– by New Deal democrat

It is vitally troublesome to trace the impacts of Tariff-palooza! on the US provide chain, attributable to delays in any kind of correct reporting. However under is one of the best general image I’ve been capable of decipher.

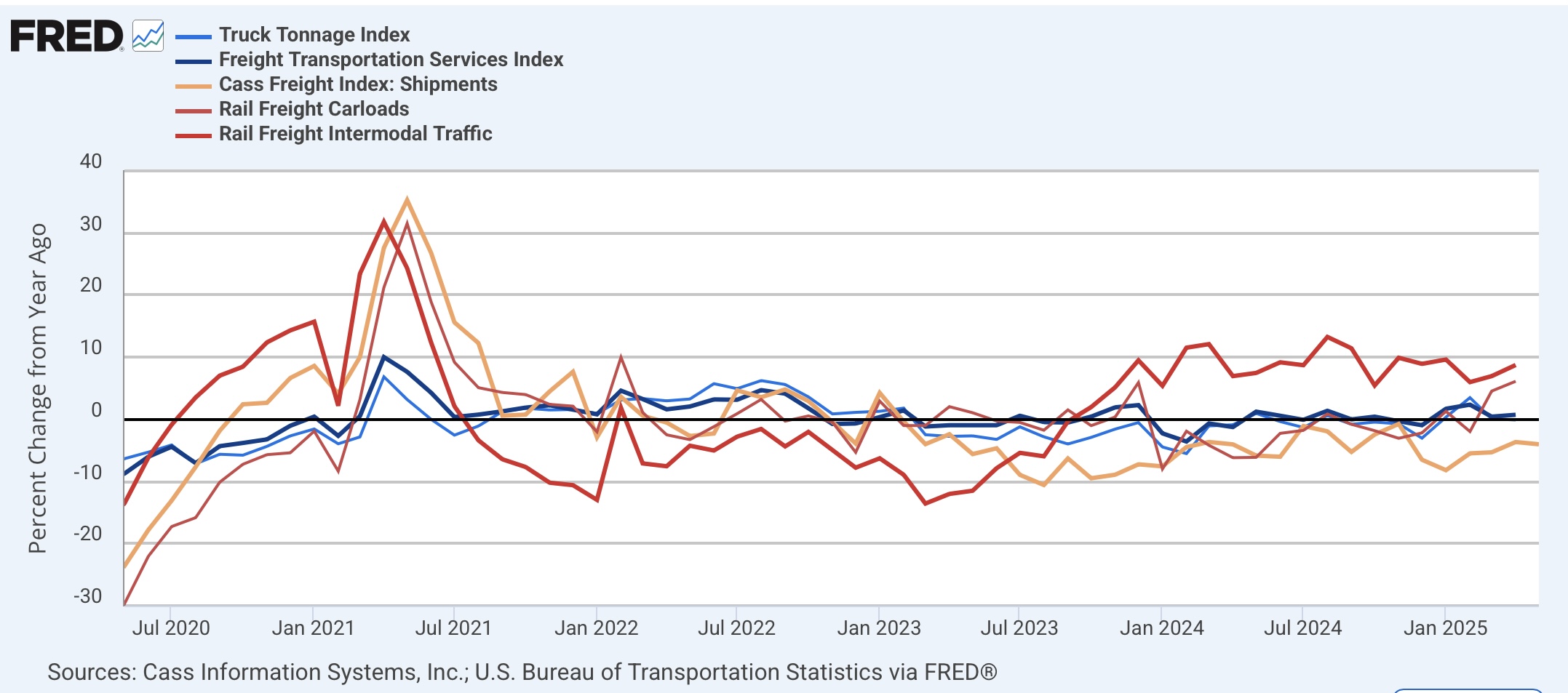

Primarily the delay is targeted on the trucking trade, as a result of rail could be very concentrated and stories intimately every week. Under is the agglomeration of intermodal (darkish crimson) and whole (mild crimson) rail site visitors, the Cass Freight Index for trucking (gold), the Truck Tonnage Index (mild blue), and the Freight Transportation Companies Index for all sorts of freight (darkish blue), all normed to 100 simply earlier than the pandemic:

Be aware that of those, solely the Cass Freight Index has been reported for Could. The remainder are solely present via April.

Earlier this week I confirmed that intermodal rail site visitors had turned unfavorable for the previous three weeks. On this week’s report, the AAR’s whole freight studying additionally turned unfavorable YoY:

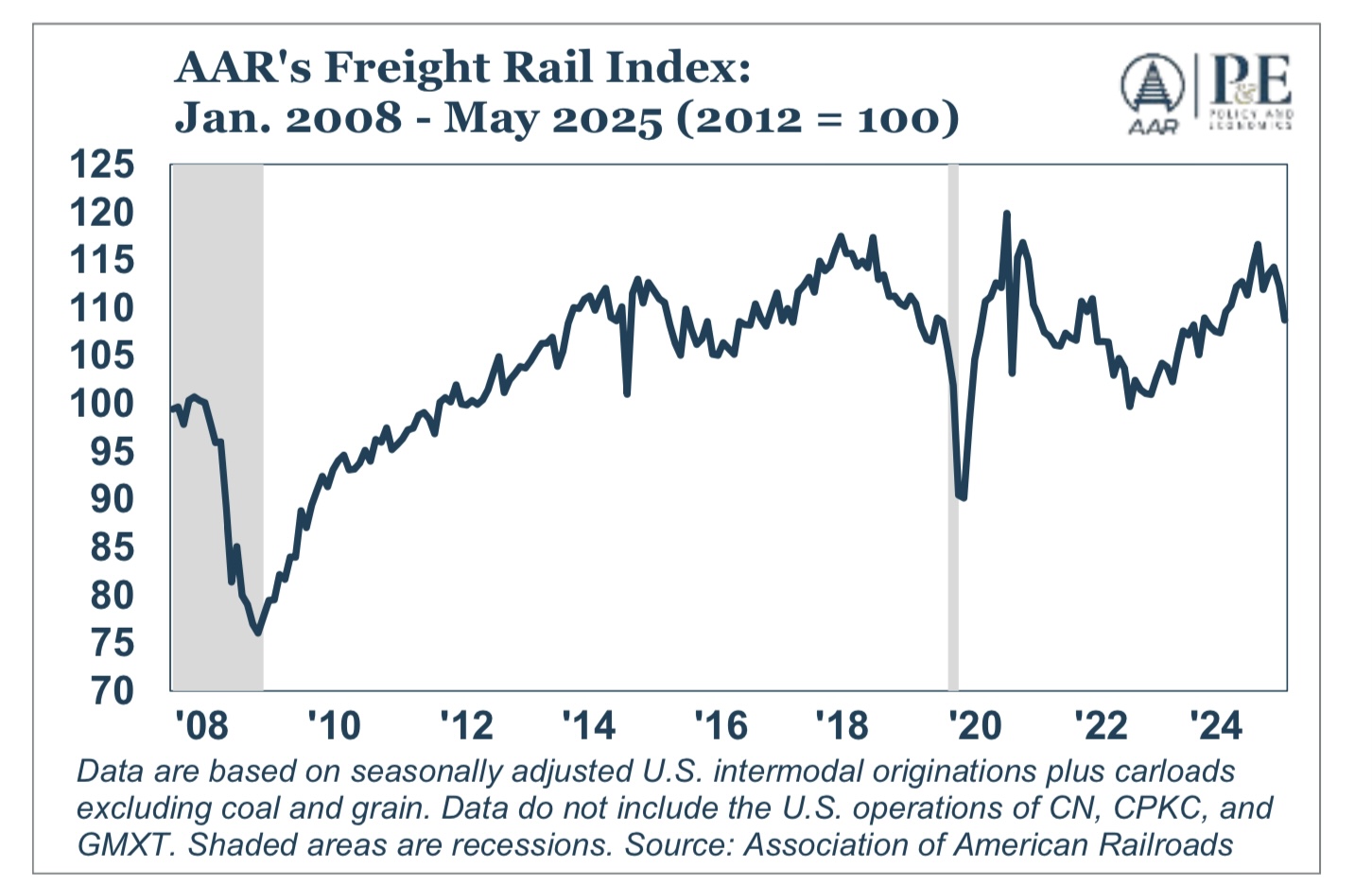

The AAR additionally stories a month-to-month graph for all hundreds besides coal and grain. Right here is the replace via Could:

It is a pretty severe turndown. Notably, coal hundreds have been nicely above final 12 months’s ranges, however the AAR ascribes that to the truth that a lot of those hundreds strikes via Baltimore, and final 12 months as you could bear in mind the fallen Francis Scott Key blocked the harbor for a number of months. Of curiosity, coal hundreds are under their 2023 numbers:

The trucking trade’s personal index was final reported in Could for April, exhibiting a month-to-month decline, however the YoY comparability was increased by 0.1%:

As they wrote: “In April, the ATA advanced seasonally adjusted For-Hire Truck Tonnage Index equaled 113.0, down from 113.3 in March. The index, which is based on 2015 as 100, was up 0.1% from the same month last year, the fourth straight year-over-year increase, albeit the smallest increase over this period.”

Their report for Could needs to be launched within the subsequent 7 to 10 days, and needs to be way more illuminating.

Traditionally, the Cass Index has been essentially the most delicate to the draw back. Because the under two graphs point out, you want the *whole* freight index, together with each rail and trucking, to say no YoY with a purpose to counsel {that a} recession is probably going:

As indicated above, the full Freight Transportation Companies Index was simply up to date this week for April. The YoY view reveals a rise of 0.7%:

That’s anemic, however it’s nonetheless optimistic. We must always have a significantly better thought of what Could regarded like as soon as the Trucking Index for Could is launched later this month.

“Tariff-palooza! Implodes – for now; but is it already too late?” Offended Bear by New Deal democrat