in July of 2023. This enhance was to struggle the inflation surge following the pandemic restoration. Consequently, borrowing prices have risen. The yield on the 10-year Treasury invoice was 4.2% in June 2024, as yields have hit the highest ranges in 15 years. Whereas the Federal Reserve is anticipated to start lowering the Fed funds fee because the slowdown in inflation continues, the Congressional Funds Workplace forecasts that the speed on 10-year Treasury notes will decline slowly to 3.6% by the fourth quarter of 2026 after which rise steadily once more, reaching 4.1% by 2034.

The mix of huge debt and excessive rates of interest signifies that the federal authorities’s value of servicing its debt relative to nationwide revenue is reaching all-time highs.

At a projected $892 billion in 2024, curiosity funds on the federal debt symbolize 3.1% of GDP in 2024. Since 1940, internet outlays for curiosity have by no means exceeded 3.2 % of GDP. Within the CBO’s June 18, 2024 outlook, authorities spending on debt service is forecast to exceed that proportion yearly from 2025 to 2034. About two-thirds of the expansion in internet curiosity prices forecast from 2024 to 2034 stems from anticipated will increase within the common rate of interest on federal debt, and the remaining third displays the anticipated enhance within the quantity of debt.

The curiosity burden of the debt partially relies upon upon the maturity construction of the debt.

The US Treasury considers tradeoffs when deciding easy methods to finance the present price range deficit and the rolling over of maturing debt. One choice includes the sample of maturities of excellent debt. The US Treasury points debt with maturities as brief as one month and so long as 30 years. Brief-maturity debt requires frequent rolling-over of the debt which makes the Treasury vulnerable to better volatility in curiosity funds. Longer maturity debt comparable to 30-year Treasury bonds usually pay greater rates of interest than shorter maturity debt comparable to 3-month Treasury payments (though not all the time, and not lately).

A lot of the excellent debt in late 2022 was scheduled to mature inside the subsequent three years. That debt has been refinanced at greater rates of interest, sharply elevating debt service prices. For instance, ~ $7 trillion price of debt held by the general public was refinanced through the 2023 fiscal 12 months (October 2022 by September 2023). Every proportion level enhance in rates of interest on that refinanced debt meant $70 billion per 12 months extra in internet curiosity funds in that first 12 months (for context, that is about 10 % of your entire United States protection price range). The maturity construction of debt stays very brief, with half of excellent debt now maturing by 2026. Latest forecasts of curiosity on the debt mirror the truth that giant quantities of federal debt shall be rolled over at greater charges.

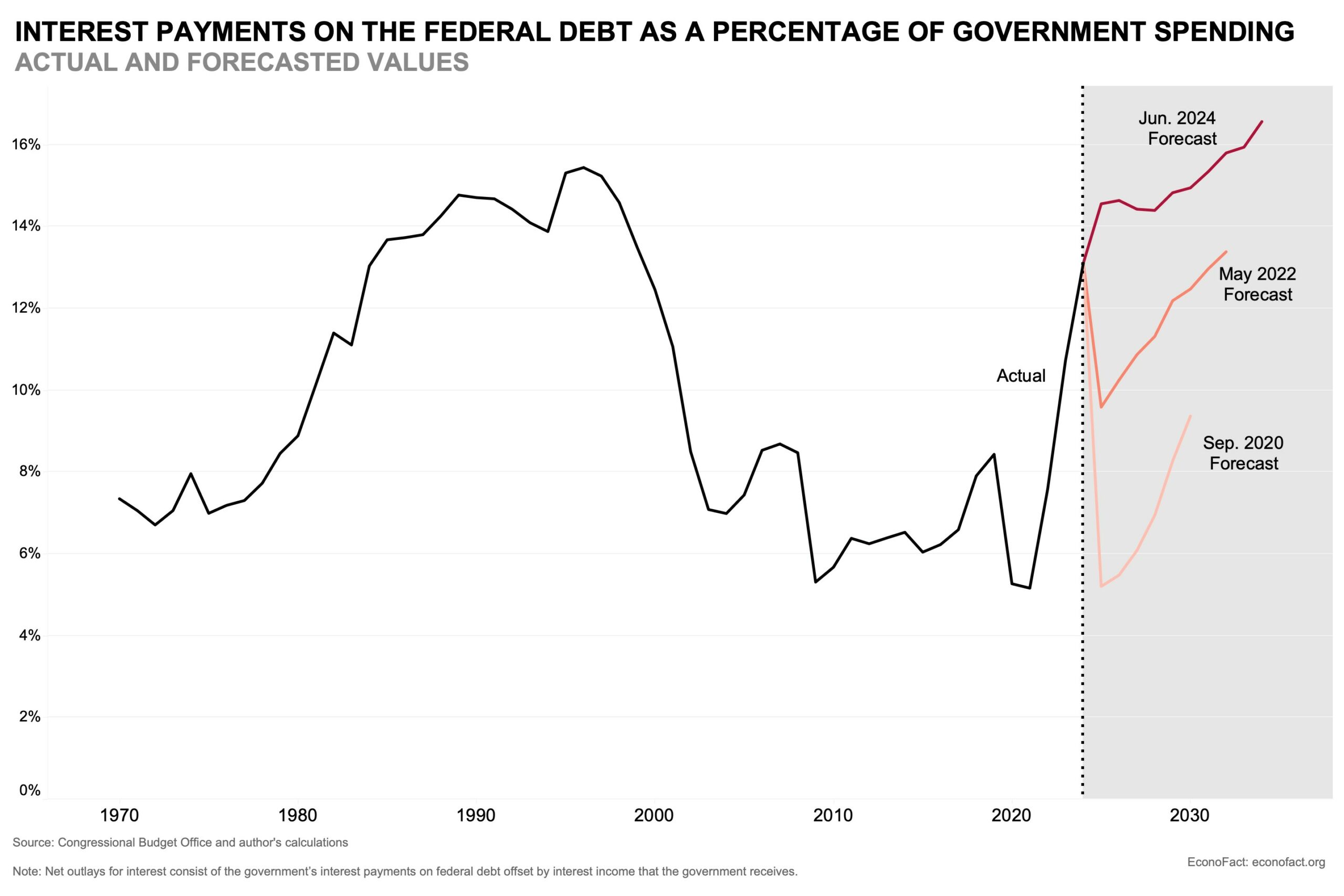

Servicing the federal debt has been taking over an more and more bigger share of presidency spending.

Curiosity funds made up about 13 % of federal spending in 2024. It being the third highest class of spending forward of spending on protection, Medicare, and revenue safety applications (see right here). It is a sharp enhance from 2017, when internet curiosity funds made up nearer to 7% of presidency outlays. The rise is approaching the state of affairs skilled within the mid-Nineties when internet curiosity funds reached over 15 % of fiscal outlays (see chart). This was at a time when the general debt held by the general public as a proportion of GDP grew from 23 % to 48 %. The discount of debt funds from the mid-Nineties to the mid-2010s displays each decrease rates of interest and a decrease degree of debt. Though the debt-to-GDP ratio rose between 2009 and 2017, internet curiosity funds as a share of whole federal outlays remained beneath 7 % throughout this era primarily due to low rates of interest.

Projections of the curiosity burden of the debt have elevated dramatically over the previous 4 years.

The Congressional Funds Workplace presently initiatives that curiosity funds on debt shall be greater than 16 % of federal spending in 2034. Present projections are effectively above these made two or 4 years in the past (see chart). The variations between forecast and precise values, and the rising forecasts over time, mirror the results of adjusting expectations on each rates of interest and debt.

What this Means:

Increased curiosity funds imply much less authorities spending is offered for protection, social security internet applications, analysis, and different necessary authorities features. Rising ranges of debt service contribute to fiscal challenges that our nation faces. As curiosity funds turn out to be the next share of presidency outlays, the US might lower spending on different classes or increase tax revenues in an effort to preserve deficits from ballooning and require much more borrowing.

The price of debt service will rely upon each the extent of debt excellent and the extent of rates of interest. Debt has risen to ranges which might be excessive by historic requirements. Till lately the rise has coincided with very low rates of interest which have saved the prices of debt service comparatively low. Nonetheless, the excessive ranges of debt imply will increase in rates of interest like those who we have now seen over the previous two years can have a big impression on our nation’s price range deficits. Which the deficits might require will increase in taxes or reductions in spending.