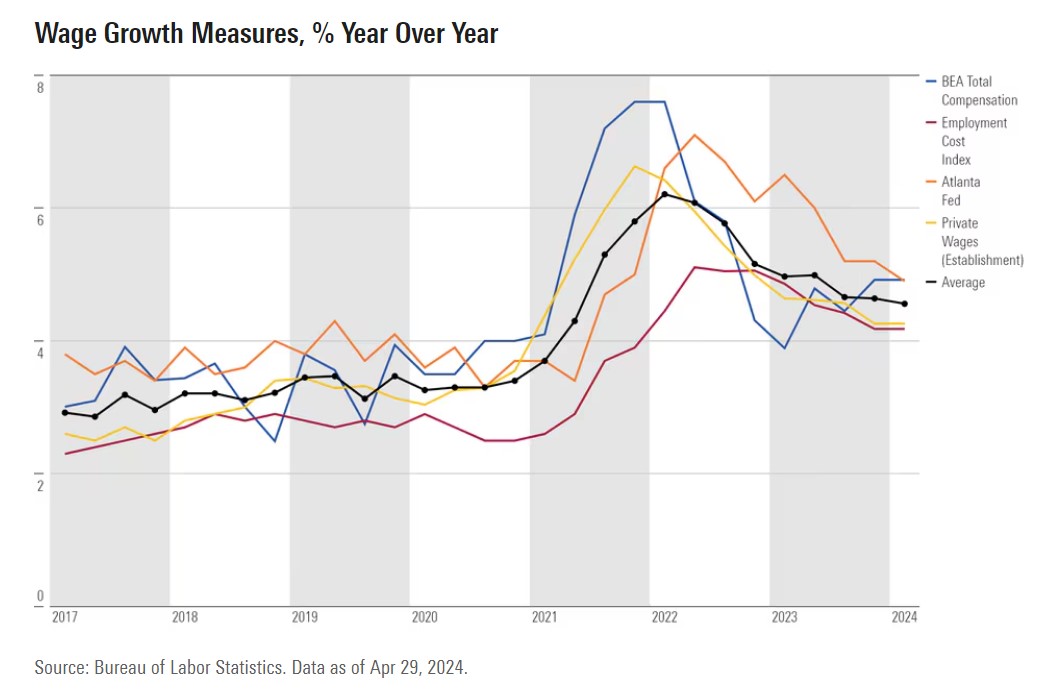

This specific graph was pulled from an April 2024 Morning Star article. The supply of it being the Bureaus of Labor Statistics. It depicts wage progress earlier than throughout and after the Pandemic. Specifically I imagine the federal government did fairly effectively in offering for and defending its residents through the pandemic when many individuals couldn’t work. The stimulus packages might have triggered among the wage progress and inflation. There are different factor that are happening additionally.

Others might argue the purpose. It seems the Democrats and Biden’s stimulus packages rescuing the inhabitants as an entire had an impression on the nation’s enterprise additionally, labor, and wage progress. Not a 2008-10 decelerate this time. Even so, wage progress peaked in 2022 at ~8% (BLS) and is now at ~5% (BLS) as depicted (YOY).

Hourly wage progress averaged a 4.1% annualized charge previously three months 2024. A small improve over the 4.0% charge within the earlier three months. Yr-over-year progress charge decreased barely to 4.1% as of March. That is down from a excessive of 5.9% in March 2022. Nonetheless, the FED holding its charge excessive anticipating it to gradual the economic system.

We’re starting to see the impression of the Fed’s makes an attempt. The economic system slows and labor openings are fewer. I’d additionally anticipate wage progress to proceed to lower, job openings lower, and layoffs improve as Powell holds the Fed Price at 5.25-5.5%.

Nonetheless, New Deal democrat and Offended Bear don’t imagine Labor is the foremost reason behind inflation. If I had been to decide on, I’d first take a look at inventories and capability to see if there’s a actual bottleneck in manufacturing attributable to pure points. It will not shock me if firms had been gradual to restock inventories to enhance pricing. In 2010, semiconductors was a difficulty and corporations arbitrarily elevated costs on a take it or go away it foundation. This was commonplace.

When you learn New Deal democrat’s (NDd) commentary, Immigration and the housing market freeze are making the “last mile” of disinflation more durable, not the Phillips Curve (additionally on Offended Bear), he offers an evidence for the cussed Inflation Price Powell is making an attempt to defeat or deliver down. It’s laborious to be temporary on this.

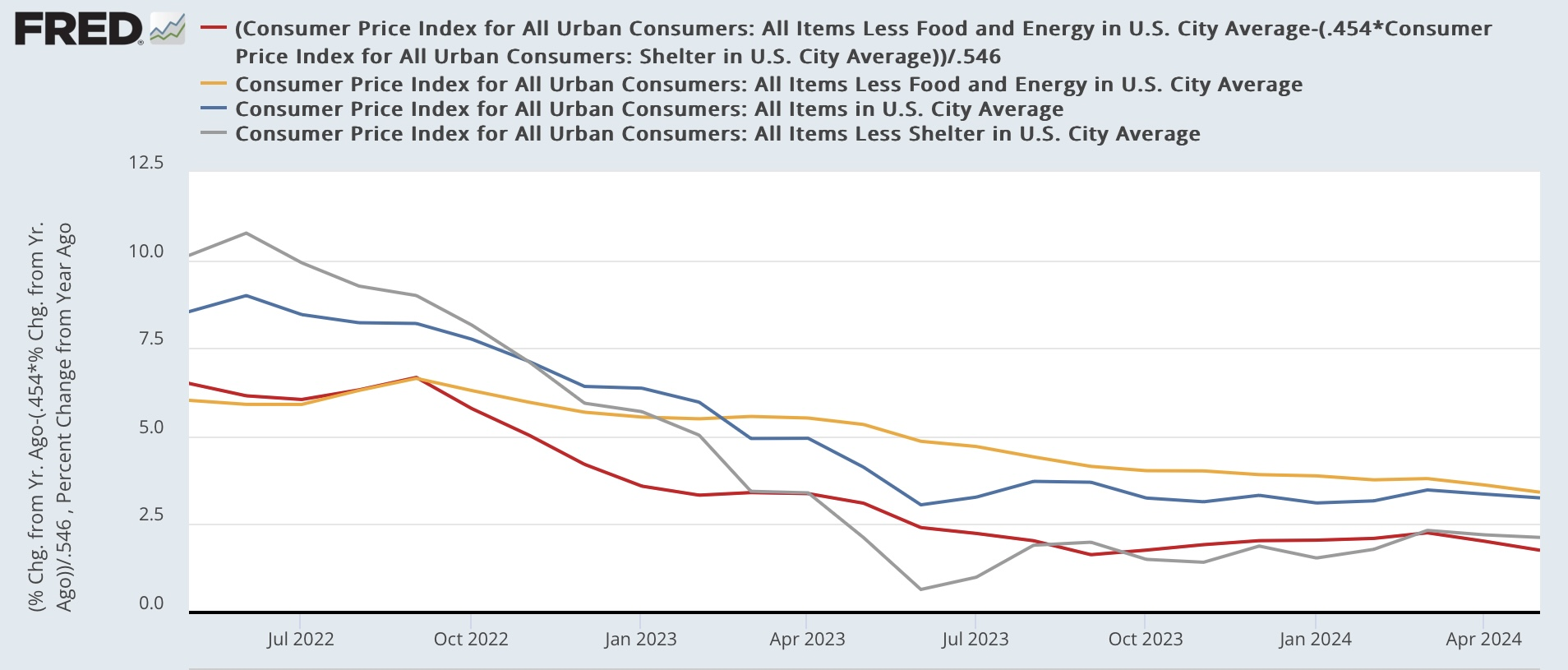

Paul Krugman put out an instantaneous rejoinder on X, that “core inflation has been higher than headline. But this is NOT because volatile food and energy are drivers of disinflation. It’s because excluding food and energy raises the weight of shelter. Over the past year headline ex-shelter is 2.1[%], core ex-shelter 1.9[%].”

Krugman doesn’t embody a graph, however reconstructing one on FRED shouldn’t be too troublesome which already consists of every little thing besides core ex-shelter. Since that’s roughly 45% of complete core CPI, all we now have to do is subtract it utilizing an applicable weighting (I’ve taken it out one additional decimal level to 45.4%). We discover that Krugman is appropriate.

To wit: the beneath graph consists of YoY headline (blue), core (gold), headline ex-shelter (grey), and core ex-shelter (purple) for the previous two years:

Click on on the picture to enlarge.

Whereas it’s true that core inflation has been falling extra slowly and stays barely greater than headline, headline and core inflation ex-shelter are decrease than each of them, and core ex-shelter is the bottom of all. My calculation to 1 additional decimal level truly rounds to 1.8% fairly than Krugman’s 1.9%.

In different phrases, the “last mile” is troublesome solely as a result of shelter prices have been so gradual to disinflate. And as I argued a number of weeks in the past (and others have argued as effectively), that in flip is as a result of greater mortgage charges, brought on by the Fed’s charge hikes themselves, have created a extreme scarcity in current houses on the market, driving *up* their costs.

Additional, as I argued final Friday, the probably reason behind the latest upturn in unemployment shouldn’t be a mirrored image of the Phillips curve, however fairly largely a perform of a pointy improve within the labor power attributable to a equally sharp spike in immigration. To briefly recap that argument: on common within the decade earlier than the pandemic, the US noticed one thing like 0.5% annual inhabitants progress. Name it 1.7 million to be beneficiant.

However after slumping through the pandemic, starting in 2022 an extra 2 million immigrants every year entered the U.S. over their pre-pandemic common.

Immigration and the housing market freeze are making the “last mile” of disinflation more durable, not the Phillips Curve – Offended Bear and The Bonddad Weblog: Immigration and the housing market freeze are making the “last mile” of disinflation more durable, not the Phillips Curve

When you take a look at Half 1 and Half 2 of The Demographic Outlook: 2024 to 2054 CBO projections. The estimation of Web Immigration varies wherever from 2.7 to three.3 million to the US in 2024. In Half 1, of CBO’s present estimates, web immigration is bigger than the company estimated final 12 months, by 0.7 million individuals in 2021, 1.4 million individuals in 2022, 1.9 million individuals in 2023, 2.1 million individuals in 2024, 1.5 million individuals in 2025, and 0.7 million individuals in 2026. There may be a lot getting in inhabitants progress via immigration.

Certainly, New Deal democrats evaluation is supported by the CBO’s calculations which AB introduced earlier in June in these two posts above. If I get a while, I’ll compose a Half III.

April 2024 Labor Market Replace: Posted Wage Development Is Declining Throughout Sectors, however Not on the Identical Price, Certainly Hiring Lab