This text cannot get any simpler to learn and clarify how the financial system survived a pandemic from 2020 onward and even into 2024. With the best actions by a president and supported by a Congress, the nation survived and it grew. In summation? The “economy has had a remarkable four-year run, judged against both its own history or the international competition.”

If you happen to disagree, this one has few technical particulars to confuse the problems. Make your pitch.

Excellent news outdoors of inflation.

Atlantic article “The US Economy Reaches “Superstar Status,” Rogé Karma . . . “if the USA’ financial system had been an athlete, proper now it could be peak LeBron James. If it had been a pop star, it could be peak Taylor Swift. 4 years in the past, the pandemic quickly introduced a lot of the world financial system to a halt.

Since then, America’s financial efficiency has left different international locations within the mud and even damaged a few of its personal information. The expansion fee is excessive, the unemployment fee is at historic lows, family wealth is surging, and wages are rising quicker than prices . . . particularly for the working class. There are numerous methods to outline a very good financial system. America is in great form in response to nearly any of them.

The American public doesn’t really feel that means—a dynamic that many individuals, together with me, have lately tried to elucidate. If, as an alternative of asking how folks really feel in regards to the financial system, we ask the way it’s objectively performing, we get a really totally different reply.

Let’s begin with economists’ favourite metric: progress. When an financial system is rising, more cash is being spent. Extra stuff is being produced, extra providers are being carried out, extra companies are being began, extra staff are being employed. Due to this abundance, dwelling requirements are most likely rising. (On the flip aspect, throughout a recession—actually, when the financial system shrinks—life will get materially worse.)

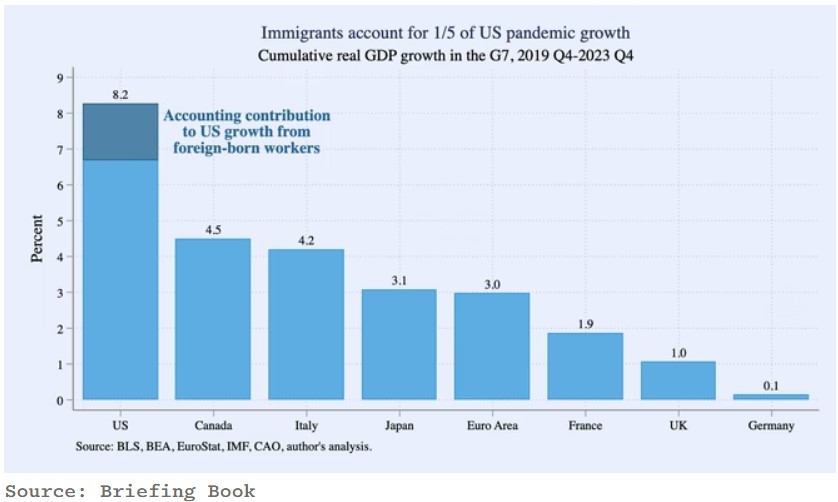

Proper now America’s economic-growth fee is the envy of the world. From the top of 2019 to the top of 2023, U.S. GDP grew by 8.2 p.c. That is almost twice as quick as Canada’s, thrice as quick because the European Union’s, and greater than eight instances as quick as the UK’s.

“It’s hard to think of a time when the U.S. economy has diverged so fundamentally from its peers,” Mark Zandi, the chief economist at Moody’s Analytics, instructed me. Over the previous 12 months, a number of the world’s greatest economies, together with these of Japan and Germany, have fallen into recession, full with mass layoffs and offended avenue protests. Within the U.S., nevertheless, the post-pandemic recession by no means arrived. The financial system simply retains rising.

Nonetheless, progress is a crude measure that claims little or no about folks’s day-to-day lives. Maybe the best query to ask is:

Are most People higher off financially than they had been earlier than the pandemic?

One college of thought maintains that the reply is not any, due to the rising price of dwelling. Thanks to 3 years of higher-than-usual inflation, nearly every thing prices greater than it did earlier than the pandemic.

Value will increase on their very own cannot inform us if the price of dwelling has gone up. What actually issues is the connection between how costly issues are and the way a lot cash folks must spend on them. As Vox’s Eric Levitz lately identified, costs have elevated by 1,400 p.c since 1947; that doesn’t imply People have much less shopping for energy at the moment than at a time when a third of the nation didn’t have operating water and 40 p.c lived in poverty.

That’s largely as a result of incomes have elevated by 2,400 p.c over the identical stretch. If costs go up however folks’s incomes go up quicker, then the price of dwelling decreases. And that’s precisely what has occurred within the U.S. over the previous 5 years.

It took a while. When inflation was at its worst, in late 2021 and 2022, costs had been rising too quick for staff’ pay to maintain up. Over the course of 2023, nevertheless, the speed of inflation plummeted whereas wages stored rising. In keeping with calculations by the economist Arindrajit Dube, costs rose about 20 p.c from the start of the pandemic to the top of 2023. The median employee’s hourly wages elevated by greater than 26 p.c. In different phrases, a greenback in 2024 may not go so far as a greenback in 2019, however at the moment the typical employee has so many extra {dollars} they will afford the next high quality of life.

Some specialists dispute this. Loretta Mester, the president of the Cleveland Federal Reserve, lately instructed The New York Occasions wage progress hadn’t stored tempo with inflation. Mester was citing an indicator that tracks adjustments in compensation inside explicit industries. However one of the crucial widespread methods for staff to get a elevate is to maneuver between industries, from lower- to higher-paying occupations. That is the best way somebody working as a fry prepare dinner, say, would possibly subsequent take a job as a package-delivery driver. Principally, each different measure of employee pay reveals wages adjusted for inflation are greater at the moment than they had been earlier than the pandemic. Dube’s calculations are significantly dependable as a result of they’re primarily based on a dataset monitoring wages for particular person staff over time.

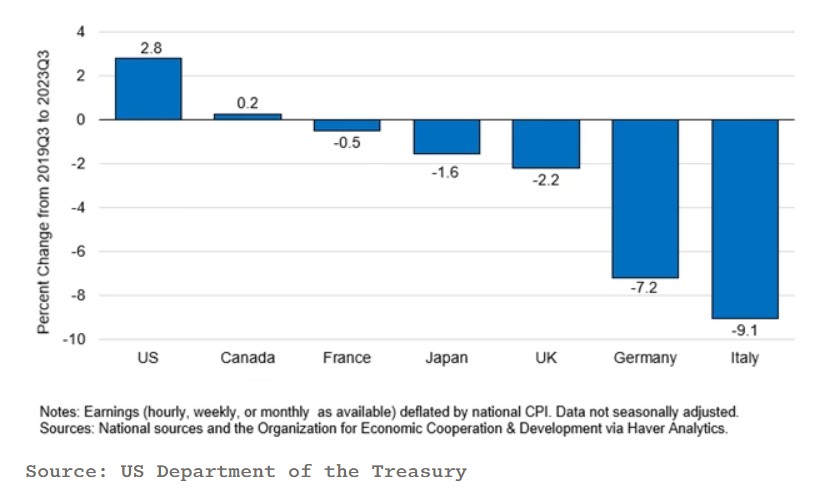

Different nations most likely would love the posh of debating such technicalities. From the start of the pandemic by the autumn of 2023 (the final interval for which we’ve good comparative knowledge), actual wages in each Europe and Japan fell. In Germany, staff misplaced 7 p.c of their buying energy; and in Italy, 9 p.c. By these metrics, the one staff in the whole developed world who’re meaningfully higher off than they had been 4 years in the past are American ones.

Averages can conceal rather a lot, after all. The rise in inflation-adjusted wages, which economists name “real wages,” may not be such excellent news if it had been flowing principally to the already-wealthy, because it did through the restoration from the Nice Recession (2008). Actually, from 1964 by 2018, actual wages for many staff hardly budged. Virtually all good points went to the richest People. Within the early days of the pandemic, when hundreds of thousands of low-income staff discovered themselves abruptly out of a job, it could have been affordable to count on the identical pattern to play itself out.

As a substitute, the alternative occurred. A current evaluation from the Financial Coverage Institute discovered that from the top of 2019 to the top of 2023, the lowest-paid decile of staff noticed their wages rise 4 instances quicker than middle-class staff and greater than 10 instances quicker than the richest decile. A current working paper by Arindrajit Dube and two co-authors reached comparable conclusions.

Wage good points on the backside, they discovered, have been so steep that they’ve erased a full third of the rise in wage inequality between the poorest and richest staff over the earlier 40 years. This discovering holds even whenever you account for the truth that lower-income People are likely to spend the next proportion of their earnings on the gadgets which have skilled the most important value will increase in recent times, similar to meals and fuel. Arindrajit Dube, “We haven’t seen a reduction in wage inequality like this since the 1940s.”

Pay in America is turning into extra equal alongside race, age, and training traces. The wage hole between Black and white People has shrunk to its lowest level since no less than the Eighties. Pay for staff youthful than 25 has elevated twice as quick as older staff’ pay. The so-called faculty wage premium which is the pay hole between these with and with out a faculty diploma, has shrunk to its lowest measure in 15 years. (The gender pay hole has additionally narrowed barely, however far lower than the others.)

What explains this sudden enhance in lower- and middle-class wages?

The reply lies within the post-pandemic American labor market, which has been unbelievably robust. The unemployment fee (outlined as the share of staff who’ve lately regarded for a job however don’t have one) has been at or beneath 4 p.c for greater than two years. The longest streak because the Nineteen Sixties. Even that understates simply how good the present labor market is. Unemployment didn’t fall beneath 4 p.c at any level through the Nineteen Seventies, ’80s, or ’90s. In 1984—the 12 months Ronald Reagan declared “It’s morning again in America”—unemployment was above 7 p.c; for a lot of the Clinton increase of the Nineteen Nineties, it was above 5 p.c.

The plain upside of low unemployment is, individuals who need jobs can get them. A extra delicate consequence, and arguably a extra vital one, is a shift in energy from employers to staff. When unemployment is comparatively excessive, because it was within the years instantly following the 2008 monetary disaster, extra staff are competing for fewer jobs, making it simpler for employers to demand greater {qualifications} and supply meager pay.

That’s how you find yourself with tales about faculty graduates working as baristas for $7.25 an hour. However when unemployment is low and comparatively few persons are on the lookout for jobs, the connection inverts: Now employers must compete in opposition to each other to draw staff, usually by elevating wages. That is the essential half, these dynamics have an effect on all staff, not simply people who find themselves out of a job.

This helps clarify what occurred after the pandemic. When the financial system first reopened, employers abruptly needed to fill hundreds of thousands of positions. In the meantime, staff—flush with stimulus checks and expanded unemployment insurance coverage might say no to dangerous jobs. In response, even famously low-paying corporations similar to Amazon, Walmart, and McDonald’s began elevating wages and providing new advantages to draw workers. What was misleadingly labeled the “Great Resignation” was actually extra of an excellent reshuffling, as report numbers of staff stop a job to take a better-paying one. Over the subsequent couple of years, as American shoppers stored spending cash, demand for labor stayed excessive.

Betsey Stevenson, a labor economist on the College of Michigan, instructed me.

“Low-wage workers are finally getting a small taste of the bargaining power that highly paid professionals experience most of the time.”

Up to now, we’ve been speaking about wages: the cash persons are paid by their employer. To higher seize general monetary well-being, we would as an alternative take a look at family wealth, which takes under consideration the total vary of individuals’s money owed and property. Over the previous few years, People have skilled the most important surge in wealth in no less than three many years.

The gold commonplace for analysis into the state of People’ funds is the Federal Reserve’s Survey of Shopper Funds, launched each three years. The most up-to-date report discovered that, from 2019 to 2022, the web value of the median family elevated by 37 p.c, from about $141,000 to $192,000, adjusted for inflation. That’s the most important three-year enhance on report because the Fed began issuing the report in 1989, and greater than double the next-largest one on report. (In keeping with preliminary knowledge from the Fed, wealth continued to rise throughout the board in 2023.) Each single earnings bracket noticed internet value enhance significantly, however the greatest good points went to poor, middle-class, Black, Latino, and youthful households, producing a slight discount in general wealth inequality (although not almost as steep a discount because the decline in wage inequality). By comparability, median family wealth really declined by 19 p.c from 2007 to 2019.

An vital caveat to the wealth statistics is far of the current enhance got here from the surge in residence costs. A household wealthier on paper may not really feel wealthy in the event that they must promote their residence to appreciate any good points. Particularly, if all of the locations they may wish to transfer to have gotten equally costly.

Certainly, the out-of-control price of housing is maybe the most important black mark on an in any other case wonderful financial system. This drawback began many years in the past because the Eighties. The median U.S. residence value has elevated by greater than 400 p.c, twice as quick as incomes, and was even worse through the pandemic. The rise of distant work prompted hundreds of thousands of individuals to hunt more room. These rising costs have collided with greater rates of interest to supply the most punishing housing market in no less than a era. Would-be householders can’t afford to purchase, and plenty of current householders really feel caught in place.

Housing is one in all a number of essential classes, together with childcare, well being care, and better training. All have ballooned in price in current many years, placing a middle-class life-style additional and additional out of attain. My colleague Annie Lowrey callsit the “Great Affordability Crisis.”

The previous few years of excessive rates of interest making borrowing cash costlier, have jacked up prices much more. And regardless of the current excellent news, the U.S. nonetheless has decrease life expectancy and far greater ranges of inequality, poverty, and homelessness than different rich nations. For hundreds of thousands of individuals, getting by in America was a battle earlier than the pandemic and continues to be a battle at the moment.

Nonetheless the actual fact is, the U.S. financial system has had a exceptional four-year run, judged in opposition to each its personal historical past or the worldwide competitors. Even so a couple of years of fine information, nonetheless isn’t sufficient to make up for 40 years of rising inequality and stagnant wages. But it surely’s a complete lot higher than the choice.