Protection denials as reported by the Commonwealth Fund as we speak virtually by no means occurred up to now and was a uncommon incidence. The insurance coverage corporations would concede to the findings of the inspecting docs. The methodology getting used as we speak is to disclaim, deny, deny till the insured and the physician hand over. I believe it was 1997 when a fictional story “The Rainmaker” grew to become a film, The difficulty was a bone marrow transplant which was denied by the healthcare insurance coverage firm Nice Profit The film was a take off of John Grisham (labored on the Obama election group) “The Rainmaker.” An excellent learn in case you are sitting on a jet going to China for 13-14 hours.

As Commonwealth reviews, Individuals are struggling in an try to get their medical insurance to work for them. Excessive deductibles and copayments are inflicting ~ two of 5 working-age adults to delay visiting the physician and having prescriptions1 crammed. These getting care generally discover themselves burdened by medical or dental debt. Virtually one-third of working-age adults report experiencing 2 situations of such. Billing errors and denials of protection by insurance coverage corporations can contribute to this downside. Media investigations discover insurers have gotten more and more adept in utilizing know-how to disclaim cost of medical claims. In flip they stress their firm physicians to disclaim care throughout prior authorization evaluations.3 Medical doctors are reporting spending rising quantities of time on the telephone with insurance coverage firm physicians over denials of care for his or her sufferers.4

Introduction

On this temporary, Commonwealth Fund reviews on findings from a survey on the extent to which working-age adults say their insurance coverage supplier charged them for a well being service. A service which they thought needs to be free or lined or denied protection for care as really useful by their docs. Commonwealth Fund examines whether or not the insured challenged such errors or protection denials, the explanation why they didn’t, and the implications for his or her well being and well-being. Individuals had been grouped by the protection supply they reported on the time of the survey. This may very well be an employer or particular person market or market. It’s famous that some have switched insurance policy throughout the 12 months.

That is an abbreviated model of your entire Commonwealth Fund report. The remainder of the report may be discovered at:

Unexpected Well being Care Payments Protection Denials by U.S. Insurers.

Some Highlights

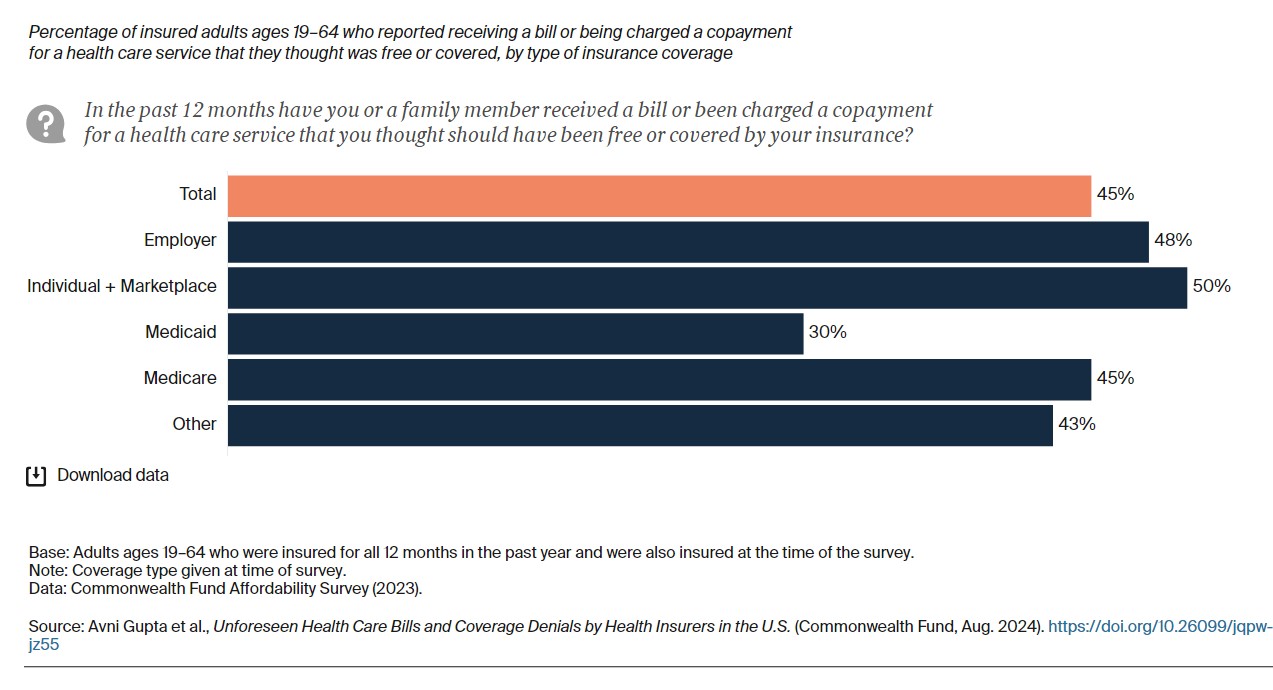

- Forty-five % of insured, working-age adults obtained a medical invoice or had been charged a copayment up to now 12 months for a service they thought ought to have been free or lined.

- Lower than half of these reporting billing errors stated they challenged them. Lack of expertise about their proper to problem a invoice was the most typical purpose, significantly amongst youthful folks and people with low earnings.

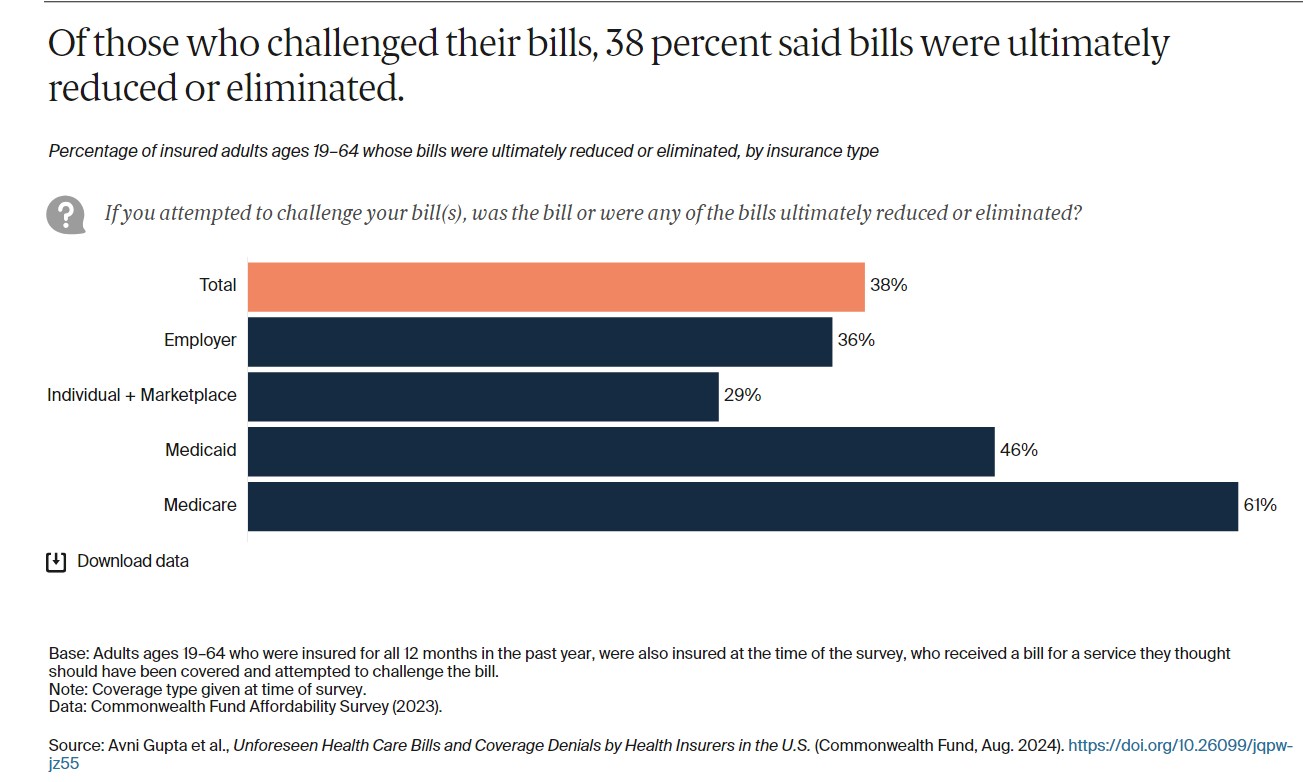

- Practically two of 5 respondents who challenged their invoice stated that it was in the end diminished or eradicated by their insurer.

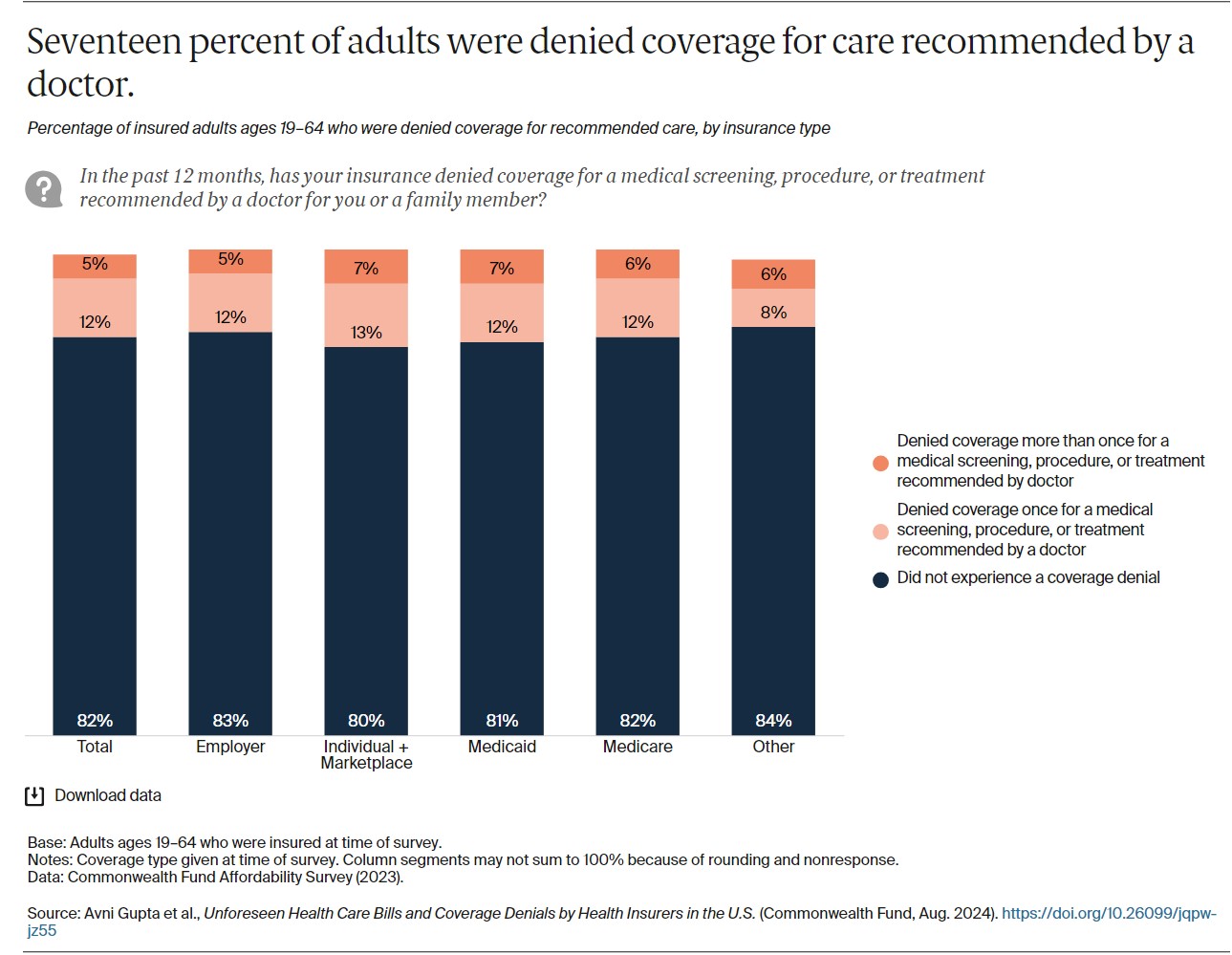

- Seventeen % of respondents stated their insurer denied protection for care really useful by their physician. Greater than half stated neither they nor their physician challenged the denial.

- Practically six of 10 adults who skilled a protection denial stated their care was delayed consequently.

Findings

Greater than two of 5 respondents reported both they or a member of the family obtained a invoice or had been charged a copayment up to now 12 months for a well being service they thought was free or lined by their insurance coverage.

Plan complexity and the heterogeneity of advantages throughout plans could go away folks unable to determine what’s and isn’t lined, and when a invoice is inaccurate.5 Whereas the Reasonably priced Care Act (ACA) requires all insurers to cowl preventive companies like colon most cancers screening freed from cost, some states and the federal authorities additionally require sure plans, corresponding to market plans, to cowl further companies both freed from cost, like annual checkups, or previous to assembly deductibles. Many employer plans exclude some companies and prescribed drugs from deductibles.

Individuals throughout all insurance coverage sorts reported such billing issues, however these lined by employer plans, market or particular person market plans, and Medicare reported them at greater charges.

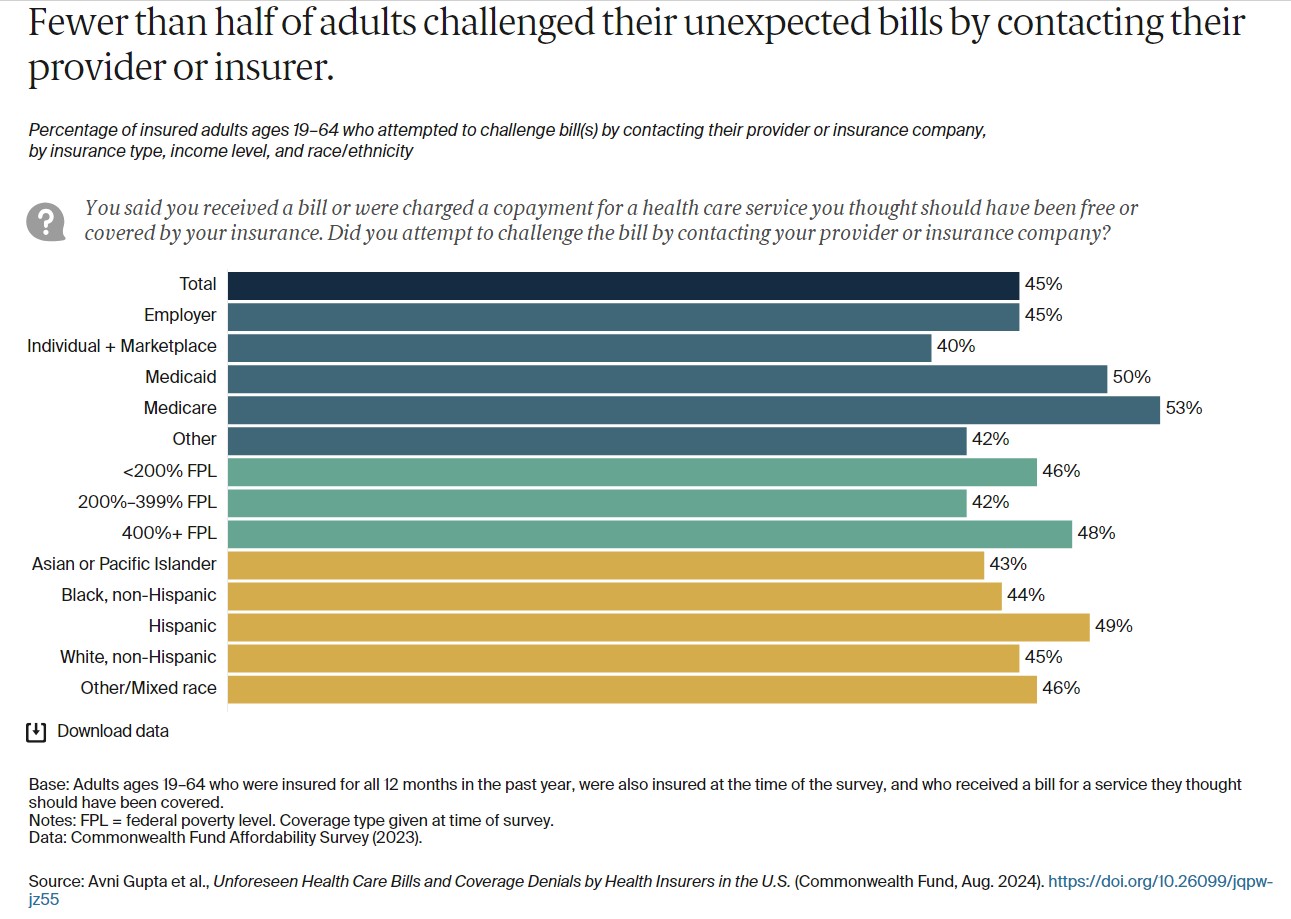

Of the respondents considering they obtained a invoice in error, fewer than half tried to problem the invoice. Individuals with market or particular person market plans challenged these payments at a price decrease than these lined by Medicaid or Medicare (the distinction was not statistically vital). This, regardless of the ACA’s requirement for insurers to have methods in place for shoppers to attraction and problem their payments. There have been no vital variations by race and ethnicity or poverty stage.

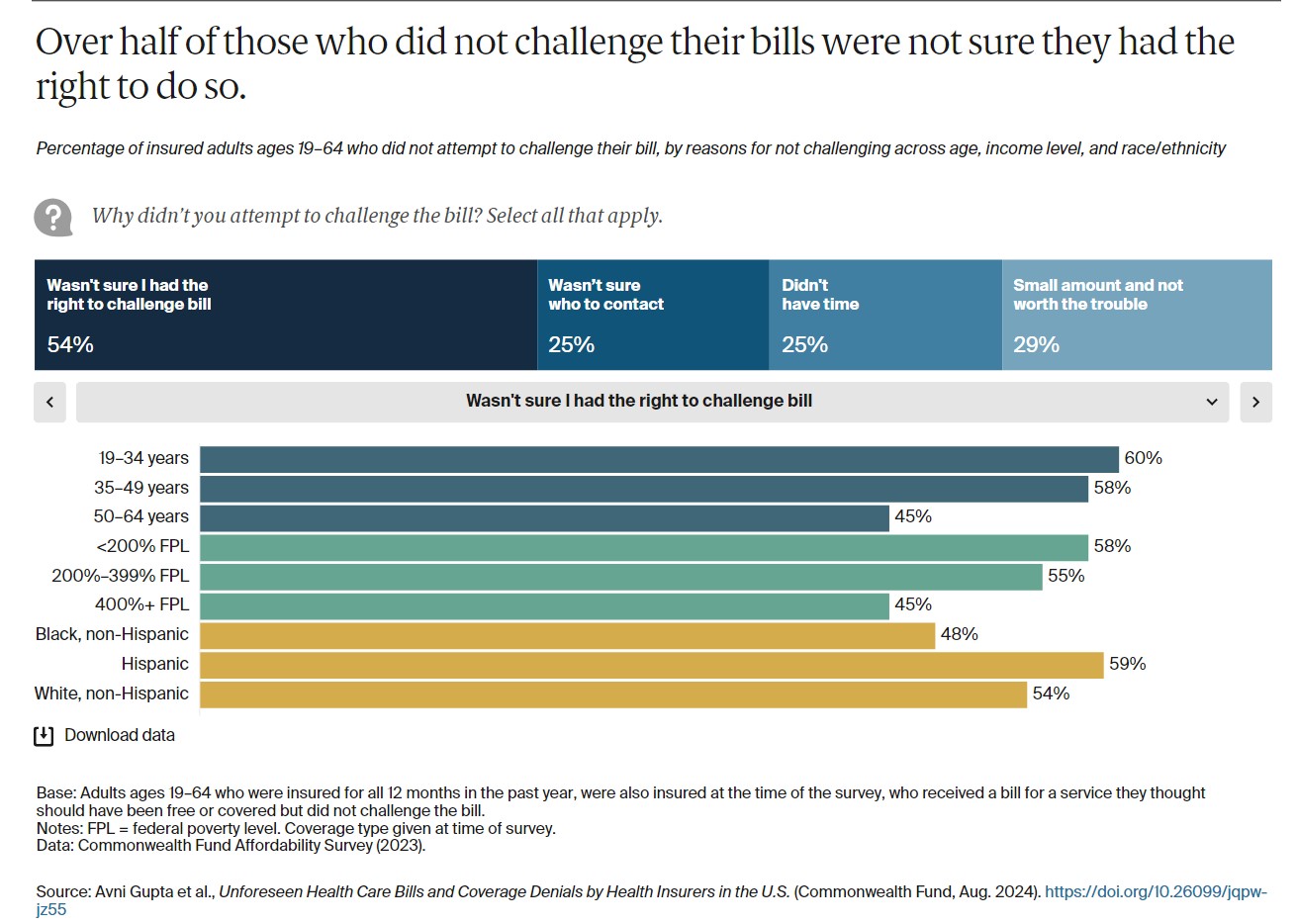

– Of those that didn’t problem their payments, over half stated it was as a result of they weren’t certain they’d the correct to take action. Different causes included not figuring out who to contact (25%), missing the time (25%), and viewing the quantity as too small to spend time difficult the invoice (29%).

– Individuals with low and reasonable incomes, these youthful than age 50, and Hispanic respondents reported on the highest charges that they had been uncertain of their proper to problem a invoice. These youthful than 50 additionally had the very best charges of not figuring out who to contact to problem a invoice.

– Individuals with greater earnings cited a scarcity of time and the quantity not being definitely worth the bother at greater charges than these with low or reasonable earnings.

Practically two of 5 adults difficult a invoice stated the quantity was in the end diminished or eradicated. Individuals with Medicare or Medicaid reported greater charges of invoice discount or elimination. This will likely mirror extra standardized and well-defined advantages in public applications in comparison with the heterogeneity of plan merchandise and advantages supplied by employers and business insurers.

Protection Denials

Seventeen % of respondents or certainly one of their relations had been denied protection for care really useful by a physician, and these charges had been related throughout insurance coverage sorts. Whereas we didn’t ask survey respondents why their protection was denied, frequent causes embody a service that’s deemed medically pointless by the insurer or delivered in a setting the insurer considers inappropriate, visiting an out of community supplier, a medicine that’s not on a plan formulary, or an experimental process.

Many well being insurers require a evaluation of claims or prior authorization requests by a nurse and a physician, each employed by the insurer.6 Current media investigations have discovered that some insurance coverage firm docs should not incentivized to spend the time wanted to scrutinize sufferers’ medical information and observe tips for making knowledgeable selections about approving or denying a care request.7 Slightly, some docs are incentivized to disclaim care utilizing a “click and close” coverage, which promotes bonuses primarily based on the amount of circumstances reviewed and therefore incentivizes speedy evaluations. This will result in wrongfully denied care.8