– by New Deal democrat

As promised yesterday, at the moment let me take an prolonged have a look at the essential main sector of housing. I wish to stroll by means of every of the essential sequence typically within the order during which they’ve sometimes peaked, and the way in at the least one essential respect this time is – considerably – totally different.

First, right here is one other variation on a graph I’ve run many instances, exhibiting how mortgage charges (pink) sometimes lead each whole (darkish blue) and single household (gold) permits and the extra noisy begins (gentle blue). Right here is 1972-98:

And right here is 1999-present:

The magnitude of the response shouldn’t be all the time proportionate (see the Seventies) and in at the least one case (the housing bubble and bust of the 2000s) overwhelmed by different elements, however the relationship nearly all the time holds.

Here’s a close-up on the post-pandemic interval:

As standard, not good, however the main main/lagging relationship holds. Most significantly for at the moment’s functions, be aware that mortgage charges haven’t modified considerably previously 20 months, and since then each permits and begins have change into extra rangebound YoY as properly.

Subsequent, let me present the connection between new dwelling gross sales (pink) and permits, first from 1962 to 1994:

And 1995-present:

The purpose right here is that gross sales lead even permits – however they’re much extra noisy (and in addition closely revised), which is why I pay extra consideration to permits.

Right here is the post-pandemic close-up, exhibiting that as standard gross sales each peaked and troughed first, earlier than permits, and have been equally rangebound since mid-2023:

For completeness’ sake, listed below are buy mortgage functions as properly:

Sadly FRED shouldn’t be allowed to publish these, however be aware that they peaked proper after new houses bought and proper earlier than permits. Additionally they troughed in late 2023, and have been rangebound till the tip of 2024, earlier than rising within the early a part of this 12 months. That will usually be an excellent signal, however functions have declined once more within the wake of the latest improve in mortgage charges resulting from Tariff-palooza!

Subsequent, let’s delete the extra noisy begins, and evaluate whole and single household permits with housing models below development (gold, proper scale), all normed to their 2022 peaks:

The details listed below are that models below development – which as I nearly all the time say, is the true whole of the financial exercise on this sector – comply with permits (and begins) with a lag. And secondly that when there have been recessions, the variety of models below development continued to say no proper into the interval of precise financial contraction.

As soon as once more, let’s concentrate on the post-pandemic interval:

As standard, the variety of models below development adopted permits by a bit of below a 12 months. Notice additionally that as per the above dialogue of mortgage charges, absolutely the variety of permits has been rangebound for nearly two years – till presumably yesterday’s report, which can have been the primary one reflecting the impression of tariffs (on lumber, for instance).

However extra importantly, the variety of models below development has declined nearly each month previously 18, and is properly throughout the vary of declines the place beforehand recessions have begun. Certainly, if models below development stabilized for a major time period, that might counsel a recession has been prevented – however that has not occurred.

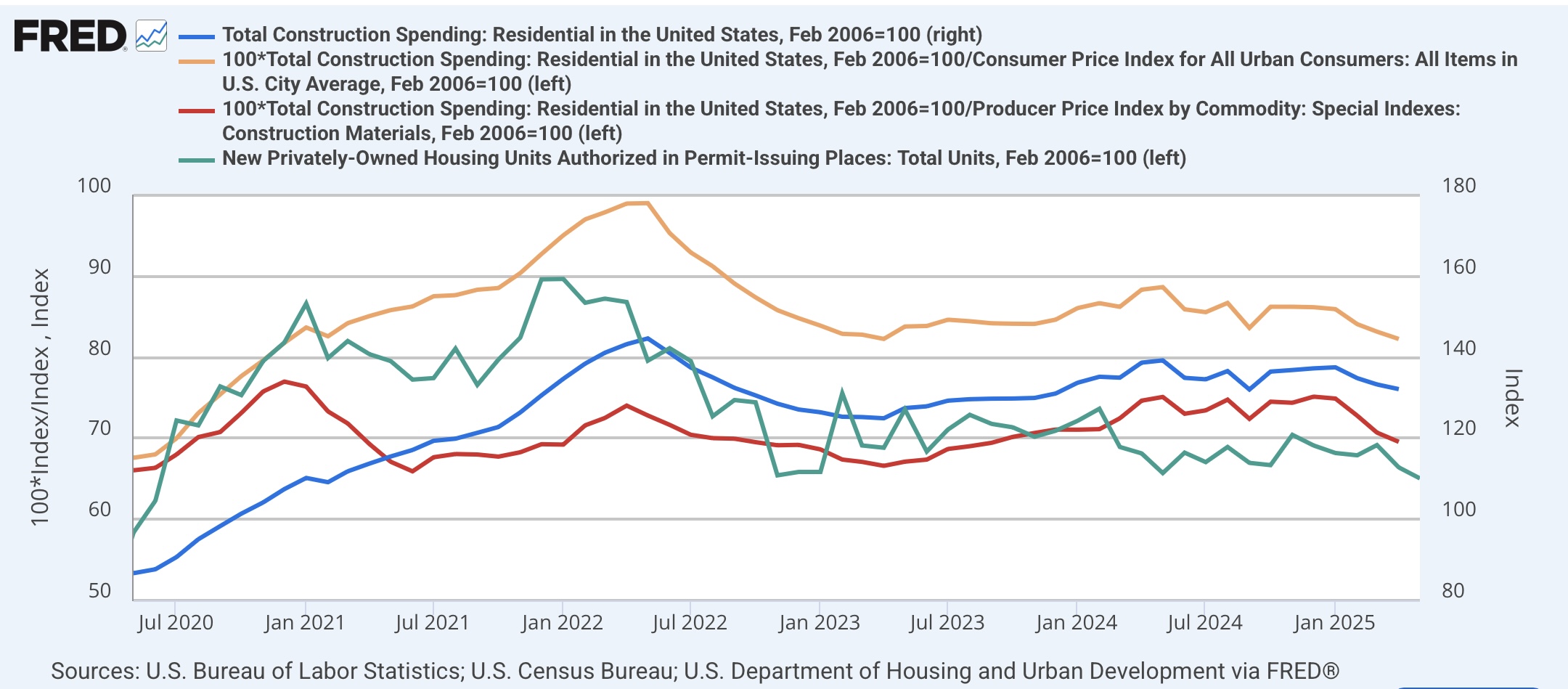

Earlier than I get to the ultimate sequence in chronological order, let me be aware that development spending, whether or not nominal or adjusted for inflation, peaked nearly concurrently with permits in 2006:

Submit-pandemic, as measured by development prices, development spending peaked on the time of the preliminary peak in permits in early 2001. Nominally or deflected by the CPI, it peaked a number of months earlier than permits (teal) did in 2022:

Notice that previously a number of months residential development spending has additionally declined additional, simply as permits have performed.

Now let’s check out what the ultimate sneakers to drop sometimes have been earlier than recessions have began, homes on the market (blue) and residential development employment (pink), compared with models below development:

Though I received’t present a graph this time, do not forget that houses on the market lag houses bought within the housing gross sales report, and it has solely been as soon as houses on the market peak after which flip down that recessions have begun. There isn’t any clear sample as as to whether houses on the market or residential development employment peak first, however each lag models below development.

And now, our closing post-pandemic look:

The variety of homes on the market declined barely in April, however it’s too quickly to know whether or not that marks the height or is simply noise. However previously 6 months, the quantity houses on the market have solely elevated by 1.2%. Residential development employment continues to be rising!

Let me make one closing level about these final two graphs. On the outset of this publish I wrote that at the least one factor was considerably totally different about this cycle, which has loads to do with why the variety of models below development appeared to levitate for therefore many months after permits and begins peaked, and why employment on this sector has not turned down but.

Discover, starting in about 2012, how a lot development employment lagged the rise in models below development. Between then and the outset of the pandemic, models below development almost tripled, whereas the variety of employees constructing these models solely elevated 50%. That has solely been exacerbated for the reason that pandemic, as models below development peaked at greater than *quadruple* their quantity in 2011, whereas employment within the sector is barely up 70%.

With such a giant decline within the variety of laborers per unit being constructed, it’s no surprise that the lag time has been so nice, and the necessity to lay off employees so little. But when there may be to be a recession, nearly definitely each of the ultimate sneakers on this chronological panorama will drop first. And Tariff-palooza! would possibly simply do the trick.

[P.S.: Since there is no significant data tomorrow, and given the length of this post, don’t be surprised if I play hooky.]