Discussing US Debt seemed attention-grabbing sufficient to publish on Indignant Bear. I don’t agree with the proposed fixes as I consider there are different fixes which might resolve the problems talked about. Maybe you’ve gotten higher concepts?

Addressing Rising US Debt

by Karen Dynan

The Concern:

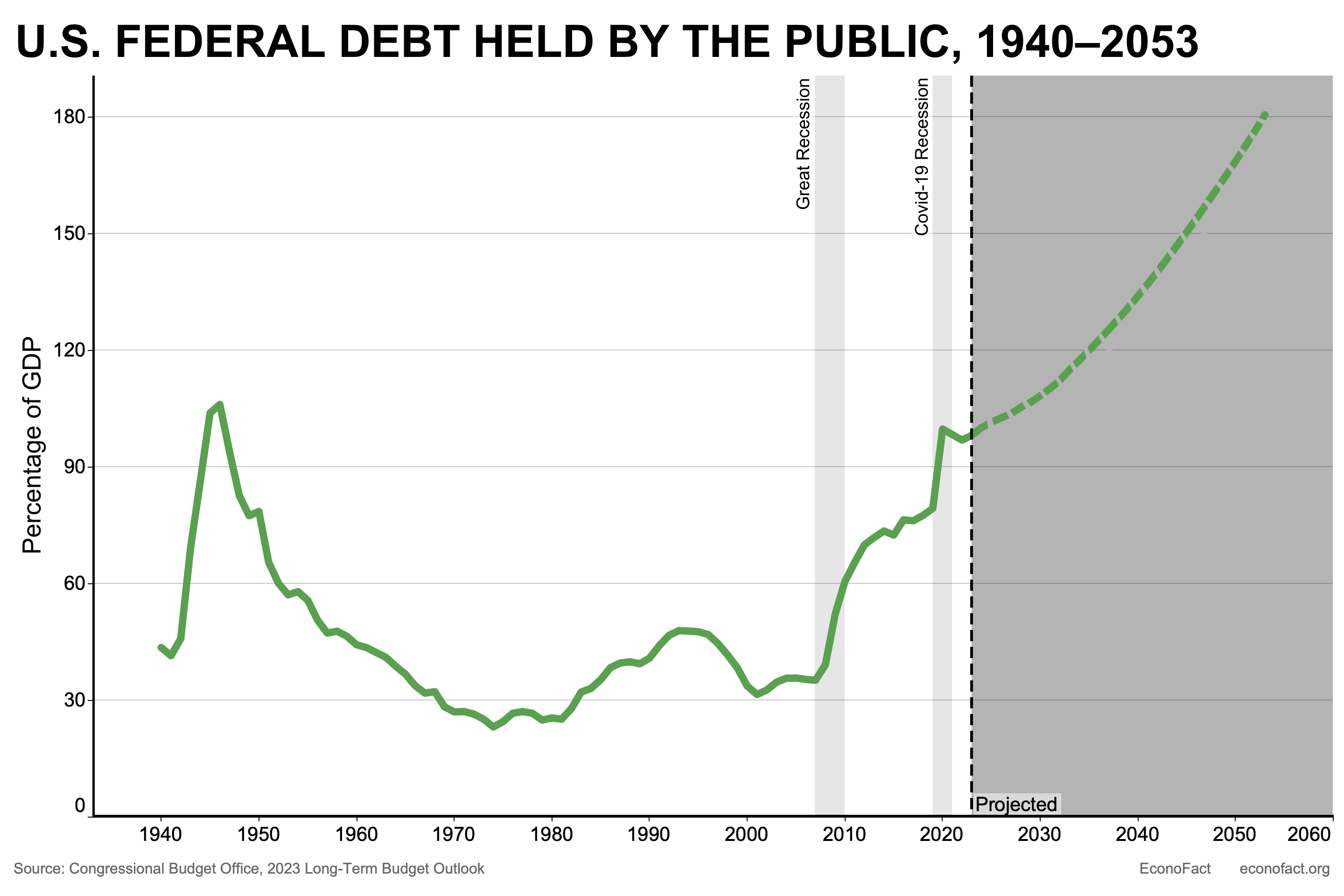

United States Federal debt rose sharply after the Nice Recession. At 98% of gross home product (GDP) in 2023, it’s near its highest degree ever. Underneath present coverage, the federal debt is anticipated to proceed rising over the subsequent three many years to achieve ranges properly above any historic expertise. It holds true even underneath optimistic assumptions about future financial situations. To maintain the federal debt from ballooning to the degrees at the moment predicted, a more in-depth alignment of presidency spending and revenues must happen in coming years. Adjustments in coverage considerably narrowing the federal deficit going ahead might have financial and political disadvantages. Adjustments shall be wanted, as unprecedented ranges of presidency debt impose important financial prices and dangers.

The Information:

Detrimental financial shocks and coverage adjustments over the previous twenty years have shifted present and projected ranges of federal debt to greater ranges.

The US has seen two important hostile shocks to financial exercise within the twenty first century. The deep and extended Nice Recession starting in 2007 on account of the world US monetary disaster and the sharp financial downturn that adopted the onset of the COVID-19 pandemic in early 2020. These episodes led to drops in financial exercise and decrease tax revenues and, on the identical time. Will increase in federal spending on restoration applications contributed. A long-lasting downshift in authorities revenues caused by main adjustments in tax coverage nonetheless contributes to greater ranges of debt. The adjustments in tax coverage embody the extension of tax cuts from early within the first decade of the 2000s and tax cuts enacted within the Tax Cuts and Jobs Act of 2017. If the provisions of the 2017 tax cuts scheduled to run out within the subsequent few years had been to be prolonged, the projected path of tax revenues would shift additional down. A rise between $400 billion and $500 billion per yr within the late 2020s and early 2030s.

Behind the projected surge in US federal debt over the subsequent three many years is an anticipated improve of the federal funds deficit, which is at the moment excessive and projected to rise steeply underneath present legislation.

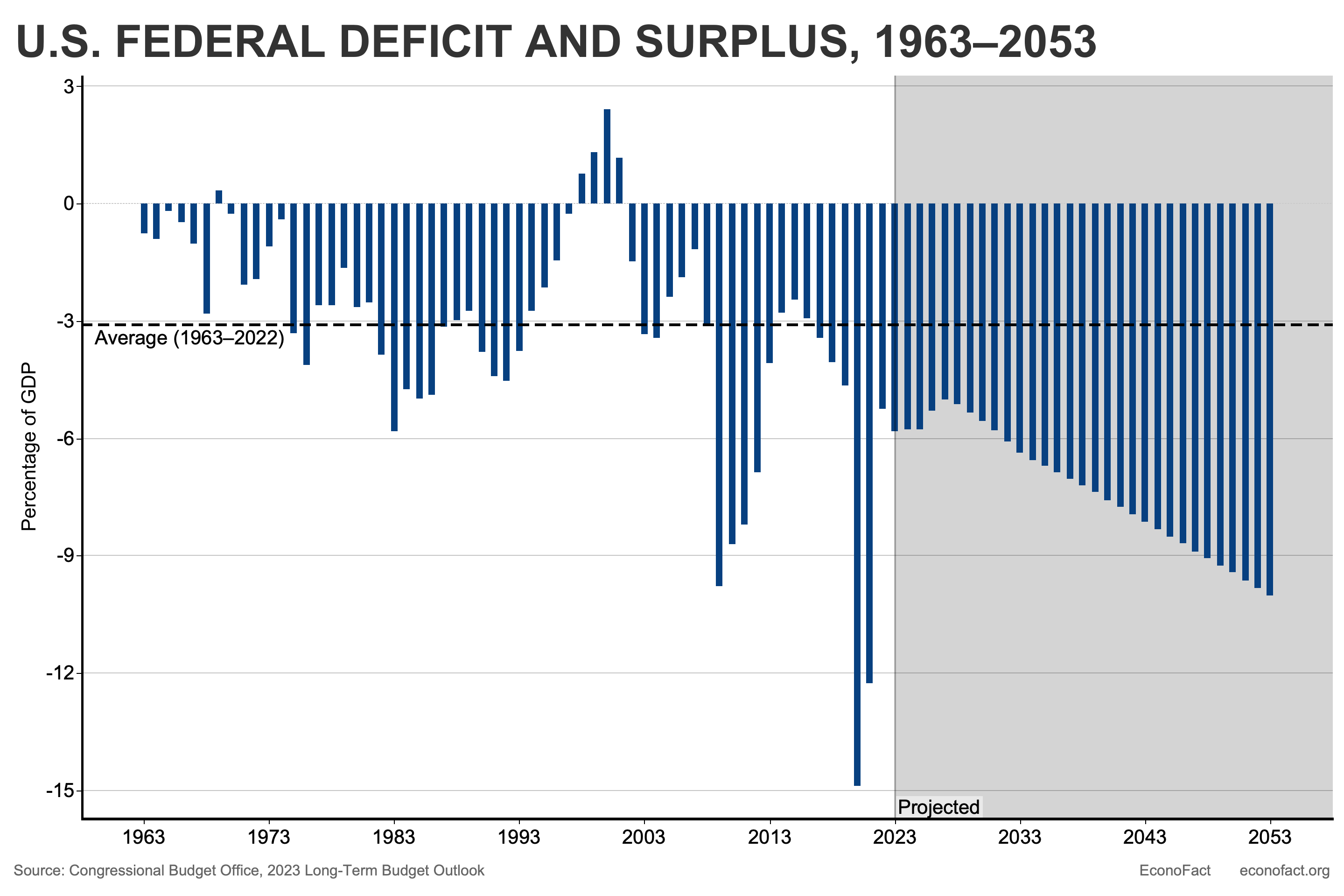

Briefly; federal funds deficit happens when federal authorities spending exceeds its revenues. The federal government must borrow in an effort to make up the distinction. The federal debt is the buildup of federal funds deficits over time. It’s not unusual for the US federal authorities to have a funds deficit. Having deficits modest in dimension is sustainable given progress within the financial system. Nevertheless, the present dimension of the federal deficit, whereas smaller than its pandemic highs, is massive by historic requirements (chart under). Furthermore, the funds deficit is projected to climb a lot greater over the subsequent three many years, reaching 10% of GDP by 2053.

The growing old US inhabitants is a key issue contributing to greater projected authorities spending.

The proportion of the US inhabitants aged 65 and older grew from about 12% within the first decade of the 2000s to 17% in 2023. Projections point out an extra improve to 22% by 2050. An rising older inhabitants would require important federal help for each revenue and well being care (see right here and right here). The Congressional Price range Workplace (CBO) has projections utilizing present coverage. By 2053, the CBO initiatives Social Safety outlays will rise by practically 1% of GDP. It additionally initiatives spending on main federal healthcare applications, together with Medicare, will rise by 3% of GDP. Spending on Social Safety and federal well being care applications will quantity to fifteen% of GDP by 2053. This improve will drive the first deficit (the deficit excluding curiosity funds on our present debt) greater.

Ongoing massive main deficits, together with an already-high degree of debt and curiosity prices, result in a dramatic snowball impact over time.

A excessive degree of accrued debt and better rates of interest imply curiosity funds on our debt are an rising a part of federal spending. Ongoing massive main deficits generate extra debt resulting in mounting curiosity prices. This in flip results in a further improve within the whole deficit and debt. Underneath the belief authorities borrowing charges stay at ranges considerably greater than the degrees of the late 2010s, the CBO estimates that greater curiosity prices will push up the general deficit by a further 4% of GDP by 2053. Absent coverage adjustments, this dynamic will push the deficit and debt ever greater even within the years past CBO’s window.

These structural challenges imply that even “good luck” with financial developments that might mitigate the debt burden, akin to excessive productiveness or low rates of interest, won’t put the debt on a sustainable path.

Progress Estimates of federal debt over time depend upon assumptions about tendencies in productiveness and rates of interest and different elements. Larger-than-expected productiveness progress results in greater GDP progress, which in flip reduces the burden of upper debt. Nevertheless, even underneath probably the most optimistic situation for productiveness progress estimated by the CBO, the federal debt would improve to 137% of GDP by 2053 or properly above the historic vary. The identical is true for probably the most optimistic rate of interest situation thought-about by the CBO. An rate of interest path that begins 5 foundation factors decrease than baseline in 2023, with the hole then rising by 5 foundation factors per yr, nonetheless leads to the federal debt held by the general public in 2053 rising to 143 % of GDP (see right here). These analyses underscore that even favorable macroeconomic outcomes are most unlikely to vary the conclusion that federal debt is on an unsustainable path.

The projected path of US federal debt presents important financial prices and dangers.

First, elevated borrowing by the federal government crowds out borrowing by households and companies. The competitors for funds drives up rates of interest, making it costlier for people and companies to borrow. Consequently, personal funding in productive capital decreases, resulting in decrease future output and nationwide revenue. Second, elevated borrowing raises the chance of a fiscal disaster. If buyers turn out to be reluctant to lend cash to the federal government as a result of they worry the debt won’t be repaid, authorities borrowing charges can rise out of the blue as potential lenders demand extra compensation to carry authorities debt. Lastly, greater debt additionally comes with the prices of lowered “fiscal space,” that means a restricted capability to extend the funds deficit, even quickly, with out endangering the entry of a rustic’s authorities to monetary markets or the sustainability of its debt. A scarcity of fiscal area constrains a rustic’s capability to successfully deal with sudden home wants, akin to financial crises or pandemics, in addition to worldwide threats.

Most of the coverage adjustments that would assist put the debt on a sustainable path have disadvantages, so selections will should be made fastidiously.

A lot of our federal spending applications serve vital functions akin to selling financial progress, fostering financial mobility, mitigating hardship, and defending nationwide safety. Massive will increase in taxes wouldn’t be standard, and a few such adjustments could lead on folks to work much less, save much less, make investments much less, and innovate much less.

What this Means:

The problem posed by excessive and rising federal debt is critical however manageable as a matter of economics. For instance, CBO initiatives {that a} mixture of reductions in noninterest spending and will increase in taxes that cut back the deficit by a median of two.8% of GDP in coming many years could be anticipated to maintain the ratio of debt to GDP at its present degree; alternatively, decreasing the deficit by a median of three.3% of GDP over the 2027 to 2052 interval (which might stability the first deficit) would lead to a gradual decline within the debt relative to GDP over time. Policymakers might want to fastidiously weigh the financial tradeoffs as they make the wanted adjustments to spending and taxes. However the greatest impediment to addressing excessive and rising federal debt could also be political. Guarantees to not contact substantial key federal spending applications or to boost taxes are standard, however they can’t all be realized if we’re to place the funds on a sustainable path.